Bank statement income verification analyzes deposit patterns over 12-24 months to calculate borrower income when traditional pay stubs aren't available. Lenders examine recurring deposits, exclude non-income transfers, and apply expense deductions to determine qualifying income for self-employed borrowers and alternative lending scenarios.

What you'll learn

- Bank statement income verification serves self-employed borrowers and gig workers who lack traditional W-2 documentation

- Lenders analyze 12-24 months of deposits, excluding transfers and one-time windfalls to calculate true income

- Business expense deductions typically reduce qualifying income by 25-50% depending on industry type

- Automated systems process income verification in minutes versus 2-4 hours for manual analysis

- Advanced fraud detection identifies 27+ manipulation signals including PDF metadata and deposit pattern anomalies

Bank statement income verification analyzes deposit patterns over 12-24 months to calculate borrower income when traditional pay stubs aren't available. Lenders examine recurring deposits, exclude non-income transfers, and apply expense deductions to determine qualifying income for self-employed borrowers and alternative lending scenarios.

What Is Bank Statement Income Verification?

Bank statement income verification has become an essential tool in modern lending, particularly as the workforce shifts toward self-employment and gig economy roles. Instead of relying on traditional W-2 forms or pay stubs, lenders analyze banking transaction data to understand a borrower's true income capacity.

This method examines deposits over an extended period — typically 12 to 24 months — to identify genuine income streams. Unlike traditional verification that relies on employer-provided documentation, bank statement parsing reveals actual cash flow patterns that reflect real-world financial behavior.

The approach has gained significant traction in alternative lending markets, where traditional documentation often fails to capture the complete financial picture. MCA lenders, non-QM mortgage providers, and business loan underwriters increasingly rely on this method to serve borrowers who don't fit conventional lending criteria.

When Traditional Income Documentation Falls Short

Traditional income verification breaks down for several growing segments of the workforce. Self-employed borrowers often show minimal taxable income due to legitimate business deductions, yet maintain healthy cash flows. Their tax returns might show $50,000 in adjusted gross income while their actual cash deposits exceed $150,000 annually.

Seasonal businesses face similar challenges. A landscaping company might generate 80% of annual revenue between April and October, making monthly pay stub verification meaningless. Gig economy workers — from rideshare drivers to freelance consultants — receive income from multiple sources without traditional employment documentation.

These scenarios demand a more nuanced approach to income verification that captures actual money flowing through accounts rather than relying on standardized employment forms.

Types of Lending That Use Bank Statement Verification

MCA lending leads the adoption of bank statement verification, using daily deposit analysis to assess repayment capacity. These lenders care more about consistent cash flow than reported income, making bank statements the primary underwriting document.

Non-QM mortgages represent another major use case. These loans serve borrowers who don't meet qualified mortgage standards but demonstrate clear ability to repay through bank deposits. Lenders typically require 12-24 months of statements to establish income stability.

Business loans increasingly rely on bank statement analysis, especially for newer businesses without extensive financial statements. Personal loans for self-employed individuals also utilize this method when traditional income documentation proves insufficient.

When Bank Statements Are Used for Income Verification

The shift toward bank statement income verification reflects broader changes in how Americans earn money. With over 36% of the U.S. workforce participating in gig work and millions running small businesses, traditional employment verification methods no longer capture the full economic picture.

Lenders have adapted by developing sophisticated methodologies to extract income data from banking transactions. This approach provides advantages for both borrowers and lenders — borrowers gain access to credit despite non-traditional income sources, while lenders get deeper insight into actual cash flow patterns.

Self-Employed and Business Owners

The gap between taxable income and actual cash flow creates the primary use case for bank statement verification among self-employed borrowers. A restaurant owner might show $75,000 in taxable income after deductions for equipment, supplies, and other business expenses, but bank statements reveal $200,000 in gross receipts.

This disparity isn't tax evasion — it's the natural result of legitimate business deductions. Bank statement verification allows lenders to see the full picture, using cash flow analysis to determine true repayment capacity rather than relying solely on net income figures.

Business owners with multiple revenue streams particularly benefit from this approach. A consultant who earns income from speaking engagements, online courses, and client work might receive deposits across several accounts. Bank statement analysis captures all these income sources comprehensively.

