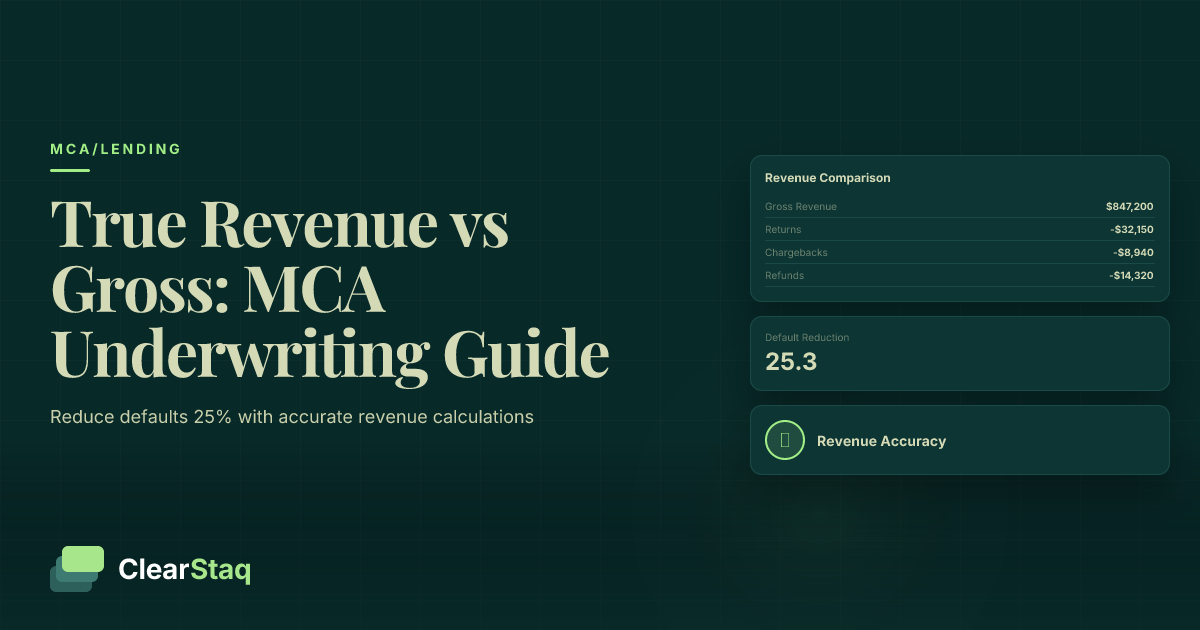

True revenue represents actual business income after deducting returns, refunds, and chargebacks, while gross revenue is the total sales amount before adjustments. For MCA underwriting, true revenue provides accurate repayment capacity assessment, reducing default risk by 15-25% compared to gross revenue calculations alone.

What you'll learn

- True revenue calculation reduces MCA default rates by 15-25% compared to gross revenue methods

- Automated parsing processes revenue calculations in 2 minutes versus 45 minutes manually

- Revenue manipulation through fake deposits is detectable using 27+ fraud signals

- Processing fees and chargebacks can inflate gross revenue by 3-7% monthly

- Seasonal adjustments prevent overadvancing during peak performance periods

True revenue represents actual business income after deducting returns, refunds, and chargebacks, while gross revenue is the total sales amount before adjustments. For MCA underwriting, true revenue provides accurate repayment capacity assessment, reducing default risk by 15-25% compared to gross revenue calculations alone.

True Revenue vs. Gross Revenue: Key Definitions

In merchant cash advance underwriting, understanding the distinction between true revenue and gross revenue isn't just accounting semantics—it's the difference between profitable lending and costly defaults. While these terms might sound straightforward, their application in MCA risk assessment requires precision that many lenders overlook.

Gross revenue represents the total sales amount before any deductions. It's the raw number that appears when you sum up all deposits in a bank statement. For a restaurant processing $50,000 in monthly credit card sales, that full amount counts as gross revenue—regardless of what happens after the initial transaction.

True revenue takes gross revenue and subtracts returns, refunds, chargebacks, and other reversals. It represents the actual money a business keeps. That same restaurant might show $50,000 in gross revenue but only $47,500 in true revenue after accounting for $2,500 in refunds and chargebacks.

