Fake bank statements can be detected by examining seven key indicators: inconsistent fonts, misaligned columns, incorrect running balances, suspicious PDF metadata, round-number deposits, missing transaction details, and irregular statement formatting. Automated tools like ClearStaq analyze 27 fraud signals simultaneously for instant verification with over 99% accuracy.

What you'll learn

- Seven visual and technical indicators reliably identify fake bank statements

- PDF metadata analysis reveals manipulation that human review misses

- Automated fraud detection achieves 99.5% accuracy versus 60-70% for manual review

- Running balance verification catches mathematical errors in fraudulent statements

- AI-powered tools analyze documents in seconds, not hours

Fake bank statements can be detected by examining seven key indicators: inconsistent fonts, misaligned columns, incorrect running balances, suspicious PDF metadata, round-number deposits, missing transaction details, and irregular statement formatting. Automated tools like ClearStaq analyze 27 fraud signals simultaneously for instant verification with over 99% accuracy.

What Are Fake Bank Statements and Why Do People Use Them?

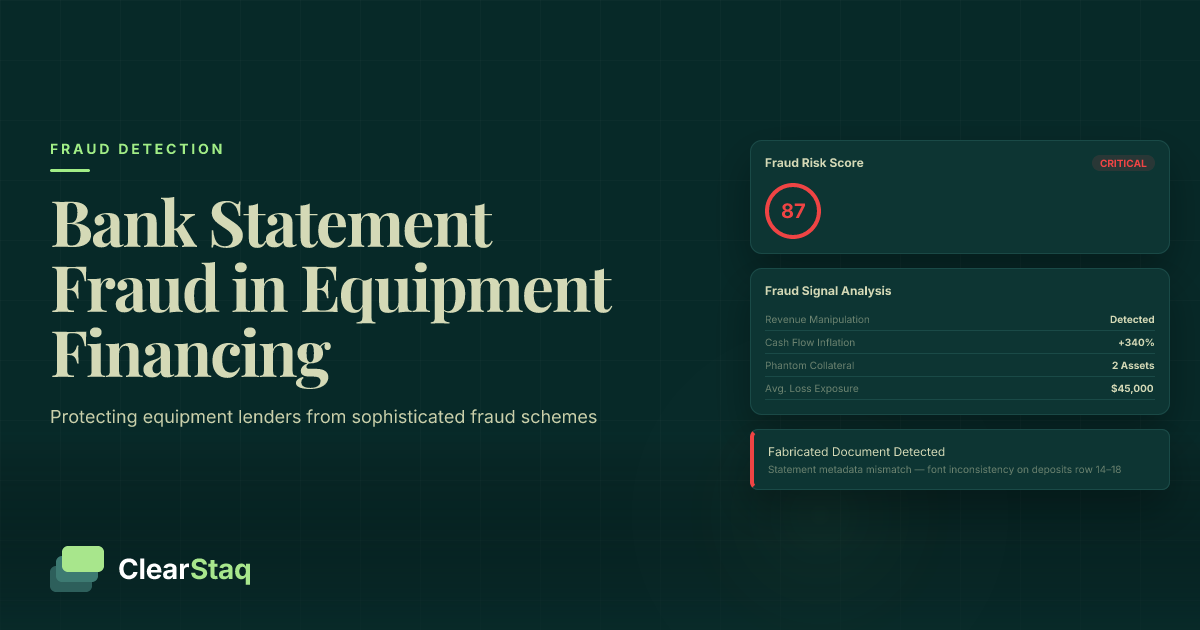

A fake bank statement is an altered or completely fabricated financial document created to misrepresent someone's financial standing. These fraudulent documents range from sophisticated digital forgeries to crude manual alterations, all designed to deceive lenders, landlords, or employers.

The scale of this problem is staggering. According to latest bank statement fraud statistics, up to 15% of loan applications contain some form of document manipulation. For MCA lenders specifically, fraudulent applications cost the industry over $1.5 billion annually in bad debt and defaults.

