What you'll learn

- Average daily balance should exceed 10% of monthly revenue.

- More than 3 NSF fees per month raises red flags; more than 5 per month triggers decline at most MCA firms.

- True revenue requires subtracting transfers, loan proceeds, and internal movements from total deposits.

- MCA stacking detection identifies existing positions through recurring ACH debits matching known funder patterns.

- Deposit concentration above 50% from a single source exposes the merchant to revenue collapse.

- Owner withdrawals exceeding 30% of net revenue indicate the business prioritizes personal draws over operational stability.

- Automated parsing platforms extract all ten checklist metrics in under 5 seconds across 900+ bank formats with 99.7% accuracy.

- A financial scorecard covering 7 risk dimensions replaces subjective judgment calls with data-driven underwriting decisions.

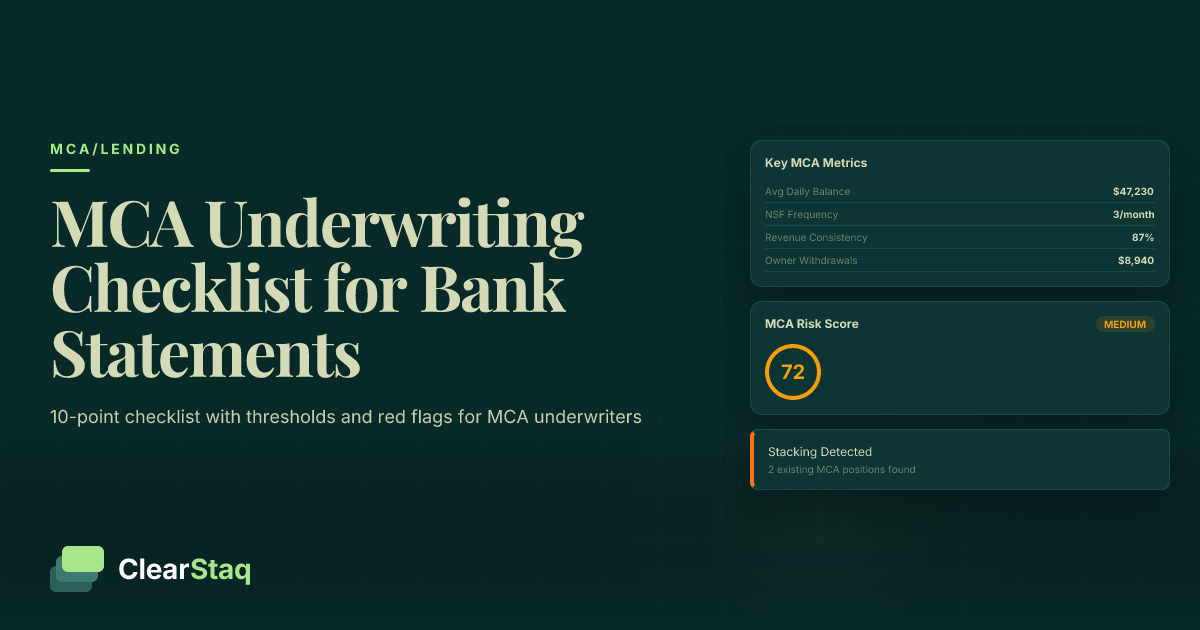

MCA underwriters review bank statements for ten core metrics: average daily balance, revenue consistency, NSF frequency, existing MCA positions (stacking), seasonal patterns, owner withdrawals, deposit concentration, true revenue, fraud indicators, and credit-to-debit ratios. Each metric carries specific thresholds that separate fundable merchants from high-risk applicants. Automated parsing extracts these metrics in seconds.

You'll Learn

- The ten bank statement metrics that predict MCA repayment capacity

- Specific threshold numbers that trigger approval, review, or decline

- How to detect MCA stacking from transaction patterns

- Red flags that signal fraudulent or manipulated statements

- How to calculate true revenue by filtering transfers and loans

- Tools that automate the entire checklist in under 5 seconds

MCA Underwriting Defined

MCA underwriting evaluates whether a business can repay a merchant cash advance from future receivables. Unlike traditional lending, MCA underwriting centers on cash flow analysis rather than credit scores. Bank statements provide the primary evidence.

A strong underwriter reviews 3-6 months of bank statements and reaches a funding decision within minutes. The checklist below covers the ten areas that matter most.