The distinction between net revenue and true revenue adds another layer of complexity in MCA context. While traditional accounting defines net revenue as gross revenue minus direct costs of goods sold, MCA underwriters focus on true revenue—the actual cash available for advance repayment. Standard accounting definitions don't fully capture the cash flow reality that determines a merchant's ability to pay back daily or weekly ACH debits.

What Counts as Gross Revenue

Identifying gross revenue starts with recognizing all legitimate business income sources. Credit card deposits form the backbone of most merchants' revenue streams, appearing as batch settlements from processors like Square, Stripe, or traditional merchant services providers.

ACH payments represent another crucial revenue component, especially for B2B merchants or service businesses with recurring billing. These direct deposits often appear with customer names or invoice numbers, requiring careful analysis to distinguish from loans or internal transfers.

Cash deposits still matter for certain industries, though they present verification challenges. Restaurants, convenience stores, and service businesses may show regular cash deposits that represent legitimate revenue but require additional documentation to verify.

Digital payment platforms have exploded in recent years. Deposits from PayPal, Venmo for Business, Zelle, and cryptocurrency processors all count toward gross revenue when they represent actual sales transactions rather than personal transfers or loan proceeds.

Understanding True Revenue Adjustments

Converting gross revenue to true revenue requires systematic identification and subtraction of reversals. Returns and refunds appear as negative transactions or separate debits, often days or weeks after the original sale. A clothing retailer might process a $500 sale on March 1st but issue a refund on March 15th—both transactions affect the true revenue calculation for March.

Chargebacks and disputes create additional complexity. These forced reversals typically appear 30-90 days after the original transaction, sometimes crossing monthly statement boundaries. A merchant showing strong January gross revenue might face significant chargebacks in March from holiday sales disputes.

Processing fees impact the equation differently. While some lenders deduct processing fees to calculate "net deposits," most MCA underwriters include them in true revenue calculations since merchants must still generate the gross sales to incur these fees. The distinction matters when setting advance amounts and payment terms.

Seasonal adjustment considerations add nuance to true revenue calculations. A tax preparation business might show minimal refunds during peak season but face higher reversal rates during off-peak months. Understanding these patterns prevents overadvancing based on temporarily inflated numbers.

Common Revenue Terms in MCA Underwriting

Operating revenue forms the core of true revenue calculations—it's the income from a business's primary activities. For a restaurant, it's food and beverage sales. For a medical practice, it's patient service fees. Non-operating revenue like insurance settlements, asset sales, or investment income typically doesn't count toward underwriting calculations since it doesn't reflect sustainable repayment capacity.

The distinction between recurring and one-time revenue shapes risk assessment. A SaaS company with $30,000 in monthly recurring revenue presents different risk than a contractor with the same amount from one-time project payments. MCA underwriters weight recurring revenue more heavily when calculating advance amounts.

Seasonal versus baseline revenue requires careful analysis. An ice cream shop showing $80,000 in July revenue and $20,000 in January has a $20,000 baseline with $60,000 in seasonal uplift. Advances based on peak season numbers without accounting for this variance lead to payment stress during slow periods.

Why the Distinction Matters for MCA Risk Assessment

The gap between gross and true revenue directly impacts every aspect of MCA underwriting, from initial approval decisions to factor rate calculations. Lenders who base decisions on gross revenue alone face systematic risk that compounds across their portfolio.

Impact on factor rate calculations proves immediate and measurable. A merchant showing $100,000 in gross revenue but only $85,000 in true revenue represents 15% less actual repayment capacity. Pricing an advance based on the inflated number means either charging too little for the actual risk or setting payments the merchant can't sustain.

Default rate differences between gross and true revenue underwriting tell a compelling story. Analysis of MCA portfolios shows that advances based on properly calculated true revenue default 15-25% less frequently than those using gross revenue figures. This improvement stems from better matching advance amounts and payment terms to actual business cash flow.

Regulatory compliance adds another dimension to accurate revenue assessment. State lending regulations increasingly require documented income verification and reasonable ability-to-repay analysis. True revenue calculations provide the defensible methodology needed for compliance documentation.

Portfolio performance improvements extend beyond individual deals. Lenders using true revenue calculations report better vintage performance, lower modification rates, and improved investor confidence. The ripple effects of accurate underwriting compound over time.

