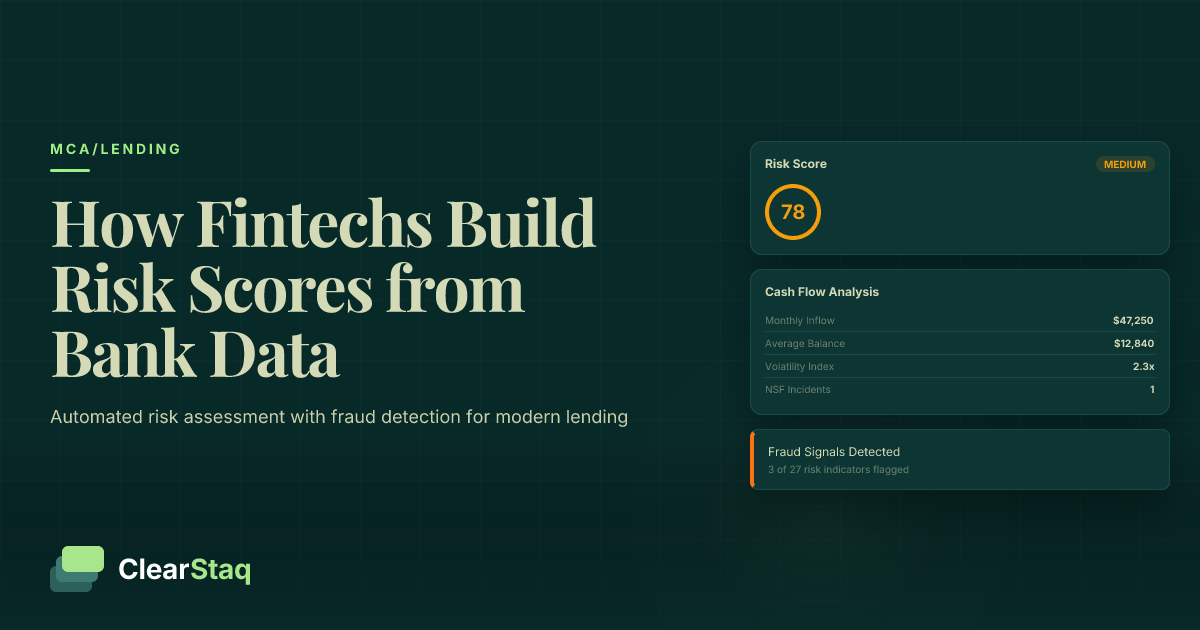

Fintech lenders build risk scores from bank statements by analyzing cash flow patterns, transaction volatility, revenue consistency, expense ratios, and balance trends using automated models. Advanced platforms integrate 27 fraud detection signals with risk assessment to generate comprehensive scores in real-time through API processing.

What you'll learn

- Bank statement risk scoring analyzes real-time cash flow patterns versus historical credit events

- Revenue consistency and expense ratios are stronger predictors than absolute income amounts

- Automated models achieve 85-95% accuracy in default prediction for cash-flow dependent businesses

- Fraud detection integration significantly improves risk assessment by identifying document manipulation

- Real-time API processing delivers risk scores within 30-60 seconds of statement upload

Fintech lenders build risk scores from bank statements by analyzing cash flow patterns, transaction volatility, revenue consistency, expense ratios, and balance trends using automated models. Advanced platforms integrate 27 fraud detection signals with risk assessment to generate comprehensive scores in real-time through API processing.

Why Fintech Lenders Rely on Bank Statement Risk Scoring

Traditional credit scores miss the financial reality of today's borrowers. A business owner with a 680 credit score might have inconsistent cash flow, while someone with a 620 score could have steady monthly revenue. Bank statement risk scoring fills these gaps by analyzing real cash flow behavior instead of relying on historical credit events.

The shift to cash flow-based underwriting has accelerated rapidly. According to Federal Reserve data, over 60% of alternative lenders now incorporate bank statement income verification into their risk models. This approach provides lenders with current financial behavior patterns that credit scores simply can't capture.

Limitations of Traditional Credit Scoring

Credit scores focus on payment history, credit utilization, and length of credit history. These metrics tell you how someone managed debt in the past, but they don't reveal current cash flow capacity. A borrower could have perfect payment history but face seasonal revenue drops that affect repayment ability.

Traditional scoring also struggles with thin-file borrowers — business owners and individuals with limited credit history. These borrowers represent a significant market opportunity, but standard underwriting models can't assess their risk accurately without alternative data sources.