1. Average Daily Balance Analysis

Average daily balance (ADB) measures how much cash the business maintains on a given day. Calculate it by summing each day's ending balance across the statement period and dividing by the number of days.

ADB reveals more than opening or closing balances alone. A merchant might show $40,000 at month's start and $38,000 at month's end, but if the balance drops to $500 on day 15, the averages mask a cash flow crisis.

Thresholds to Apply

- Strong: ADB above 15% of monthly revenue

- Acceptable: ADB between 10-15% of monthly revenue

- Caution: ADB below 10% of monthly revenue

- Decline trigger: More than 5 negative balance days per month

A restaurant depositing $80,000 per month with an ADB of $12,000 (15%) manages cash well. The same restaurant with a $4,000 ADB (5%) runs on fumes. That merchant will struggle to meet daily remittance obligations when a slow week hits.

2. Revenue Consistency and Trends

Compare monthly deposit totals across the statement period. Look for growth, stability, or decline. A business with $100,000 in month one, $95,000 in month two, and $105,000 in month three shows stable revenue. A drop from $100,000 to $60,000 to $40,000 shows a business in trouble.

Patterns to Flag

- Month-over-month decline exceeding 15%: Investigate the cause before approving

- Revenue growth above 50% in one month: Verify the source — could indicate loan proceeds misclassified as revenue

- Revenue variance exceeding 30% between months: Indicates volatility that complicates repayment projections

Stable revenue supports predictable remittance. Volatile revenue forces underwriters to model worst-case scenarios when calculating advance amounts and hold-back percentages.

3. NSF Fees and Overdraft Frequency

NSF (non-sufficient funds) fees signal that the business authorizes payments it cannot cover. Each NSF fee represents a failed obligation. Clusters of NSF fees in consecutive weeks indicate chronic cash shortfalls.

Claim: NSF frequency predicts MCA repayment risk.

Stat: Merchants with 5+ NSF occurrences per month default on MCA obligations at 3x the rate of merchants with zero NSFs, according to industry data compiled by deBanked.

Source: deBanked MCA Industry Reports

NSF Scoring Guide

- 0-2 per month: Acceptable for most funders

- 3-4 per month: Requires explanation — seasonal dip or management issue?

- 5+ per month: High risk — most funders decline or require additional collateral

Count overdraft fees separately. Banks that extend overdraft protection prevent the NSF but charge a different fee. Both fee types reveal the same underlying problem: the account lacks funds to cover obligations.

4. Existing MCA Position Detection (Stacking)

Stacking occurs when a merchant holds multiple active MCA positions from different funders. Each position reduces the cash available for new remittance obligations. A merchant with two existing positions and 40% of daily revenue going to MCA payments has limited capacity for a third advance.

Detection Methods

Look for these transaction patterns:

- Recurring ACH debits with funder names: Search for company names matching known MCA funders (e.g., "YELLOWSTONE CAPITAL," "FORWARD FINANCING," "LIBERTAS")

- Fixed-amount daily debits: A $350 withdrawal at the same time each business day suggests a fixed daily remittance

- Multiple small debits on the same day: Three or four ACH debits of $200-$500 each on the same day indicate multiple positions

- Percentage-based variable debits: Debits that fluctuate in proportion to daily deposits suggest a percentage-based hold-back

ClearStaq's automated MCA stacking detection scans every transaction against a database of known funder names and remittance patterns. The system flags existing positions and estimates remaining balances based on payment frequency and amounts.

5. Seasonal Patterns and Cash Flow Cycles

Seasonal businesses present unique underwriting challenges. A landscaping company deposits $120,000 in July and $30,000 in January. A tax preparation firm generates 70% of annual revenue between February and April.

Seasonal Assessment Steps

- Compare current statement period to the same period in prior years (if available)

- Identify the merchant's peak and trough months

- Calculate the advance amount against trough-month revenue, not peak

- Structure remittance terms to accommodate seasonal drops

Underwriting a seasonal business during peak season creates a false picture of repayment capacity. A $100,000 advance approved in August, based on $150,000 in monthly revenue, becomes a burden when December revenue drops to $40,000 and daily remittance remains constant.

Automate Your Underwriting Checklist

ClearStaq extracts all ten checklist metrics from bank statements in under 5 seconds. The platform generates a financial scorecard with 7 risk dimensions, detects MCA stacking, and runs 27 fraud signals across every document.

6. Owner Withdrawals vs. Business Expenses

Separate owner draws from operating expenses. Large or frequent owner withdrawals indicate the business prioritizes personal compensation over operational stability. This pattern increases repayment risk.