Default Rate Impact

The 15-25% reduction in defaults from true revenue underwriting isn't theoretical—it's backed by portfolio data across multiple MCA lenders. One ISO analyzing 1,000 funded deals found their default rate dropped from 12% to 9% after implementing true revenue calculations, saving over $2 million in losses annually.

Case studies reveal the pattern consistently. A restaurant group funded based on $200,000 monthly gross revenue defaulted within four months when chargebacks and refunds weren't considered. Their true revenue of $170,000 couldn't support the aggressive payment schedule. Similar scenarios play out across retail, e-commerce, and service sectors when comprehensive MCA underwriting checklist protocols skip true revenue verification.

Pricing Accuracy Benefits

Better factor rate setting flows naturally from accurate revenue assessment. When underwriters know a merchant's true revenue, they can price risk appropriately. A 1.35 factor rate might work for strong true revenue, while questionable gross revenue figures might warrant 1.45 or decline altogether.

Reduced overadvancing risk protects both lender and merchant. Advances sized on true revenue align with actual repayment capacity, preventing the payment stress that leads to defaults, modifications, and damaged merchant relationships. The sustainability benefits compound through renewal and upsell opportunities.

Regulatory Considerations

Documentation standards for revenue verification continue evolving as states implement MCA-specific regulations. California, New York, and Virginia now require specific disclosures about how advances are calculated and assessed. True revenue calculations provide the clear methodology regulators expect.

Risk assessment compliance goes beyond simple documentation. Regulators examine whether lenders conduct meaningful ability-to-repay analysis. True revenue calculations demonstrate the sophistication expected in modern commercial finance, especially as consumer protection concepts migrate to small business lending.

How to Calculate True Revenue from Bank Statements

Calculating true revenue from bank statements requires systematic methodology, attention to detail, and understanding of transaction patterns. The process transforms raw banking data into actionable underwriting intelligence.

Step-by-step calculation methodology ensures consistency across deals and underwriters. Start with complete bank statements—partial months or missing pages invalidate the analysis. Most lenders require three to six months for accurate trending, though twelve months provides superior seasonal insight.

Transaction categorization forms the foundation of accurate revenue identification. Not every deposit represents revenue, and automated bank statement parsing technology can categorize thousands of transactions in seconds with higher accuracy than manual review.

Handling refunds, returns, and chargebacks requires tracking both original sales and their reversals. A $1,000 sale on day one followed by a $1,000 refund on day fifteen nets to zero true revenue, not $1,000 in gross revenue. This matching process grows complex with high transaction volumes.

Time period considerations affect calculation accuracy. Calendar month analysis might split related transactions, while statement cycle analysis maintains transaction integrity. Rolling averages smooth volatility but can mask declining trends that signal risk.

Step 1: Identify Revenue Transactions

Credit card processor deposits appear with recognizable patterns. Square shows as "SQ *MERCHANT NAME," while traditional processors like First Data or Global Payments use batch numbers and merchant IDs. These deposits represent gross sales but often net of processing fees, requiring adjustment calculations.

ACH business payments demand careful scrutiny. Legitimate B2B revenue shows consistent patterns—regular amounts from identified business customers, often with invoice numbers or customer references. Distinguishing these from loan deposits, tax refunds, or owner contributions requires transaction-level analysis.

Digital payment platforms continue proliferating. PayPal, Stripe, Shopify Payments, and Amazon Seller deposits all indicate revenue but with varying fee structures and timing. A single day's sales might appear across multiple platforms, requiring consolidation for accurate daily revenue tracking.

Excluding internal transfers prevents revenue inflation. Transfers between business accounts, credit line draws, or owner deposits don't represent sales activity. These transactions often show round numbers, paired credits/debits, or descriptive memos that reveal their non-revenue nature.

6 fields extracted automatically • 99.8% accuracy

Step 2: Calculate Adjustments

Returns identification starts with finding negative transactions or debits labeled as refunds, returns, or reversals. Modern processors often code these clearly, but some appear as generic debits requiring investigation. Matching returns to original sales provides insight into return rates and customer satisfaction.

Chargeback processing adds complexity since these forced reversals appear weeks or months after sales. Processors typically batch chargebacks separately from regular refunds, often with fee additions. High chargeback rates signal operational issues beyond simple revenue calculation concerns.

