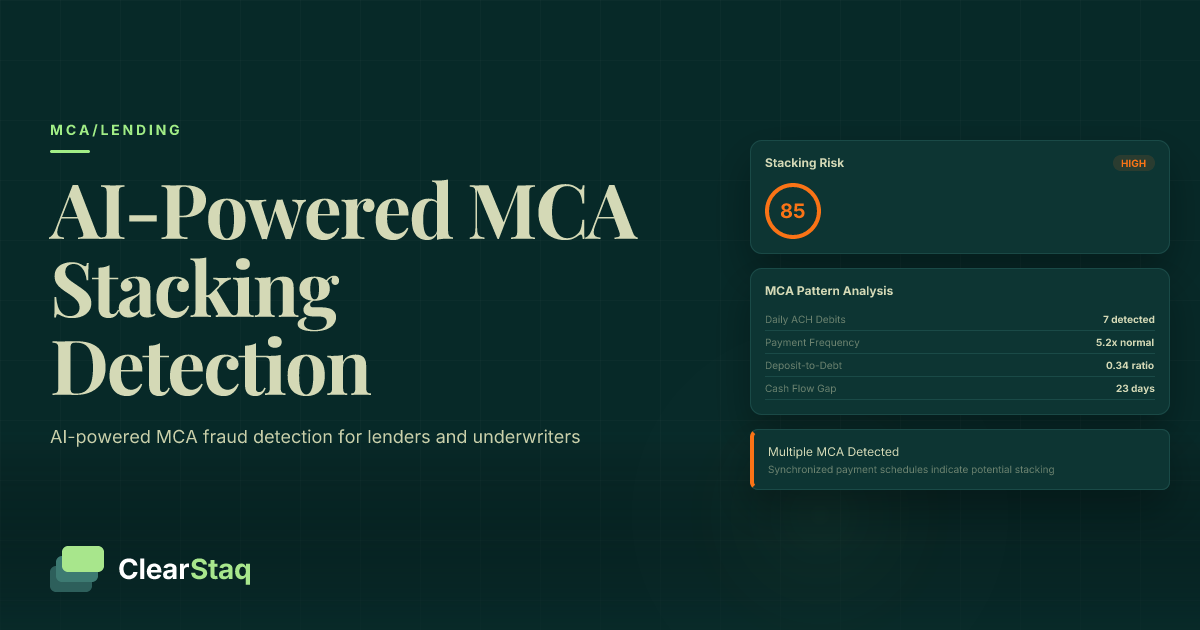

MCA stacking detection requires analyzing bank statements for specific patterns: multiple daily ACH debits, synchronized payment schedules, declining deposit-to-debt ratios, and cash flow inconsistencies. Automated systems can identify 27 fraud signals simultaneously, including transaction timing patterns and payment frequency anomalies that indicate layered merchant cash advances.

What you'll learn

- MCA stacking increases default risk by 40-75% depending on the number of stacked advances

- Seven specific bank statement patterns reliably identify MCA stacking scenarios

- Automated detection achieves 95% accuracy compared to 75% for manual underwriting review

- Multiple daily ACH debits with similar amounts are the clearest indicator of stacking

- AI systems process complex stacking patterns in 30 seconds versus 45-60 minutes manually

MCA stacking detection requires analyzing bank statements for specific patterns: multiple daily ACH debits, synchronized payment schedules, declining deposit-to-debt ratios, and cash flow inconsistencies. Automated systems can identify 27 fraud signals simultaneously, including transaction timing patterns and payment frequency anomalies that indicate layered merchant cash advances.

What is MCA Stacking and Why It Matters

MCA stacking occurs when a merchant obtains multiple overlapping merchant cash advances from different lenders, often without disclosing existing obligations. This practice creates a dangerous web of financial commitments that can quickly spiral out of control for both merchants and lenders.

The prevalence of MCA stacking has grown significantly in recent years. Industry data shows that 26% of merchants with one MCA will take a second advance within six months, and 15% will have three or more active advances simultaneously. For lenders, this represents a hidden risk that's difficult to detect through traditional underwriting methods.

How MCA Stacking Works

Merchants engage in two primary types of stacking: sequential and simultaneous. Sequential stacking happens when a merchant takes a new MCA shortly after receiving a previous one, often using the fresh capital to service existing debt. Simultaneous stacking is more aggressive — merchants apply to multiple lenders at once, hoping to secure funding before any single lender discovers the others.

The factor rate compounding effect makes stacking particularly dangerous. A merchant with three MCAs at 1.3 factor rates isn't paying 30% more — they're often paying 90-120% more than their original revenue once daily payments compound. This mathematical reality catches many merchants off guard.