People create fake bank statements for various reasons:

- Loan applications — Inflating income or hiding negative balances to qualify for financing

- Rental applications — Meeting income requirements for apartment leases

- Business funding — Securing merchant cash advances or working capital

- Employment verification — Proving financial stability for job applications

Fraudsters typically use two approaches: completely fabricated statements created from templates, or altered legitimate statements where specific transactions, dates, or amounts are modified. The financial impact on lenders is severe — fraudulent loans default at 3.5x the rate of legitimate ones, with average losses exceeding $45,000 per incident.

The Growing Problem of Document Fraud

Document fraud has evolved dramatically with digital technology. What once required physical cut-and-paste techniques now happens in seconds with PDF editing software. The proliferation of online fraud services has made fake documents more accessible and harder to detect.

Industry fraud rates have increased 42% since 2020, driven by economic pressures and the shift to digital lending. MCA lenders face particular challenges — their speed-focused underwriting processes and higher risk tolerance make them prime targets for sophisticated fraud operations.

The evolution of fraud techniques keeps pace with detection methods. As lenders implement new verification processes, fraudsters develop workarounds. Today's fake statements can include realistic transaction patterns, proper formatting, and even fake bank websites for "verification."

Why Bank Statements Are Prime Targets

Bank statements are especially vulnerable to fraud for several reasons. First, they're easy to manipulate digitally — PDF editing tools allow fraudsters to change any element without leaving obvious traces. Unlike physical documents with security features, digital statements rely primarily on formatting consistency for authenticity.

Second, bank statements are critical for underwriting decisions. They provide the primary evidence of cash flow, financial stability, and repayment capacity. This makes them high-value targets — successfully faking a statement can mean the difference between approval and rejection.

Finally, the availability of template-based fraud tools has lowered the barrier to entry. Online services offer "bank statement generators" that create realistic-looking documents for any major bank. Some even provide matching websites that appear to verify the fraudulent statements.