Fee deductions require nuanced handling. While processing fees don't reduce true revenue for MCA purposes, other fees like NSF charges, overdraft fees, or account maintenance fees should be excluded from revenue calculations. The distinction matters for accurate cash flow assessment.

Timing considerations affect monthly calculations significantly. A sale processed on January 31st might not deposit until February 2nd. Statement-based analysis captures actual cash timing, while accrual-based analysis matches sales to their occurrence period. Most MCA underwriters prefer cash-basis analysis for its payment prediction value.

Step 3: Apply Seasonal Factors

Historical trending reveals seasonal patterns crucial for accurate underwriting. Comparing the same month across multiple years shows whether current performance represents normal seasonality or concerning deviation. A landscaping company's 50% winter revenue drop might be expected, while a restaurant showing similar patterns signals problems.

Industry benchmarks provide context for seasonal adjustments. Retail businesses typically see 30-40% of annual revenue in Q4, while tax preparers might generate 70% between January and April. Understanding industry norms prevents overadvancing during peak seasons.

Peak period adjustments require mathematical precision. Calculate baseline revenue as the lowest sustainable monthly amount, then express peak months as multiples of baseline. This approach clarifies true repayment capacity during both strong and weak periods.

Common Revenue Calculation Mistakes That Cost Lenders

Revenue calculation errors create cascading problems throughout the underwriting process. These mistakes inflate advance amounts, underestimate risk, and ultimately drive portfolio losses that proper methodology prevents.

Including non-operating income as business revenue tops the list of costly errors. Insurance payouts, legal settlements, asset sales, and investment gains might boost bank balances but don't reflect sustainable business performance. One lender discovered 8% of their defaults traced to advances based on one-time insurance settlements misclassified as revenue.

Failing to account for processing fees and chargebacks creates systematic overstatement. A merchant processing $100,000 monthly might only receive $96,000 after fees, then face $3,000 in chargebacks. The $7,000 difference represents 7% overstatement of available cash flow—enough to push marginal deals into default.

Misclassifying internal transfers as revenue happens surprisingly often in manual reviews. Round-number transfers between accounts, loan proceeds, or owner capital injections inflate revenue figures without representing actual sales. Automated categorization catches these patterns that human reviewers miss in repetitive analysis.

Ignoring seasonal patterns and one-time payments leads to advances sized for peak performance rather than sustainable baselines. Holiday retailers, tourist destinations, and event-driven businesses show dramatic swings that require careful analysis and appropriate advance sizing.

The $50K Loan Refund Mistake

Case study analysis reveals how one misclassified transaction can doom a deal. A restaurant showed a $50,000 deposit labeled "SBA TREAS 310" that a junior underwriter counted as revenue. The advance was sized assuming $200,000 monthly revenue instead of the actual $150,000.

Impact on advance sizing proved immediate and severe. The extra $50,000 "revenue" supported a $30,000 larger advance with proportionally higher daily payments. When the mistake was discovered post-funding, the merchant already struggled with unsustainable payments.

Recovery challenges mounted quickly. The merchant couldn't support the inflated payments, leading to NSFs within the first month. Modification attempts failed because the true revenue couldn't support even reduced payments. The deal ultimately charged off at a 60% loss—entirely preventable with accurate revenue classification.

Processing Fee Oversights

The 3-4% revenue inflation from fees seems minor but compounds dangerously. A merchant processing $1 million annually might show $30,000-40,000 less in actual deposits than gross sales. Across a 12-month advance, this translates to $2,500-3,300 monthly overstatement of available cash flow.

Compound impact on factor calculations magnifies the error. If true revenue is $96,000 instead of $100,000, a 1.3 factor rate advance should be $124,800, not $130,000. The $5,200 difference might determine success or failure, especially for merchants operating on thin margins.

Timing and Seasonality Errors

Holiday spike misinterpretation creates January disasters. Retailers showing massive December revenue often face 50-70% drops in January. Advances based on December statements without seasonal adjustment default at alarming rates when reality hits in Q1.

Quarter-end payment clustering presents subtler risks. B2B merchants often show inflated month-end deposits as customers pay invoices before closing their own books. The clustering doesn't represent higher sales—just timing compression that reverses the following month.

Automated vs. Manual Revenue Analysis

The evolution from manual to automated revenue analysis represents a fundamental shift in MCA underwriting efficiency and accuracy. While experienced underwriters bring valuable judgment, technology delivers consistency and scale impossible through manual methods alone.