MCA and Alternative Lending Applications

Merchant cash advance providers pioneered bank statement income verification out of necessity. Unlike traditional loans based on credit scores and collateral, MCAs advance funds against future revenue. This model requires deep understanding of daily cash flow patterns.

MCA underwriters analyze average daily deposits, identifying patterns that indicate business health. They look for consistency in deposit frequency, amounts, and sources. A coffee shop with steady daily deposits of $1,500-2,000 presents lower risk than one with sporadic large deposits.

Revenue-based lending extends this concept further, tying repayment directly to income percentage. These lenders need accurate income verification to set appropriate repayment terms that align with business cash flow cycles.

Regulatory Compliance Requirements

The Consumer Financial Protection Bureau (CFPB) requires lenders to verify ability to repay for most consumer loans. Bank statements provide documented proof of income that satisfies these requirements when traditional employment verification isn't possible.

Ability-to-repay rules specifically allow for alternative documentation when evaluating self-employed borrowers. Lenders must maintain clear policies for income calculation methods and document their verification processes. Bank statement analysis, when properly implemented, meets these regulatory standards.

State regulations add another layer of compliance requirements. Some states mandate specific calculation methods or minimum documentation periods. Lenders operating across multiple jurisdictions must ensure their bank statement verification processes meet the strictest applicable standards.

How to Calculate Income from Bank Statements

Calculating income from bank statements requires systematic analysis to separate genuine income from other deposits. The process starts with gathering complete statements — gaps in documentation can hide irregular income patterns or suspicious activity.

Most lenders use either 12-month or 24-month averaging methods. The 12-month approach works well for stable businesses, while 24-month averaging better captures seasonal variations. Some lenders apply weighted averages, giving more recent months greater influence on the final calculation.

The fundamental challenge lies in distinguishing income deposits from transfers, loans, and other non-income transactions. Automated expense categorization helps separate business revenue from other deposit types, ensuring accurate income calculations.

Identifying Qualifying Income Deposits

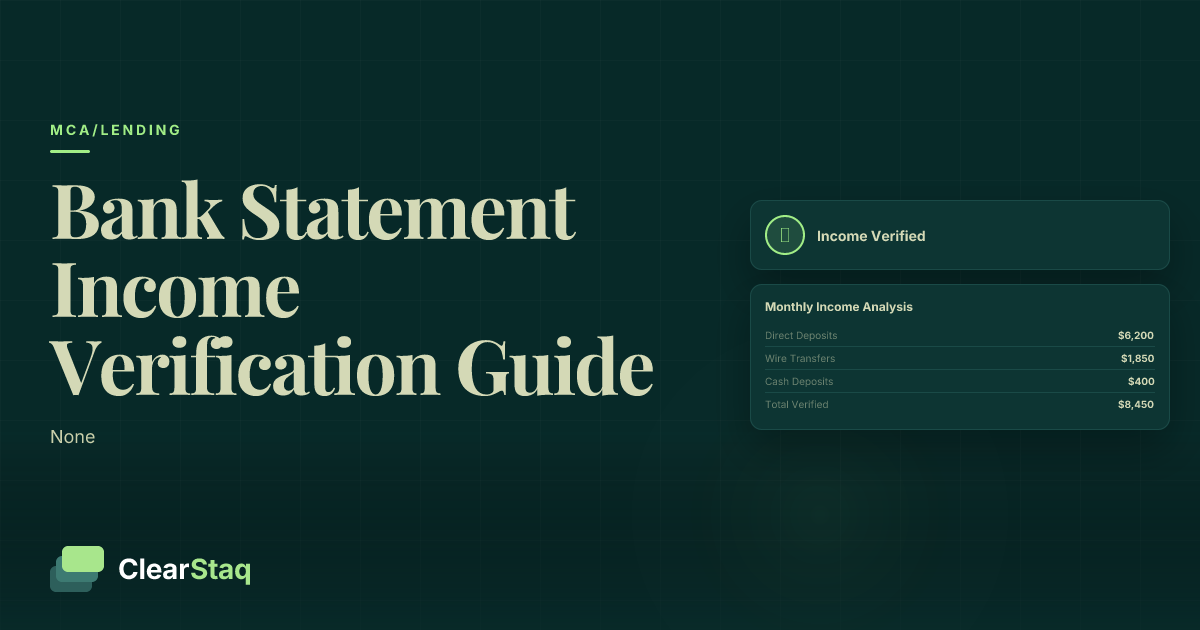

Business revenue deposits form the primary income source for self-employed borrowers. These include customer payments, merchant processing settlements, and cash deposits from daily operations. Identifying these requires pattern recognition — business deposits typically follow consistent schedules and amount ranges.