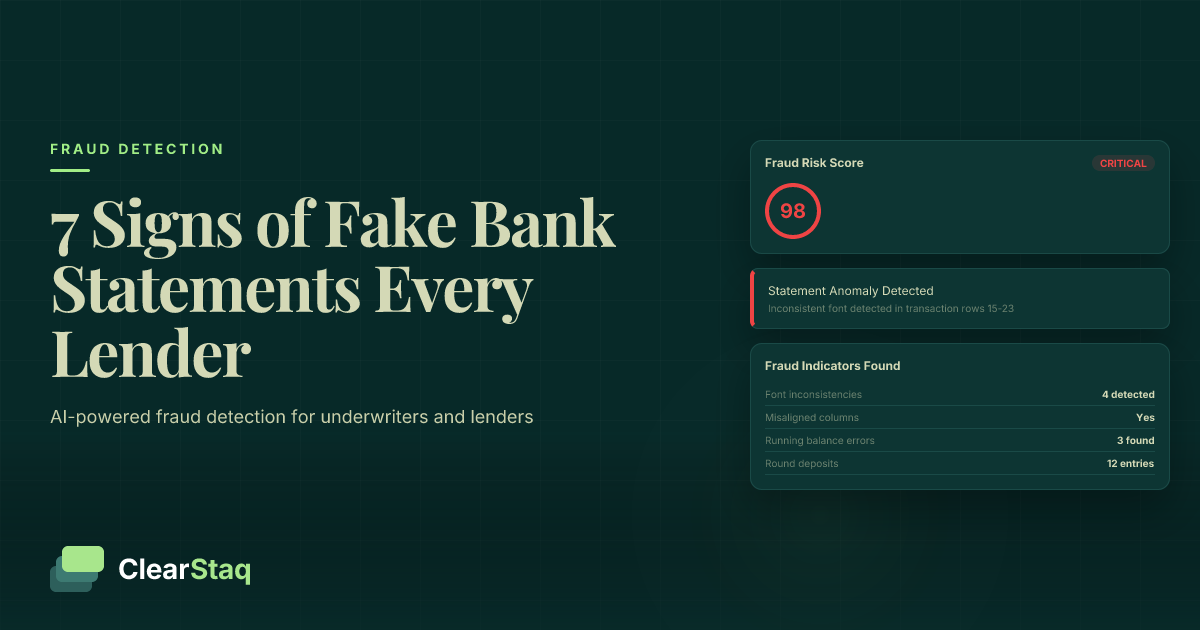

7 Signs of a Fake Bank Statement Every Underwriter Should Know

Detecting fake bank statements requires knowing exactly what to look for. These seven indicators, when examined systematically, reveal document manipulation that fraudsters hope will slip past busy underwriters. Master these signs and you'll catch fraud that others miss.

1. Inconsistent Fonts and Typography

Font inconsistencies are the most common giveaway in fake bank statements. Legitimate bank statements use consistent typography throughout — same font family, size, and weight for similar elements. Fraudsters often overlook these details when editing.

Look for these specific typography red flags:

- Font switching mid-statement — Different fonts for account numbers vs. transaction details

- Incorrect bank font usage — Using Arial when the bank uses Helvetica

- Size and weight inconsistencies — Transaction amounts in different sizes

- Character spacing irregularities — Compressed or expanded text where edits were made

Professional fraudsters may match fonts closely, but pixel-level analysis reveals subtle differences in kerning, baseline alignment, and anti-aliasing that human eyes miss.

2. Mathematical Errors in Running Balances

Mathematical errors are smoking guns in fake statements. Every transaction must correctly calculate into the running balance — a single error exposes the entire document as fraudulent.

Common mathematical red flags include:

- Balance calculations don't add up — Deposits and withdrawals don't match balance changes

- Missing or incorrect running totals — Skipped balance updates after transactions