Time efficiency demonstrates the starkest contrast: automated systems process complete bank statement analysis in under 2 minutes, while manual review of the same statements takes 45-60 minutes for experienced underwriters. This 20-30x speed improvement transforms operational capacity and customer experience.

Accuracy improvements with automated categorization stem from consistent rule application across millions of transactions. Where human reviewers might categorize similar transactions differently based on fatigue or interpretation, automated systems apply identical logic every time. Pattern recognition algorithms identify revenue transactions with 99.5% accuracy across 900+ bank formats.

Scalability benefits multiply for high-volume lenders. A team of ten underwriters might process 100 deals daily with manual review. The same team using automated parsing can handle 500+ deals while focusing their expertise on exception handling and risk assessment rather than data entry.

Integration with existing underwriting workflows amplifies automation benefits. Modern APIs pass parsed revenue data directly into scoring models, CRMs, and decision engines. This integration eliminates transcription errors while enabling real-time decisioning.

Manual Analysis Limitations

Human error rates in manual transaction categorization typically range from 5-8% even with experienced staff. These errors compound when calculating totals, applying adjustments, and transcribing results. A misplaced decimal or skipped page can drastically alter revenue calculations.

Time consumption extends beyond the initial review. Quality control requires second reviews, error correction adds rework, and complex statements might need multiple passes. The true time cost often doubles the initial estimate when including these necessary steps.

Inconsistent categorization between underwriters creates portfolio-level risks. One underwriter might count PayPal transfers as revenue while another excludes them. These inconsistencies make portfolio analysis unreliable and risk modeling inaccurate.

Limited fraud detection represents perhaps the greatest manual review weakness. Human reviewers focus on calculating totals, not examining metadata, font consistency, or pixel-level anomalies that reveal statement manipulation. This gap leaves lenders exposed to sophisticated fraud schemes.

Automated Parsing Advantages

Consistent categorization rules ensure every transaction receives identical treatment regardless of volume or reviewer fatigue. Machine learning models trained on millions of transactions recognize patterns humans miss, correctly categorizing edge cases that confuse manual reviewers.

Real-time processing enables instant decision capability. Merchants upload statements and receive advance offers within minutes, not days. This speed advantage captures deals before competitors while reducing operational costs.

Fraud signal detection operates continuously across 27+ verification points. While calculating revenue, the system simultaneously checks for document tampering, unusual patterns, and consistency markers that reveal manipulation attempts. This dual-purpose analysis provides superior risk management without additional time investment.

API integration capabilities transform parsed data into actionable intelligence. Revenue calculations flow directly into: - Underwriting scorecards for automated decisioning - CRM systems for sales pipeline management - Risk monitoring platforms for portfolio surveillance - Accounting systems for reconciliation

This business demonstrates strong financial health with consistent cash flow and minimal overdraft activity. Recommended for approval with standard terms.

ROI of Automation

Labor cost savings provide immediate returns. Reducing review time from 45 minutes to 2 minutes saves approximately $35 per file in direct labor costs. For a lender processing 1,000 applications monthly, that's $35,000 in monthly savings—$420,000 annually.

Faster funding decisions capture more deals while reducing acquisition costs. Merchants choosing between lenders often select the first approval. Automated parsing enabling same-day approvals can increase close rates by 20-30% while reducing the sales cycle.

Reduced default rates from accurate revenue calculation and fraud detection provide the highest long-term returns. Even a 1% reduction in default rates saves $1 million annually per $100 million funded. Combined with labor savings and improved close rates, automation ROI typically exceeds 400% in the first year.

Beyond raw ROI calculations, automation enables strategic advantages. Lenders can pursue smaller deals profitably, enter new markets quickly, and scale operations without proportional headcount increases. The comprehensive cash flow analysis capabilities extend beyond simple revenue calculation to holistic financial assessment.

Red Flags: When Revenue Numbers Don't Add Up

Revenue manipulation represents one of the most common fraud types in MCA underwriting. Sophisticated fraudsters know lenders focus on revenue, making it a prime target for manipulation through document alteration or transaction insertion.

Identifying revenue manipulation requires understanding both technical and behavioral indicators. Technical signs include inconsistent fonts, impossible running balances, and metadata anomalies. Behavioral patterns reveal themselves through too-perfect round numbers, suspicious timing, and transactions that don't match business type.