Salary and wage deposits appear as regular transfers from employers, usually matching specific amounts on predictable dates. Even for business owners who pay themselves irregularly, these owner draws count as qualifying income when properly documented.

Recurring income patterns help validate deposit sources. A freelance designer receiving monthly retainer payments of $5,000 from three clients shows clear income patterns. Rental income, investment distributions, and other passive income sources also qualify when they demonstrate consistency.

Excluding Non-Income Transactions

Accurate income calculation requires removing non-income deposits that inflate the numbers. Transfers between accounts represent the most common exclusion — moving $10,000 from savings to checking doesn't constitute income.

Loan proceeds must be identified and excluded. A $50,000 business loan deposit would dramatically skew income calculations if included. These typically appear as large, one-time deposits from financial institutions.

One-time windfalls like insurance settlements, asset sales, or gifts don't reflect ongoing income capacity. While a $25,000 insurance payout helps current finances, it doesn't indicate ability to make regular loan payments.

Calculating Net Qualifying Income

Gross deposit analysis provides only part of the picture. Lenders must account for business expenses to determine actual available income. This process varies by lender and loan type.

Business expense deductions typically range from 25% to 50% of gross deposits, depending on industry. A restaurant with high food and labor costs might see 40% expense ratios, while consultants operate with 20% ratios.

Standard percentage methods offer quick calculations — many lenders simply apply industry-standard expense ratios. Actual expense analysis provides more accuracy by categorizing outgoing transactions, but requires more sophisticated processing.

As shown in the income calculation demonstration above, different methodologies can produce varying results. Choosing the right approach depends on business type, loan purpose, and risk tolerance.

Required Documentation and Time Periods

Documentation requirements for bank statement income verification vary significantly across loan types and lenders. While some MCA providers accept as few as three months of statements, mortgage lenders typically require 12 to 24 months to establish income stability.

The distinction between personal and business bank statements adds complexity. Many self-employed borrowers mix personal and business finances, requiring analysis of multiple accounts to capture complete income pictures. Seasonal businesses need longer documentation periods to show full annual cycles.

Personal Bank Statement Requirements

Individual account statements must include all pages, showing beginning and ending balances for each month. Missing pages raise red flags and can delay or derail loan approval. Digital statements should be original PDFs from the bank, not scanned copies.

Joint account considerations require additional documentation to establish ownership percentages. Lenders need written confirmation from all account holders about income attribution. A married couple sharing accounts might split income 50/50, or attribute specific deposits to one spouse.

Multiple account aggregation becomes necessary when borrowers spread income across several accounts. A freelancer might receive ACH payments in one account, wire transfers in another, and deposit checks in a third. Complete income verification requires statements from all accounts receiving income.

Business Bank Statement Requirements

Business checking accounts provide the clearest income picture for established companies. These accounts should separate business transactions from personal finances, making income identification straightforward. However, many small business owners still commingle funds.

Merchant processing statements supplement bank statements for retail and restaurant businesses. These show credit card sales that might appear as lump sum deposits in bank accounts. Matching processing statements to bank deposits prevents double-counting income.

Multiple entity considerations affect business owners with several companies. Income might flow through multiple EINs before reaching the owner. Lenders need statements from all related entities to track income paths and avoid missing or duplicating revenue.

Time Period Requirements by Loan Type

MCA lending typically requires 3-12 months of statements, focusing on recent cash flow trends rather than long-term stability. These lenders prioritize current business performance over historical data.

Mortgage lending demands 12-24 months to satisfy investor requirements and demonstrate stable income patterns. Self-employed borrowers usually need 24 months to account for income variability.