Ratios to Monitor

- Owner draws under 20% of net revenue: Typical for stable businesses reinvesting in growth

- Owner draws between 20-30% of net revenue: Acceptable for established businesses with consistent cash flow

- Owner draws exceeding 30% of net revenue: Red flag — the owner extracts cash faster than the business generates it

Look for patterns: a $15,000 transfer to a personal account every two weeks, ATM withdrawals totaling $5,000+ per month, or Venmo/Zelle payments to the owner's personal accounts. These all reduce the cash available for MCA remittance.

Also compare owner withdrawals to payroll. An owner paying themselves $25,000 per month while employees earn $12/hour raises questions about business sustainability.

7. Deposit Concentration Risk

Deposit concentration measures how much revenue comes from a single source. A business receiving 80% of deposits from one customer operates with fragile income. Losing that customer eliminates most of the revenue backing the advance.

Concentration Thresholds

- No single source above 25%: Diversified — lower concentration risk

- One source between 25-50%: Moderate risk — assess the stability of that relationship

- One source above 50%: High concentration risk — the advance depends on a single relationship

Identify the deposit sources. "STRIPE TRANSFER" appearing for 90% of deposits tells you the merchant runs an e-commerce business through one payment processor. "ABC CONSTRUCTION CO" appearing as the only large deposit source means one client funds the entire operation.

Concentration risk doesn't disqualify a merchant. A medical practice receiving 60% of deposits from one insurance network holds a stable, contractual relationship. A subcontractor receiving 80% from one general contractor faces termination risk with each project completion.

8. True Revenue Calculation

Total deposits overstate business income. Transfers between the merchant's own accounts, loan proceeds, tax refunds, insurance settlements, and credit card cash advances inflate the deposit total without representing earned revenue.

Deposits to Exclude

- Internal transfers: "TRANSFER FROM SAVINGS," "MOBILE DEPOSIT — OWN CHECK," movements between accounts at the same bank

- Loan proceeds: SBA deposits, line of credit draws, MCA funding deposits (large lump sums from known funders)

- Tax refunds: IRS deposits, state tax refunds

- Insurance payouts: Claim settlement deposits

- Credit card cash advances: Cash advance deposits that create new debt obligations

- Returned item redeposits: Items deposited, returned, and redeposited inflate the count

A merchant showing $500,000 in total 3-month deposits might have $350,000 in true revenue after removing $80,000 in transfers, $50,000 in loan proceeds, and $20,000 in tax refunds. Underwriting against $500,000 instead of $350,000 leads to advances the business cannot support.

Automated bank statement parsing categorizes each deposit at extraction time, separating revenue from non-revenue items. ClearStaq's financial analysis outputs true revenue as a distinct metric.

9. Red Flags That Signal Fraud

Fraudulent bank statements cost MCA funders millions per year. Organized fraud rings submit manipulated or fabricated statements to obtain advances they never intend to repay.

Document-Level Red Flags

- PDF metadata shows editing software: Adobe Illustrator, Photoshop, or similar tools in the document properties indicate manipulation

- Font inconsistencies: Different fonts or sizes on the same page suggest edited values

- Mathematical errors: Running balances that don't reconcile with transaction amounts prove the numbers were changed

- Missing or inconsistent headers: Statement headers that differ between pages or don't match the bank's template

- Image artifacts: Blurring, pixelation, or color differences around specific transaction amounts

Behavioral Red Flags

- Round-number deposits: Businesses receive $4,287.53 from credit card processing, not $5,000.00. Consistent round deposits suggest fabrication

- Deposit clustering: All deposits landing on the same day of the week without business justification

- Revenue inconsistent with business type: A small dry cleaner showing $200,000 in monthly deposits

- Sudden revenue spikes: Revenue doubling in the month before application without explanation

- Identical transaction descriptions: Copy-pasted transaction lines with identical wording across different dates

ClearStaq's fraud detection runs 27 signals across both document integrity and behavioral analysis. The system catches manipulation that human reviewers miss: metadata anomalies, mathematical inconsistencies, and statistical patterns that indicate synthetic data.

10. Credit vs. Debit Ratio Analysis

The ratio between total credits (deposits) and total debits (withdrawals) reveals operating margin at the bank account level. A healthy business deposits more than it withdraws, building reserves over time.