Inconsistent deposit patterns signal potential problems even in unaltered statements. Legitimate businesses show natural variation in daily sales. Statements displaying identical daily deposits, perfectly ascending amounts, or patterns too regular for reality warrant deeper investigation.

Cross-referencing with processor statements provides crucial verification. Merchants can't easily alter statements from payment processors, making them valuable for confirming bank statement accuracy. Discrepancies between processor reports and bank deposits reveal manipulation attempts or operational issues requiring explanation.

Using fraud detection tools transforms verification from art to science. Modern systems analyze dozens of fraud indicators simultaneously, catching sophisticated schemes that fool human reviewers. The combination of automated detection and human investigation provides optimal protection.

Revenue Inflation Tactics

Fake deposit insertion remains the most direct manipulation method. Fraudsters add transactions to PDFs using editing software, inflating revenue to qualify for larger advances. These insertions often show subtle signs: slightly different fonts, alignment issues, or running balances that don't calculate correctly.

Processing fee manipulation involves altering fee amounts to show higher net deposits. A fraudster might change a 3.5% fee to 0.5%, making $96,500 in net deposits appear as $99,500. The $3,000 monthly difference supports significantly larger advances.

Date shifting schemes move future deposits into the statement period under review. January sales deposited in February get shifted back, inflating January revenue for underwriting while creating gaps discoverable through careful chronological analysis.

Detection Methods

Pattern analysis reveals unnatural regularities in supposedly organic business activity. Real businesses show daily variation, seasonal patterns, and random fluctuations. Statements showing too-perfect patterns like exactly $5,000 daily or precisely 10% weekly growth signal manipulation.

Metadata examination uncovers technical evidence of alteration. PDF creation dates after the statement period, multiple software signatures, or embedded fonts not matching bank standards all indicate tampering. Professional bank statement fraud red flags include these technical markers alongside content anomalies.

Cross-document verification compares bank statements against processor reports, tax returns, and accounting records. Revenue inflation in one document creates discrepancies with others, revealing fraud through inconsistency even when individual documents appear legitimate.

Automated Fraud Signals

Modern fraud detection analyzes 27 distinct signals simultaneously, far exceeding human capability. These signals span document integrity, transaction patterns, mathematical consistency, and behavioral anomalies. Machine learning models trained on millions of statements recognize subtle fraud patterns humans miss.

Real-time alert systems flag suspicious findings immediately during parsing. Rather than discovering fraud after funding, automated systems identify red flags during initial review. This early detection prevents losses while maintaining fast approval times for legitimate merchants.

The combination of revenue accuracy and MCA stacking detection provides comprehensive risk assessment. Accurate revenue calculation helps identify when existing advance payments consume too much cash flow, preventing overextension that leads to defaults.

Best Practices for Accurate Revenue Assessment

Establishing best practices for revenue assessment creates consistency, reduces errors, and improves portfolio performance. These standards should cover the entire process from document collection through final calculation and ongoing monitoring.

Standard operating procedures for revenue calculation ensure every deal receives identical treatment regardless of underwriter, time pressure, or complexity. Written procedures should detail transaction categorization rules, adjustment calculations, seasonal factors, and exception handling. Regular updates keep procedures current with market changes and lessons learned.

Documentation requirements extend beyond basic calculations to create clear audit trails. Every revenue adjustment needs explanation and support. Quality control reviews verify both calculations and judgment calls. This documentation proves invaluable for regulatory exams, investor due diligence, and portfolio analysis.

Quality control checkpoints catch errors before they impact funding decisions. Multi-level reviews, automated validation, and exception reporting create overlapping safeguards. The investment in quality control pays dividends through reduced defaults and regulatory compliance.

Integration with broader risk assessment ensures revenue calculations inform holistic underwriting decisions. True revenue feeds credit models, determines advance sizing, sets payment terms, and triggers monitoring alerts. This integration transforms revenue from a single data point into actionable intelligence.

Documentation Standards

Calculation worksheets provide transparent methodology for every deal. Whether using spreadsheets or automated systems, the path from gross deposits to true revenue must be clear and auditable. Include transaction-level detail for all adjustments, not just summary totals.