Business term loans fall between these extremes, usually requiring 6-12 months. Established businesses might qualify with six months, while startups need longer histories to prove viability.

Red Flags and Fraud Detection in Income Verification

Income manipulation represents one of the most common forms of lending fraud. Desperate borrowers alter statements to qualify for loans they can't afford, creating risk for lenders and ultimately harming their own financial futures.

Modern fraud detection goes beyond simple document review. Sophisticated analysis examines transaction patterns, document metadata, and mathematical relationships within statements. Understanding these 27 fraud detection signals helps lenders protect their portfolios while serving legitimate borrowers.

Income Inflation Red Flags

Unusually round deposits often indicate manipulation. Real business income rarely arrives in perfect $5,000 or $10,000 amounts. When multiple deposits show suspiciously round numbers, it suggests someone manually added transactions.

Sudden income spikes without corresponding business changes raise concerns. A landscaping business showing $5,000 monthly deposits suddenly jumping to $20,000 needs explanation. Legitimate growth happens gradually, not overnight.

Inconsistent deposit timing reveals potential fraud. Real customers don't all pay on the same day each month. Deposits showing perfect weekly or monthly patterns suggest fabrication rather than actual business activity.

Document Manipulation Signs

Altered PDF metadata provides definitive fraud evidence. Every PDF contains creation and modification timestamps. When these don't match the bank's typical patterns, it indicates post-production editing.

Font inconsistencies appear when fraudsters add or modify transactions. Banks use consistent fonts throughout their statements. Mixed fonts, slightly different sizes, or misaligned text reveal tampering.

Balance calculation errors expose amateur fraud attempts. Each transaction should mathematically connect to running balances. When deposits don't properly add to balances, it shows manual manipulation without recalculating totals.

Advanced Fraud Detection Techniques

Pattern analysis algorithms examine transaction behavior across thousands of data points. AI-powered fraud detection identifies subtle anomalies humans miss, like deposits that don't match typical merchant processing schedules.

Cross-reference verification compares stated income against known benchmarks. A small coffee shop claiming $50,000 monthly revenue exceeds industry norms, triggering deeper investigation.

Real-time fraud scoring evaluates multiple risk factors simultaneously, generating probability scores for document authenticity. High-risk applications receive additional scrutiny before approval.

The fraud detection demonstration above shows how multiple signals combine to assess document authenticity. No single indicator confirms fraud — the combination of multiple red flags drives risk decisions.

Automated vs Manual Income Verification

The traditional manual review process for bank statement income verification consumes significant time and resources. Underwriters spend hours calculating deposits, categorizing transactions, and checking for fraud indicators. This manual approach limits lending volume and introduces human error.

Automation transforms this process from hours to minutes while improving accuracy. Modern systems process statements from 900+ bank format support providers, ensuring comprehensive coverage regardless of where borrowers bank.

Manual Income Verification Challenges

Time-intensive analysis represents the primary manual review limitation. An experienced underwriter needs 2-4 hours to properly analyze 12 months of statements, including deposit categorization, income calculation, and fraud checking.

Human error potential increases with document volume. Calculating hundreds of transactions across multiple statements invites mistakes. A single transcription error can significantly impact income calculations and loan decisions.

Inconsistent methodologies emerge when multiple underwriters apply different standards. One might exclude certain deposits another includes, leading to different income calculations for identical statements.

See ClearStaq's Automated Income Verification in Action

Upload a bank statement and see instant income analysis with automated calculations and fraud detection. Start your free trial — no credit card required.

Automated Processing Benefits

Instant income calculation revolutionizes underwriting workflows. Systems process 12 months of statements in under 60 seconds, extracting transactions, categorizing deposits, and calculating income using consistent methodologies.

Standardized methodologies ensure every application receives identical treatment. Automated systems apply the same rules to every statement, eliminating subjective interpretation and ensuring fair lending practices.

Scalable processing enables lenders to handle volume spikes without adding staff. Whether processing 10 or 1,000 applications daily, automated systems maintain consistent speed and accuracy.

API Integration Capabilities

Real-time verification through API integration eliminates document handling entirely. Borrowers authorize direct bank connections, allowing instant access to transaction data without uploading statements.