Ratio Benchmarks

- Credits exceed debits by 10%+: Business builds cash reserves — strong indicator

- Credits roughly equal debits (within 5%): Business operates at breakeven — manageable with careful structuring

- Debits exceed credits: Business burns cash — the account balance declines each month, signaling inability to support additional obligations

A credit-to-debit ratio below 1.0 across consecutive months means the business spends more than it earns at the bank account level. Adding an MCA remittance obligation accelerates the cash drain.

Break the ratio down by month. A 3-month average of 1.05 looks acceptable, but if the ratio moves from 1.15 in month one to 1.05 in month two to 0.95 in month three, the trend shows deterioration.

Putting the Checklist Together

Each metric tells part of the story. The full picture requires all ten.

| Checklist Item | Strong Signal | Caution Signal | Decline Signal |

|---|---|---|---|

| Average Daily Balance | Above 15% of monthly revenue | 10-15% of monthly revenue | Below 10% or 5+ negative days |

| Revenue Trend | Stable or growing | Variance under 15% month-to-month | Decline exceeding 15% per month |

| NSF/Overdraft Fees | 0-2 per month | 3-4 per month | 5+ per month |

| MCA Stacking | No existing positions | 1 position with low remittance | 2+ positions or high total remittance |

| Seasonal Impact | Underwritten against trough revenue | Moderate seasonal swing (30-50%) | Trough revenue below remittance capacity |

| Owner Withdrawals | Under 20% of net revenue | 20-30% of net revenue | Above 30% of net revenue |

| Deposit Concentration | No source above 25% | One source 25-50% | One source above 50% |

| True Revenue Accuracy | Transfers/loans under 10% of deposits | Transfers/loans 10-25% of deposits | Transfers/loans above 25% of deposits |

| Fraud Signals | Zero flags | 1 minor flag (review required) | Multiple flags or any document integrity failure |

| Credit/Debit Ratio | Above 1.10 | 1.00-1.10 | Below 1.00 |

A merchant with six or more "strong" signals and zero "decline" signals represents a straightforward approval. Merchants with mixed signals require experienced underwriter judgment on advance amount, factor rate, and remittance structure.

Automating the Checklist with ClearStaq

Running this ten-point checklist by hand takes 30-45 minutes per application. An underwriter processing 50 applications per day cannot complete this analysis for each one. Shortcuts happen. Metrics get skipped. Risk gets missed.

ClearStaq automates the entire checklist. Upload a bank statement set and receive a financial scorecard covering 7 risk dimensions in under 5 seconds. The platform:

- Parses bank statements with 99.7% accuracy across 900+ bank formats

- Calculates average daily balance, true revenue, and credit-to-debit ratios

- Counts NSF fees and negative balance days

- Detects MCA stacking through automated transaction pattern matching

- Runs 27 fraud detection signals across document integrity and behavioral analysis

- Categorizes deposits to separate revenue from transfers, loans, and internal movements

- Flags owner withdrawals and calculates withdrawal-to-revenue ratios

Underwriters review a one-page scorecard instead of scrolling through hundreds of transactions. Time shifts from data extraction to decision-making. Teams using ClearStaq review 3-5x more applications per day while catching risk signals that manual review misses.

Start your free trial and run the full checklist on your first statement set in minutes.

Key Takeaways

- Average daily balance should exceed 10% of monthly revenue — below this threshold signals tight cash flow and higher repayment risk.

- More than 3 NSF fees per month raises red flags; more than 5 per month triggers decline at most MCA firms.

- True revenue requires subtracting transfers, loan proceeds, and internal movements from total deposits — raw deposit totals overstate business income.

- MCA stacking detection identifies existing positions through recurring ACH debits matching known funder patterns and fixed-amount daily or weekly withdrawals.

- Deposit concentration above 50% from a single source exposes the merchant to revenue collapse if that relationship ends.

- Owner withdrawals exceeding 30% of net revenue indicate the business prioritizes personal draws over operational stability.

- Automated parsing platforms like ClearStaq extract all ten checklist metrics in under 5 seconds across 900+ bank formats with 99.7% accuracy.

- A financial scorecard covering 7 risk dimensions replaces subjective judgment calls with data-driven underwriting decisions.

Frequently Asked Questions About MCA Underwriting

What do MCA underwriters look for in bank statements?

MCA underwriters analyze average daily balance, monthly revenue trends, NSF and overdraft frequency, existing MCA positions, deposit consistency, owner withdrawal ratios, and fraud indicators. They calculate true revenue by subtracting transfers, loan proceeds, and internal movements from total deposits. A strong applicant shows stable or growing revenue, fewer than 3 NSF fees per month, and an average daily balance above 10% of monthly revenue.