The Rise of Cash Flow Underwriting

Market adoption has been driven by necessity. Fintech lenders competing against traditional banks need speed and accuracy advantages. Manual bank statement review takes days; automated risk scoring delivers results in seconds. This speed difference often determines whether a borrower accepts or declines a loan offer.

Regulatory acceptance has grown alongside market adoption. The CFPB and OCC have published guidance supporting the use of alternative data in lending decisions, provided lenders maintain fair lending compliance and model validation standards.

Key Bank Statement Data Points for Risk Assessment

Bank statement risk scoring analyzes multiple financial dimensions simultaneously. Revenue consistency matters more than revenue amount — a borrower earning $8,000 monthly with 5% variation presents lower risk than someone earning $12,000 with 40% volatility. The key is identifying patterns that predict repayment capacity.

Modern risk models examine four primary categories: revenue metrics, expense patterns, cash flow health, and transaction behavior. Each category contributes weighted signals to the overall risk score, with weights adjusted based on loan type and borrower characteristics.

Revenue Analysis Metrics

Revenue consistency ranks as the strongest predictor of repayment ability. Risk models calculate coefficient of variation across monthly revenue, seasonal adjustments for businesses with predictable cycles, and growth trends over 6-12 month periods.

The most predictive revenue metrics include:

- Monthly variance coefficient: Standard deviation divided by mean monthly revenue

- Seasonal factor: Adjustment for predictable revenue cycles

- Growth trajectory: 6-month revenue trend analysis

- Revenue concentration: Dependency on single income sources

Expense Pattern Recognition

Expense analysis reveals operational efficiency and financial management skills. Risk models distinguish between operational expenses (rent, payroll, inventory) and discretionary spending (entertainment, luxury purchases) to assess business health versus personal financial management.

Automated transaction categorization enables precise expense ratio calculations. Expense-to-revenue ratios above 85% typically indicate higher risk, while consistent operational expense patterns suggest stable business management. For detailed insights into how transaction types affect risk assessment, see our guide on transaction types and business health.

Cash Flow Health Indicators

Cash flow health metrics focus on liquidity and financial stability. Average daily balance provides baseline liquidity assessment, while negative balance frequency indicates cash flow stress. Overdraft patterns reveal whether cash shortfalls are occasional or systematic problems.

Critical cash flow indicators include:

- Average daily balance: Mean balance across statement period

- Minimum balance reached: Lowest balance point and frequency

- Days with negative balance: Frequency and duration of overdrafts

- NSF fee patterns: Frequency and amounts of insufficient fund charges

For comprehensive analysis of how NSF fees and negative balance patterns affect borrower risk assessment, lenders use automated detection systems that flag concerning patterns immediately.

This business demonstrates strong financial health with consistent cash flow and minimal overdraft activity. Recommended for approval with standard terms.

Building Automated Risk Scoring Models

Automated bank statement risk scoring requires sophisticated data processing pipelines. Raw bank statement data comes in 900+ different formats, each with unique structures, fonts, and layouts. Risk models can only be as accurate as the data feeding them, making standardization the critical first step.

The model building process follows three stages: data preprocessing, model training, and real-time integration. Each stage presents unique challenges, from format normalization to fraud detection integration. Successful implementations require careful attention to data quality, model validation, and continuous monitoring.

Data Preprocessing and Standardization

Data preprocessing transforms raw bank statements into standardized transaction records. This process handles format variations across 900+ bank format support systems, extracting consistent data fields regardless of source format.

Key preprocessing steps include:

- Format normalization: Converting PDFs, CSV, and OFX files to unified structure

- Transaction parsing: Extracting dates, amounts, descriptions, and balances

- Data validation: Checking for mathematical consistency and completeness

- Quality scoring: Assessing statement completeness and reliability

Transaction categorization uses machine learning to classify expenses and revenue streams automatically. Automated expense categorization enables precise operational ratio calculations that manual review couldn't achieve at scale.

Model Training and Validation

Risk model training requires historical performance data linking bank statement patterns to actual loan outcomes. Training datasets must include diverse borrower profiles, economic conditions, and loan types to ensure model robustness across market segments.

Model validation uses standard machine learning techniques with finance-specific considerations. Cross-validation prevents overfitting, while holdout testing validates performance on unseen data. Model accuracy metrics focus on default prediction rather than traditional classification accuracy.