Seamless workflow integration embeds income verification within existing loan origination systems. APIs pass calculated income directly to decision engines, eliminating manual data entry.

Developer-friendly implementation makes integration straightforward. Modern APIs offer comprehensive documentation, SDKs in multiple languages, and sandbox environments for testing.

6 fields extracted automatically • 99.8% accuracy

The automated extraction process shown above demonstrates how quickly systems can transform raw bank statements into actionable income data, enabling faster lending decisions.

Best Practices for Lenders and Underwriters

Establishing robust income verification processes protects lenders while serving borrowers fairly. Success requires balancing thorough analysis with efficient operations, maintaining compliance while meeting business objectives.

Leading lenders develop comprehensive policies covering calculation methods, exception handling, and quality control. These standards ensure consistent treatment across all applications while adapting to unique borrower situations.

Income Calculation Standardization

Consistent averaging methods prevent confusion and ensure fairness. Lenders should document whether they use simple averages, weighted averages, or other methodologies. Once established, apply these methods uniformly.

Standardized exclusion criteria clarify which deposits count toward income. Create detailed lists of excluded transaction types — transfers, loans, refunds, reimbursements — and train staff to identify them consistently.

Documentation requirements must be clear and consistently enforced. Specify exact statement requirements including time periods, account types, and acceptable formats. Communicate these upfront to prevent delays.

Quality Control Procedures

Secondary review processes catch errors before loan funding. Randomly audit 10-20% of approved applications, checking calculation accuracy and policy compliance. Track error rates to identify training needs.

Exception handling procedures address unique situations systematically. Document how to handle partial months, missing pages, or unusual deposit patterns. Clear escalation paths prevent bottlenecks.

Audit trail maintenance protects against regulatory scrutiny. Document every calculation, exclusion, and override decision. Modern systems automatically capture this data, but manual processes need careful documentation.

Risk Assessment Integration

Income stability analysis goes beyond simple averaging. Examine month-to-month variance, seasonal patterns, and trend lines. Declining income trends might warrant lower loan amounts despite acceptable averages.

Debt-to-income calculations using bank statement income require careful consideration. The MCA underwriting process often uses debt service coverage ratios instead of traditional DTI metrics.

Cash flow trend evaluation predicts future performance. Growing businesses show increasing deposits over time, while struggling operations display declining trends. Weight recent performance appropriately in decisions.

For comprehensive MCA lending solutions, automated income verification becomes essential for competitive operations.

Regulatory Compliance and Guidelines

Income verification requirements stem from multiple regulatory sources, each adding specific obligations. The regulatory landscape continues evolving as alternative documentation methods gain acceptance.

Compliance requires understanding federal mandates, GSE guidelines, and state regulations. Lenders must maintain current knowledge of all applicable requirements while implementing systems to ensure adherence.

Federal Regulatory Requirements

CFPB ATR rule compliance mandates verifying borrower ability to repay most consumer loans. Bank statements qualify as income verification when properly analyzed and documented. The key lies in using reasonable, good-faith methods to determine income.

Fair lending considerations require consistent treatment of all applicants. If bank statements are accepted for one self-employed borrower, similar accommodation must extend to all qualified applicants. Document policies clearly to demonstrate compliance.

Documentation standards under federal regulations require retaining income verification records. Keep original statements, calculation worksheets, and decision documentation for required retention periods — typically five to seven years.

GSE Guidelines for Bank Statement Loans

Fannie Mae requirements allow bank statement income verification for self-employed borrowers under specific programs. These guidelines specify 12 or 24-month documentation periods and particular calculation methods.

Freddie Mac standards similarly accommodate bank statement documentation with detailed requirements. Both GSEs regularly update guidelines, requiring lenders to monitor changes.

Investor overlays often add requirements beyond GSE minimums. Many investors require 24 months of statements even when GSEs allow 12, or mandate specific expense ratios for income calculations.

State and Local Compliance

State licensing requirements may include specific income verification mandates. Some states require licensed loan officers to personally review income documentation, limiting full automation.

Disclosure obligations vary by jurisdiction. Certain states mandate explaining income calculation methods to borrowers, including how deposits were categorized and expenses deducted.