Adjustment rationales explain why specific transactions were included or excluded. A $10,000 deposit excluded as a loan proceed needs documentation of the research confirming its non-revenue nature. These rationales protect against second-guessing and provide training examples.

Source verification confirms the authenticity and completeness of analyzed documents. Bank statements should come directly from financial institutions when possible, with appropriate verification of merchant-provided documents. Chain of custody documentation prevents disputes about document handling.

Quality Control Process

Peer review requirements add a second set of eyes to complex calculations. Junior underwriters benefit from senior review, while even experienced staff catch each other's errors. Random sampling of automated calculations ensures system accuracy over time.

Automated validation checks flag impossible or improbable results. Revenue exceeding reasonable industry ranges, perfect mathematical relationships, or sudden changes trigger investigation. These systematic checks catch both errors and fraud attempts.

Exception handling procedures define escalation paths for unusual situations. When standard rules don't apply, clear procedures ensure consistent treatment and appropriate approval levels. Document exceptions thoroughly for future reference and procedure updates.

Technology Integration

API-first architecture enables seamless data flow between systems. Modern MCA underwriting platforms should accept documents via API, return parsed results programmatically, and integrate with existing decision engines. This integration eliminates manual data movement and transcription errors.

Real-time data feeds keep revenue calculations current throughout the relationship. Post-funding monitoring using bank data APIs can flag revenue deterioration before payment problems occur. This proactive approach reduces losses while enabling early intervention.

Automated reporting transforms raw calculations into actionable intelligence. Dashboards showing portfolio-level revenue trends, accuracy metrics, and exception rates enable continuous improvement. Regular reporting identifies training needs, procedure gaps, and technology opportunities.

Frequently Asked Questions

What is the difference between true revenue and gross revenue in MCA underwriting?

True revenue is gross revenue minus returns, refunds, and chargebacks, providing a more accurate picture of actual business income. Gross revenue includes all sales without deductions, which can overestimate repayment capacity.

How do you calculate true revenue from bank statements?

Identify all revenue deposits, subtract returns and refunds, account for chargebacks, and apply seasonal adjustments. Automated parsing tools can categorize transactions and perform these calculations in under 2 minutes.

Why is accurate revenue calculation critical for MCA risk assessment?

Accurate true revenue calculation reduces default rates by 15-25% compared to gross revenue methods. It provides better factor rate pricing and prevents overadvancing to merchants with inflated revenue figures.

What expenses should be deducted from gross revenue for MCA purposes?

Deduct returns, refunds, chargebacks, and any reversed transactions. Processing fees are typically not deducted since they don't affect the merchant's actual income available for advance repayment.

How can automated parsing improve revenue calculation accuracy?

Automated systems consistently categorize transactions, detect fraud patterns, process statements in real-time, and eliminate human calculation errors. They can analyze 27+ fraud signals simultaneously while extracting revenue data.

Ready to Calculate True Revenue in Seconds?

Stop guessing at merchant revenue. ClearStaq's automated revenue calculation gives you accurate true revenue numbers in seconds, not hours.

Frequently Asked Questions

What is the difference between true revenue and gross revenue in MCA underwriting?

True revenue is gross revenue minus returns, refunds, and chargebacks, providing a more accurate picture of actual business income. Gross revenue includes all sales without deductions, which can overestimate repayment capacity.

How do you calculate true revenue from bank statements?

Identify all revenue deposits, subtract returns and refunds, account for chargebacks, and apply seasonal adjustments. Automated parsing tools can categorize transactions and perform these calculations in under 2 minutes.

Why is accurate revenue calculation critical for MCA risk assessment?

Accurate true revenue calculation reduces default rates by 15-25% compared to gross revenue methods. It provides better factor rate pricing and prevents overadvancing to merchants with inflated revenue figures.

What expenses should be deducted from gross revenue for MCA purposes?

Deduct returns, refunds, chargebacks, and any reversed transactions. Processing fees are typically not deducted since they don't affect the merchant's actual income available for advance repayment.

How can automated parsing improve revenue calculation accuracy?

Automated systems consistently categorize transactions, detect fraud patterns, process statements in real-time, and eliminate human calculation errors. They can analyze 27+ fraud signals simultaneously while extracting revenue data.

ClearStaq Team

Product Team

The ClearStaq team builds AI-powered tools for bank statement parsing, fraud detection, and income verification.