Ready to Build Risk Scores That Combine Financial Metrics with Fraud Detection?

Try ClearStaq's integrated risk assessment platform with a free trial. See how automated bank statement processing feeds real-time risk models with comprehensive fraud protection.

API Integration Architecture

Real-time risk scoring requires robust API architecture supporting high-volume processing with low latency. Modern fintech lenders expect risk scores within 30-60 seconds of statement upload, including fraud detection and compliance checks.

Integration architecture considerations include:

- Webhook processing: Asynchronous statement processing with status updates

- Error handling: Graceful degradation for incomplete or corrupted statements

- Rate limiting: Managing high-volume processing loads

- Result caching: Optimizing repeated requests for same borrower

For technical implementation details, see our bank statement processing pipeline guide covering webhook integration and error handling strategies.

Advanced Risk Metrics Fintech Lenders Track

Beyond basic cash flow analysis, advanced risk models calculate sophisticated financial ratios that predict repayment capacity. Debt Service Coverage Ratio (DSCR) calculations use bank statement data to assess borrower ability to service additional debt based on actual cash flow performance.

The most predictive advanced metrics combine multiple data dimensions into composite scores. Revenue volatility coefficients weighted against average balances provide nuanced risk assessment. Operational efficiency ratios reveal business management quality beyond simple revenue numbers.

Cash Flow-Based DSCR

Traditional DSCR calculations rely on tax returns or financial statements that may be months old. Bank statement-based DSCR uses recent cash flow data for current repayment capacity assessment. Monthly DSCR calculations provide more granular analysis than annualized figures.

Advanced DSCR calculations include:

| Metric | Calculation Method | Risk Threshold |

|---|---|---|

| Monthly DSCR | Net Operating Income / Total Debt Service | < 1.2 High Risk |

| Seasonal DSCR | Seasonally Adjusted NOI / Debt Service | < 1.0 High Risk |

| Forward DSCR | Projected NOI / Proposed Debt Service | < 1.15 Decline |

For comprehensive guidance on cash flow assessment techniques, see our detailed analysis of cash flow analysis methodologies used by top MCA lenders.

Volatility and Stability Metrics

Revenue volatility measurement goes beyond simple standard deviation. Risk models calculate coefficient of variation, seasonal adjustments, and trend-adjusted volatility to distinguish between predictable seasonal variation and concerning irregularity.

Balance trend analysis reveals cash management patterns. Consistently declining balances indicate potential liquidity problems, while stable or growing balances suggest healthy cash flow management. The trend direction often matters more than absolute balance amounts.

Operational Health Indicators

Operational efficiency ratios assess business management quality beyond raw financial performance. Expense ratios, working capital trends, and burn rate calculations provide insights into borrower operational competence.

Key operational metrics include:

- Operating expense ratio: Operating expenses divided by total revenue

- Working capital velocity: Change in net working capital over time

- Cash burn rate: Monthly cash consumption rate for growing businesses

- Revenue per transaction: Average transaction size and frequency trends

Understanding the difference between true revenue vs gross revenue becomes critical for accurate operational ratio calculations, especially for businesses with high transaction volumes.

Integrating Fraud Detection with Risk Scoring

Fraud detection integration transforms traditional risk scoring by adding document authenticity assessment to financial analysis. A borrower might present excellent cash flow patterns, but if the bank statement shows manipulation signs, the overall risk profile changes dramatically.

Modern risk platforms combine financial metrics with fraud signals in real-time. When 27 fraud detection signals indicate potential document manipulation, risk scores adjust automatically to reflect the increased uncertainty and potential misrepresentation.

Fraud as a Risk Multiplier

Document fraud doesn't just indicate dishonesty — it suggests the underlying financial data may be unreliable. Risk models treat fraud signals as multipliers rather than additive factors. A moderate financial risk borrower with fraud signals becomes high risk due to data uncertainty.

Common fraud indicators that affect risk scores include:

- PDF metadata inconsistencies: Creation date mismatches or software anomalies

- Font irregularities: Mixed fonts suggesting manual editing

- Balance calculation errors: Running balance inconsistencies

- Transaction pattern anomalies: Unusual deposit timing or amounts

For comprehensive coverage of fraud detection techniques, see our guide on how to fake bank statement detection using automated analysis tools.

Real-Time Fraud Assessment

Real-time fraud detection during underwriting prevents fraudulent applications from reaching human underwriters. Automated systems analyze PDF metadata analysis alongside financial patterns to flag suspicious documents immediately.