The Merchant's Motivation

Understanding why merchants stack MCAs helps identify at-risk applicants. Cash flow gaps drive most stacking behavior — a merchant might need $50,000 but only qualify for $20,000 from a single lender. Rather than addressing underlying business issues, they seek multiple smaller advances.

Traditional loan qualification challenges push many merchants toward stacking. Banks typically require 680+ credit scores and two years of tax returns. MCAs offer faster approval with lower barriers, making it tempting to layer multiple advances when traditional financing isn't available. When discussing broader MCA cash flow analysis, these motivations become critical risk factors.

The Hidden Cost of MCA Stacking for Lenders

MCA stacking dramatically increases portfolio risk beyond what most lenders model in their underwriting. The financial impact compounds with each additional layer of debt a merchant carries, creating cascading default risks that affect recovery rates and profitability.

Beyond direct losses, stacked merchants require more servicing resources, generate more disputes, and create regulatory scrutiny. State regulators increasingly focus on predatory lending practices, and portfolios heavy with stacked merchants draw unwanted attention.

Financial Impact by Stacking Level

The data on stacking risk is stark. Merchants with two active MCAs show a 40% higher default rate compared to single-advance merchants. This jumps to 75% higher default risk for merchants carrying three or more advances. Recovery rates also plummet — while single-MCA defaults typically recover 45-60%, stacked merchant defaults often recover less than 20%.

Portfolio concentration amplifies these risks. A lender with 20% of their portfolio in unknowingly stacked merchants faces potential losses 3-4x higher than their risk models predict. This hidden exposure has bankrupted several mid-sized MCA companies in recent downturns.

Legal and Regulatory Risks

Disclosure requirements vary by state, but most jurisdictions require lenders to assess a borrower's ability to repay. Funding a merchant who's already overleveraged with multiple MCAs raises serious compliance questions. California, New York, and Virginia have enacted specific MCA regulations that increase liability for lenders who don't perform adequate due diligence.

Fair lending practices also come into play. Regulators view systematic funding of overleveraged merchants as potentially predatory, especially when automated systems could have detected the stacking. The legal costs of defending against such claims often exceed the profits from the entire merchant relationship.

7 Bank Statement Patterns That Reveal MCA Stacking

Bank statements tell the story of MCA stacking through specific, identifiable patterns. Understanding these patterns transforms underwriting from guesswork into data-driven risk assessment. Here's how multiple MCA payments create recognizable signatures in transaction data:

1. Multiple Daily ACH Debits with Similar Amounts

The most obvious pattern appears as multiple ACH debits hitting the account each business day. Look for 2-5 separate withdrawals ranging from $200 to $2,000, often with similar but not identical amounts. These payments typically post between 6 AM and 10 AM EST.

Pattern recognition requires examining payment consistency. Legitimate business expenses rarely recur daily with such precision. When you see "$847.32" from one processor and "$623.41" from another every single business day, you're looking at MCA payments.

2. Synchronized Payment Schedules

MCAs follow predictable schedules — either daily (Monday-Friday) or weekly. Stacked merchants show multiple payment streams following these patterns simultaneously. Watch for payments that skip the same holidays or adjust on the same dates.

Weekly patterns reveal stacking when multiple Wednesday or Friday debits appear from different sources. The synchronization often breaks down during holiday weeks, making Thanksgiving week and Christmas week particularly revealing for pattern analysis.

3. Declining Deposit-to-Payment Ratios

Mathematical indicators provide objective stacking evidence. Calculate the ratio of daily deposits to daily MCA payments. Healthy merchants maintain ratios above 3:1. Stacked merchants often drop below 2:1, with severely stacked situations showing 1.5:1 or worse.

Trend analysis over 90 days typically shows steady ratio decline as merchants add new MCAs. A merchant starting at 4:1 who drops to 2:1 over three months has likely added at least one additional advance during that period.

4. Cash Flow Timing Inconsistencies

Revenue and payment timing mismatches indicate stacking stress. Merchants receiving most revenue on weekends but facing daily weekday MCA payments often stack to bridge cash flow gaps. This pattern intensifies during seasonal slowdowns.

Understanding these bank statement fraud patterns helps identify both intentional deception and merchants sliding toward default through desperation stacking.

Manual vs. Automated MCA Stacking Detection

Manual review of bank statements for MCA stacking patterns requires significant expertise and time. An experienced underwriter needs 45-60 minutes to thoroughly analyze three months of statements, and even then, accuracy rates hover around 75% for complex stacking scenarios.