Consumer protection laws at state levels add additional requirements. These might include cooling-off periods, additional disclosures, or specific calculation methods for determining income.

Common Challenges and Solutions

Real-world income verification rarely follows textbook examples. Borrowers present complex situations requiring flexible yet consistent approaches to accurate income determination.

Successful lenders anticipate common challenges and develop systematic solutions. This preparation prevents delays while ensuring accurate income calculations across diverse borrower profiles.

Handling Irregular and Seasonal Income

Seasonal business adjustments require analyzing full annual cycles. A tax preparation service earning 70% of revenue during January-April needs different treatment than steady-state businesses. Use 24-month averages to capture complete seasons.

Trend analysis techniques help separate temporary fluctuations from permanent changes. Moving averages smooth monthly variations while highlighting underlying trends. Weight recent months appropriately without overreacting to short-term changes.

Multiple year comparisons reveal growth patterns obscured by seasonal variations. Comparing April this year to April last year provides clearer insight than comparing April to March.

Multiple Account Aggregation

Cross-account income tracking prevents missing or duplicating deposits. Create matrices showing money movement between accounts, identifying true external income versus internal transfers.

Duplicate deposit identification requires careful analysis. A $10,000 check deposited via mobile app might appear twice — once as pending, again when cleared. Automated systems excel at catching these duplications.

Consolidated income reporting combines multiple accounts into unified income figures. Present clear summaries showing income by source and account, with supporting detail for verification.

Mixed Fund Challenges

Personal vs business separation in commingled accounts demands careful analysis. Look for patterns — business deposits often follow different schedules than personal income. Grocery purchases indicate personal use, while inventory purchases suggest business expenses.

Commingled account analysis uses transaction patterns to allocate income and expenses. Regular transfers to personal accounts might represent owner draws, while business expenses reduce net income calculations.

Income source verification confirms deposit origins when account activity mixes multiple sources. Match deposits to invoices, contracts, or other documentation proving business revenue versus personal funds.

Frequently Asked Questions

How do you verify income from bank statements?

Income is verified by analyzing 12-24 months of bank statements to identify recurring deposits, calculate average monthly income, and deduct business expenses. Automated tools can process this analysis in minutes rather than hours.

What percentage of deposits should be counted as income?

Typically 50-75% of business deposits are counted as income after expense deductions, though the exact percentage depends on industry type and lender guidelines. Personal salary deposits usually count at 100%.

How many months of bank statements are needed for income verification?

Most lenders require 12-24 months for mortgage loans, 6-12 months for business loans, and 3-12 months for MCA lending, depending on income stability and loan type.

Can business bank statements be used for personal income verification?

Yes, business bank statements can verify personal income for business owners by analyzing owner draws, distributions, and salary payments from the business to the owner.

How does automated income verification work?

Automated systems use AI to extract transaction data, categorize deposits and expenses, identify income patterns, and calculate qualifying income using standardized methodologies across 900+ bank formats.

Ready to Transform Your Income Verification Process?

Transform your income verification process with automated analysis, fraud detection, and instant calculations. Start your free trial today.

Frequently Asked Questions

How do you verify income from bank statements?

Income is verified by analyzing 12-24 months of bank statements to identify recurring deposits, calculate average monthly income, and deduct business expenses. Automated tools can process this analysis in minutes rather than hours.

What percentage of deposits should be counted as income?

Typically 50-75% of business deposits are counted as income after expense deductions, though the exact percentage depends on industry type and lender guidelines. Personal salary deposits usually count at 100%.

How many months of bank statements are needed for income verification?

Most lenders require 12-24 months for mortgage loans, 6-12 months for business loans, and 3-12 months for MCA lending, depending on income stability and loan type.

Can business bank statements be used for personal income verification?

Yes, business bank statements can verify personal income for business owners by analyzing owner draws, distributions, and salary payments from the business to the owner.

How does automated income verification work?

Automated systems use AI to extract transaction data, categorize deposits and expenses, identify income patterns, and calculate qualifying income using standardized methodologies across 900+ bank formats.

ClearStaq Team

Product Team

The ClearStaq team builds AI-powered tools for bank statement parsing, fraud detection, and income verification.