How do underwriters detect MCA stacking in bank statements?

Underwriters look for recurring ACH debits with names matching known MCA funders, daily or weekly fixed-amount withdrawals that match typical MCA remittance patterns, and multiple small debits occurring on the same day. ClearStaq's automated stacking detection scans for these patterns across 900+ bank formats and flags existing positions with funder names and estimated remaining balances.

What is a good average daily balance for MCA approval?

Most MCA funders want an average daily balance above 10% of monthly revenue. A business depositing $100,000 per month should maintain at least $10,000 in average daily balance. Balances below this threshold signal tight cash management and higher repayment risk. Negative balance days exceeding 5 per month often trigger automatic declines.

How many NSF fees are too many for MCA underwriting?

More than 3 NSF fees per month raises concern for most MCA funders. More than 5 per month triggers decline at many firms. NSF fees signal that the business writes checks or authorizes payments without sufficient funds, which predicts future difficulties meeting daily or weekly MCA remittance obligations.

How do you calculate true revenue from bank statements?

Subtract transfers between the merchant's own accounts, loan proceeds, tax refunds, insurance payouts, and internal movements from total deposits. The remainder represents actual business revenue. A merchant showing $500,000 in total deposits might have only $300,000 in true revenue after removing $150,000 in transfers and $50,000 in loan proceeds.

What bank statement red flags indicate fraud?

Red flags include round-number deposits inconsistent with the business type, deposits clustered on specific days without business justification, running balances that don't reconcile mathematically, PDF metadata showing editing software, font inconsistencies across pages, and sudden revenue spikes without corresponding business activity. ClearStaq checks 27 fraud signals across document integrity and behavioral patterns.

Can software automate MCA bank statement underwriting?

Yes. Platforms like ClearStaq parse bank statements in under 5 seconds with 99.7% accuracy, extract all ten checklist metrics, detect MCA stacking, run 27 fraud signals, and generate a financial scorecard with 7 risk dimensions. Underwriters review a one-page summary instead of scrolling through hundreds of transactions. Teams using automated parsing review 3-5x more applications per day.

Run the Full Underwriting Checklist in 5 Seconds

ClearStaq automates every metric on this checklist: daily balances, NSF counts, stacking detection, true revenue, fraud analysis, and more. Upload a statement set and receive a complete financial scorecard across 7 risk dimensions.

Frequently Asked Questions

What do MCA underwriters look for in bank statements?

MCA underwriters analyze average daily balance, monthly revenue trends, NSF and overdraft frequency, existing MCA positions, deposit consistency, owner withdrawal ratios, and fraud indicators. They calculate true revenue by subtracting transfers, loan proceeds, and internal movements from total deposits. A strong applicant shows stable or growing revenue, fewer than 3 NSF fees per month, and an average daily balance above 10% of monthly revenue.

How do underwriters detect MCA stacking in bank statements?

Underwriters look for recurring ACH debits with names matching known MCA funders, daily or weekly fixed-amount withdrawals that match typical MCA remittance patterns, and multiple small debits occurring on the same day.

What is a good average daily balance for MCA approval?

Most MCA funders want an average daily balance above 10% of monthly revenue. A business depositing $100,000 per month should maintain at least $10,000 in average daily balance.

How many NSF fees are too many for MCA underwriting?

More than 3 NSF fees per month raises concern for most MCA funders. More than 5 per month triggers decline at many firms.

How do you calculate true revenue from bank statements?

Subtract transfers between the merchant's own accounts, loan proceeds, tax refunds, insurance payouts, and internal movements from total deposits. The remainder represents actual business revenue.

What bank statement red flags indicate fraud?

Red flags include round-number deposits inconsistent with the business type, deposits clustered on specific days without business justification, running balances that don't reconcile mathematically, PDF metadata showing editing software, and font inconsistencies across pages.

Can software automate MCA bank statement underwriting?

Yes. Platforms like ClearStaq parse bank statements in under 5 seconds with 99.7% accuracy, extract all ten checklist metrics, detect MCA stacking, run 27 fraud signals, and generate a financial scorecard with 7 risk dimensions.

ClearStaq Team

Document Intelligence Platform

The ClearStaq team builds AI-powered tools for bank statement parsing, fraud detection, and income verification.