The limitations of human review become clear when you consider the volume of transactions. A typical small business processes 1,000-3,000 transactions monthly. Identifying patterns across 9,000 transactions while maintaining consistency requires superhuman attention to detail.

The Manual Review Process

Manual reviewers typically start by identifying potential MCA payments through amount patterns and timing. They'll create spreadsheets tracking daily debits, calculate running ratios, and flag suspicious patterns. This process requires deep expertise — junior underwriters miss 40% of stacking indicators that veterans catch.

Skill dependencies create bottlenecks. Most MCA companies have 2-3 senior underwriters capable of reliable stacking detection. When these key people are unavailable, approval quality drops dramatically. The time investment also limits throughput — even the best underwriters can only process 8-12 complete reviews daily.

Why Automation Wins

Automated systems process the same three-month statement set in under 30 seconds with 95%+ accuracy. Pattern matching algorithms identify payment streams that humans miss, especially when MCAs use different payment processors or varying amounts.

Real-time analysis enables dynamic risk assessment. While manual reviewers work with static PDFs, automated bank statement parsing systems can flag new patterns as they emerge, enabling proactive risk management rather than reactive damage control.

Scalability benefits compound quickly. An automated system processing 1,000 applications monthly saves approximately 750 underwriting hours — equivalent to 4-5 full-time employees. This efficiency gain allows human underwriters to focus on complex cases requiring judgment rather than pattern recognition.

How AI Identifies MCA Stacking Patterns

Artificial intelligence transforms MCA stacking detection from pattern matching to predictive risk analysis. Machine learning models trained on millions of bank transactions identify subtle relationships that indicate stacking risk before it becomes obvious through payment patterns.

Modern AI systems analyze transaction data across multiple dimensions simultaneously. While a human underwriter might spot daily ACH debits, AI correlates those debits with deposit timing, merchant category codes, seasonal patterns, and cash flow velocity to build a comprehensive risk profile.

Transaction Pattern Analysis

ACH debit identification goes beyond simple amount matching. AI algorithms analyze transaction descriptors, timing patterns, and amount variations to identify MCA payments with 98% accuracy. The system learns from each new pattern, continuously improving its detection capabilities.

Payment frequency algorithms detect both obvious daily patterns and complex weekly or bi-weekly arrangements. The AI identifies split-funding arrangements where MCAs take percentages of credit card batches rather than fixed amounts, a pattern human reviewers often miss.

Amount clustering reveals hidden relationships between seemingly unrelated transactions. When three different ACH debits show mathematical relationships — like one being exactly 1.5x another — it suggests coordinated MCA payments even with different processors.

Risk Signal Aggregation

Multiple signal weighting creates nuanced risk scores. Rather than binary "stacked/not stacked" decisions, AI systems evaluate probability across a spectrum. A merchant showing five weak signals might score the same as one showing two strong signals.

Confidence scoring helps underwriters focus their attention. High-confidence stacking detection (90%+) can trigger automatic decline or require senior review. Medium-confidence scores (60-89%) might proceed with additional stipulations. This graduated approach based on 27 fraud detection signals reduces both false positives and missed risks.

Best Practices for MCA Underwriters

Effective MCA stacking detection requires systematic approaches, whether using manual or automated methods. These practices help identify stacking while maintaining efficient operations and positive merchant relationships.

Documentation standards form the foundation of effective detection. Requiring six months of bank statements instead of three increases stacking detection rates by 40%. Merchants rarely maintain deception across extended periods, and longer histories reveal pattern evolution.

Initial Screening Protocol

Bank statement requirements should be non-negotiable. Accept only PDF statements directly from banks or authorized aggregators. Screenshots, photos, or edited PDFs invite fraud. Implement immediate verification through penny deposits or banking APIs when possible.

Look-back periods must account for sequential stacking. Three months shows current obligations, but six months reveals stacking progression. For renewal applications, compare current patterns to original underwriting — ratio degradation often indicates interim stacking.

Documentation standards should specify complete statements including all pages. Merchants sometimes remove pages showing MCA payments while keeping deposit pages. Automated page-count verification against bank standards catches this manipulation.

Ongoing Monitoring Strategies

Periodic statement reviews catch post-funding stacking. Monthly spot checks on 10-20% of your portfolio, focusing on merchants 3-6 months into their advance, identify problems before they cascade. Early detection enables proactive merchant counseling rather than costly defaults.

Performance triggers automate monitoring efficiency. Set alerts for payment delays, NSFs, or requests for payment modifications. These events correlate strongly with new stacking as merchants scramble for additional capital.