Integration architecture processes fraud detection and financial analysis simultaneously, delivering combined risk scores that account for both repayment capacity and document authenticity. This dual-analysis approach significantly improves overall model accuracy.

Real-World Implementation: How Top Fintechs Do It

A leading MCA lender implemented automated bank statement risk scoring and reduced default rates by 40% while cutting underwriting time from 2 days to 15 minutes. The key was combining comprehensive financial analysis with real-time fraud detection in a single automated workflow.

Implementation success requires careful planning around data integration, model validation, and staff training. The most successful deployments start with pilot programs processing 10-20% of applications before scaling to full automation.

MCA Lending Success Story

The lender processed 50,000+ applications annually using manual bank statement review. Underwriters spent 45 minutes per statement, missing subtle fraud indicators and inconsistent risk assessment. Default rates averaged 18% across their portfolio.

After implementing automated risk scoring:

- Default rates dropped to 11% through improved risk assessment accuracy

- Processing time reduced to 15 minutes including fraud detection

- Underwriter productivity increased 300% focusing on complex cases only

- Cost per application decreased 60% through automation

The ROI analysis showed $2.8M annual savings from reduced defaults and operational efficiency, with implementation costs recovered within 8 months.

Technical Implementation Roadmap

Successful implementation follows a structured approach: API integration, data validation testing, model calibration, and gradual rollout. Most fintech lenders complete implementation within 60-90 days using established integration frameworks.

Key implementation steps include:

- API integration setup: Webhook configuration and authentication

- Data validation testing: Accuracy verification across bank formats

- Model calibration: Risk threshold adjustment for portfolio characteristics

- Staff training: Underwriter education on automated scoring interpretation

- Monitoring deployment: Performance tracking and model adjustment

For detailed technical guidance, see our ClearStaq API integration documentation covering authentication, error handling, and best practices.

Overcoming Common Challenges

Data quality issues represent the most common implementation challenge. Inconsistent statement formats, missing data, and poor PDF quality can affect model accuracy. Robust preprocessing pipelines with quality scoring help identify and handle problematic statements.

Model accuracy concerns often arise during initial deployment. Regular backtesting against historical performance data and continuous model monitoring ensure sustained accuracy. Most lenders see improved performance within 30-60 days as models adapt to portfolio characteristics.

Best practices for implementation success align with industry standards outlined in our comprehensive MCA underwriting checklist covering risk assessment, compliance, and operational procedures.

Compliance and Regulatory Considerations

Bank statement-based lending operates under existing consumer protection frameworks, primarily FCRA for alternative data usage and fair lending requirements. Lenders must ensure model fairness, maintain adverse action procedures, and document risk assessment methodologies.

Data security requirements have intensified with increased digital processing. SOC2 compliance standards apply to any platform processing sensitive financial data, requiring comprehensive security controls and regular auditing.

FCRA and Alternative Data

Bank statement data used for credit decisions falls under FCRA requirements when obtained from third parties. Lenders must have permissible purposes, maintain reasonable procedures for data accuracy, and provide adverse action notices when declining applications based on bank statement analysis.

Key FCRA compliance requirements include:

- Permissible purpose verification: Documented business need for data access

- Adverse action notices: Specific reasons for credit denial

- Consumer notification: Disclosure of alternative data usage

- Dispute procedures: Process for data accuracy challenges

Fair Lending Compliance

Fair lending requirements apply to all credit decisions, including those based on alternative data. Lenders must test models for disparate impact, document business justification for risk factors, and maintain consistent application procedures across borrower demographics.

Model bias testing requires regular analysis of approval rates, pricing, and risk scores across protected classes. Any disparate impact must be justified by business necessity and demonstrated predictive value for credit risk assessment.

Data Security Standards

Financial data processing requires enterprise-grade security controls. SOC2 Type II compliance provides the industry standard framework for data security, availability, and confidentiality controls. Regular penetration testing and security audits ensure ongoing protection.

Required security measures include:

- Encryption at rest and in transit: AES-256 encryption for all data storage and transmission

- Access controls: Role-based permissions with multi-factor authentication

- Audit logging: Comprehensive activity tracking and monitoring

- Incident response: Documented procedures for security breaches

The Future of Bank Statement Risk Scoring

Machine learning advances continue improving pattern recognition accuracy. Neural networks trained on millions of bank statements can identify subtle risk indicators that traditional statistical models miss. These advances particularly benefit thin-file borrower assessment and fraud detection.