Early warning systems based on the MCA underwriting checklist help standardize detection across your team. When multiple team members follow identical protocols, pattern recognition improves and institutional knowledge accumulates faster.

See ClearStaq's MCA Stacking Detection in Action

Upload a bank statement and watch our AI identify complex stacking patterns in seconds. Book a demo to see how automated detection protects your portfolio from hidden risks.

How ClearStaq Detects MCA Stacking Automatically

ClearStaq's fraud detection engine analyzes bank statements using 27 distinct signals specifically calibrated for MCA stacking patterns. The system processes transactions in real-time through API integration, delivering risk assessments in seconds rather than hours.

Our machine learning models train on millions of verified MCA transactions, recognizing patterns across different payment processors, banking platforms, and merchant industries. This comprehensive training enables detection accuracy exceeding 95%, with false positive rates below 3%.

Advanced Pattern Recognition

ClearStaq's pattern recognition goes beyond simple ACH matching. The system identifies split-funding arrangements, percentage-based withdrawals, and even manually initiated daily transfers that mimic automated MCA payments. Transaction categorization algorithms separate legitimate recurring expenses from MCA obligations with remarkable precision.

Timing analysis reveals hidden relationships between payments. Our AI detects when merchants deliberately stagger MCA payments throughout the day to obscure stacking, or when they use multiple bank accounts to segregate different advances. These sophisticated evasion techniques fool manual reviewers but create detectable patterns in aggregated data.

API Integration Benefits

Real-time processing through the ClearStaq API transforms underwriting workflows. Submit bank statements programmatically and receive comprehensive risk analysis including stacking probability scores, identified MCA payments, and cash flow projections within seconds.

Workflow automation eliminates manual data entry and reduces human error. Our MCA lending solutions integrate with popular loan origination systems, CRMs, and underwriting platforms. Automatic risk scoring enables instant decisioning for clear approvals or declines, while flagging borderline cases for human review.

Scalable analysis handles volume spikes without degrading accuracy or speed. Whether you're processing 10 or 10,000 applications monthly, each receives the same thorough 27-point analysis. This consistency improves portfolio quality while reducing operational costs.

Frequently Asked Questions

What is MCA stacking and why is it dangerous?

MCA stacking occurs when merchants obtain multiple overlapping merchant cash advances. It's dangerous because each additional MCA exponentially increases default risk, with merchants holding 3+ MCAs showing 75% higher failure rates than single-MCA borrowers.

How can you detect MCA stacking from bank statements?

Look for multiple daily ACH debits, synchronized payment schedules, declining deposit-to-payment ratios, and cash flow inconsistencies. Automated systems analyze 27+ signals simultaneously to identify these patterns with higher accuracy than manual review.

What are the most reliable signs of merchant cash advance layering?

The most reliable indicators include multiple daily ACH debits with similar amounts, payment schedules that align across different dates, and deposit-to-debt ratios that decline over time as payment obligations compound.

How accurate is automated MCA stacking detection?

Modern AI-powered systems achieve over 95% accuracy in detecting MCA stacking by analyzing transaction patterns, payment timing, and cash flow relationships that human reviewers often miss or miscategorize.

Stop MCA Stacking from Threatening Your Portfolio

Don't let complex stacking patterns slip through your underwriting process. ClearStaq's automated detection catches what manual review misses — in seconds, not hours. Book your demo today and see the difference AI-powered analysis makes.

Frequently Asked Questions

What is MCA stacking and why is it dangerous?

MCA stacking occurs when merchants obtain multiple overlapping merchant cash advances. It's dangerous because each additional MCA exponentially increases default risk, with merchants holding 3+ MCAs showing 75% higher failure rates than single-MCA borrowers.

How can you detect MCA stacking from bank statements?

Look for multiple daily ACH debits, synchronized payment schedules, declining deposit-to-payment ratios, and cash flow inconsistencies. Automated systems analyze 27+ signals simultaneously to identify these patterns with higher accuracy than manual review.

What are the most reliable signs of merchant cash advance layering?

The most reliable indicators include multiple daily ACH debits with similar amounts, payment schedules that align across different dates, and deposit-to-debt ratios that decline over time as payment obligations compound.

How accurate is automated MCA stacking detection?

Modern AI-powered systems achieve over 95% accuracy in detecting MCA stacking by analyzing transaction patterns, payment timing, and cash flow relationships that human reviewers often miss or miscategorize.

ClearStaq Team

Product Team

The ClearStaq team builds AI-powered tools for bank statement parsing, fraud detection, and income verification.