Open banking adoption will transform risk scoring by providing real-time account access instead of static statement uploads. Direct bank connections enable continuous monitoring, real-time balance verification, and immediate fraud detection for ongoing risk management.

Emerging Technologies

Advanced ML models using transformer architectures show promising results for sequential transaction analysis. These models understand transaction context and relationships better than traditional feature-based approaches, improving both accuracy and explainability.

Real-time data streams from open banking APIs enable dynamic risk assessment. Instead of monthly statement snapshots, lenders can monitor cash flow changes, detect account activity anomalies, and adjust risk scores based on current behavior patterns.

Predictive analytics evolution focuses on forward-looking risk indicators. Models trained on economic data, industry trends, and seasonal patterns can predict borrower stress before it appears in current bank statements.

Industry Evolution

Regulatory developments continue supporting alternative data adoption while strengthening consumer protection requirements. The CFPB's emphasis on fair lending compliance and model explainability shapes industry best practices for risk assessment.

Industry standardization efforts aim to establish common frameworks for bank statement analysis, fraud detection, and risk scoring. These standards will improve consistency across lenders and enable more efficient compliance management.

Market adoption trends suggest bank statement risk scoring will become standard practice for most alternative lenders by 2026. For detailed analysis of market evolution, see our report on MCA industry trends and technological adoption patterns.

Frequently Asked Questions

How do lenders calculate risk scores from bank statements?

Lenders analyze cash flow patterns, revenue consistency, expense ratios, balance trends, and transaction velocity using automated models. Advanced platforms combine financial metrics with fraud detection signals to generate comprehensive risk scores in real-time.

What bank statement data points affect credit risk most?

The most predictive data points are revenue consistency, expense-to-revenue ratios, negative balance frequency, overdraft patterns, and transaction volatility. These indicators reveal cash flow health and repayment capacity better than traditional credit scores.

How accurate are automated risk scoring models?

Modern bank statement risk scoring models achieve 85-95% accuracy in predicting default risk, significantly outperforming traditional credit scores for cash-flow dependent businesses. Accuracy improves with more transaction history and fraud detection integration.

What role does transaction categorization play in risk assessment?

Automated transaction categorization enables precise calculation of operational ratios, revenue recognition, and expense patterns. It distinguishes between business and personal transactions, improving model accuracy and regulatory compliance for commercial lending.

How do seasonal businesses affect bank statement risk scoring?

Risk models adjust for seasonality by analyzing 12+ months of data, calculating seasonal coefficients, and normalizing revenue patterns. Advanced models use industry benchmarks and historical seasonal trends to accurately assess year-round repayment capacity.

Transform Your Underwriting with Bank Statement Risk Scoring

Build risk scores that are faster, more accurate, and fraud-aware. ClearStaq combines comprehensive financial analysis with 27 fraud detection signals for complete borrower assessment. Start your free trial today.

Frequently Asked Questions

How do lenders calculate risk scores from bank statements?

Lenders analyze cash flow patterns, revenue consistency, expense ratios, balance trends, and transaction velocity using automated models. Advanced platforms combine financial metrics with fraud detection signals to generate comprehensive risk scores in real-time.

What bank statement data points affect credit risk most?

The most predictive data points are revenue consistency, expense-to-revenue ratios, negative balance frequency, overdraft patterns, and transaction volatility. These indicators reveal cash flow health and repayment capacity better than traditional credit scores.

How accurate are automated risk scoring models?

Modern bank statement risk scoring models achieve 85-95% accuracy in predicting default risk, significantly outperforming traditional credit scores for cash-flow dependent businesses. Accuracy improves with more transaction history and fraud detection integration.

What role does transaction categorization play in risk assessment?

Automated transaction categorization enables precise calculation of operational ratios, revenue recognition, and expense patterns. It distinguishes between business and personal transactions, improving model accuracy and regulatory compliance for commercial lending.

How do seasonal businesses affect bank statement risk scoring?

Risk models adjust for seasonality by analyzing 12+ months of data, calculating seasonal coefficients, and normalizing revenue patterns. Advanced models use industry benchmarks and historical seasonal trends to accurately assess year-round repayment capacity.

ClearStaq Team

Product Team

The ClearStaq team builds AI-powered tools for bank statement parsing, fraud detection, and income verification.