- Rounding errors — Improper decimal calculations

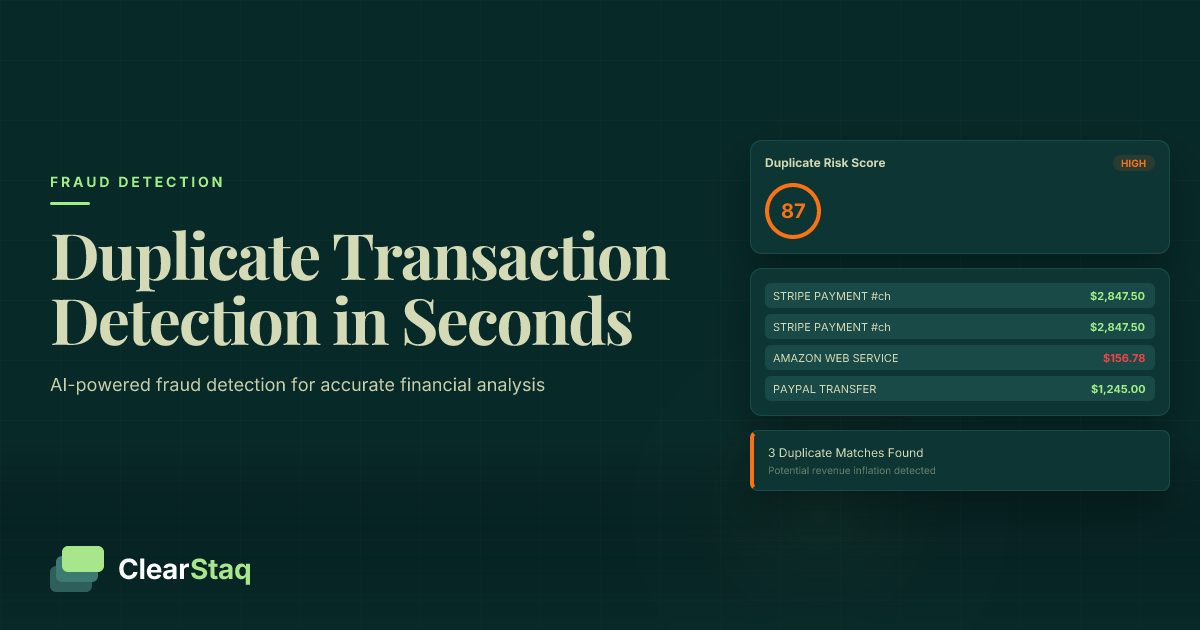

- Duplicate balances — Same balance appearing after different transactions

Automated verification catches these errors instantly by recalculating every transaction. Manual reviewers should spot-check at least 10 transactions, focusing on large deposits and the statement's final balance.

3. Suspicious PDF Metadata and Digital Forensics

PDF metadata tells the hidden story of a document's creation and modification. This invisible information reveals when, how, and by whom a statement was created — critical evidence that fraudsters often forget to scrub.

Key metadata indicators of fraud:

- Creator software reveals manipulation — "Adobe Photoshop" instead of bank systems

- Creation vs. modification dates — Statement "created" after its supposed date

- Multiple modification timestamps — Evidence of post-creation editing

- Missing digital signatures — Legitimate bank PDFs include cryptographic signatures

Banks generate statements using specific software that leaves unique metadata fingerprints. Any deviation from these patterns indicates manipulation.

4. Formatting and Layout Irregularities

Banks maintain strict formatting standards across all statements. Even minor deviations from these standards signal potential fraud. Fraudsters struggle to replicate the precise alignment and spacing of legitimate statements.

Watch for these formatting issues:

- Column misalignment — Transaction details don't line up properly

- Inconsistent date formats — Switching between MM/DD/YY and MM/DD/YYYY

- Logo quality and placement — Blurry or incorrectly positioned bank logos

- Page structure variations — Headers and footers in wrong positions

Legitimate statements use precise grid systems. Measure the pixel distances between elements — fraudulent edits almost always disturb this mathematical precision.

5. Unrealistic Transaction Patterns

Fraudulent transaction patterns betray themselves through their unnaturalness. Real spending follows predictable patterns — coffee shops, gas stations, groceries. Fake statements often lack this organic flow.

Transaction pattern red flags:

- Too many round-number amounts — Real transactions rarely end in .00

- Missing typical bank fees — No monthly maintenance or ATM fees

- Suspicious timing of deposits — All deposits on the same day of the week

- Lack of normal spending patterns — No small daily purchases or recurring bills

Sophisticated fraudsters study real statements to mimic natural patterns, but they often overcorrect, creating patterns that are too perfect or too random.

6. Missing or Altered Bank Security Features

Banks embed multiple security features in their statements. These elements are difficult to replicate and often removed entirely by fraudsters to simplify editing.

Security features to verify:

- Watermark absence — Background patterns or bank logos

- Security elements removed — Microtext or guilloche patterns

- Bank routing information errors — Incorrect or mismatched routing numbers

- Missing transaction codes — Reference numbers banks use for tracking

Each bank has unique security implementations. Building a reference library of legitimate statement features helps quickly identify missing elements.

7. Pixel-Level Manipulation Evidence

Digital forensics at the pixel level reveals manipulation invisible to casual inspection. Every edit leaves traces in how pixels interact with surrounding areas.

Pixel-level fraud indicators:

- Image compression artifacts — JPEG artifacts around edited text

- Color inconsistencies — Slightly different black values in edited areas

- Copy-paste detection — Identical pixel patterns from duplicated elements

- Digital alteration traces — Edge artifacts from selection tools

Advanced detection systems analyze these pixel-level patterns across the entire document, comparing them to known legitimate statement characteristics.

As you can see, ClearStaq's fraud detection engine analyzes all seven indicators simultaneously, plus 20 additional signals, providing instant risk scoring that would take human reviewers hours to complete.

How Fraudsters Create Fake Bank Statements

Understanding fraud techniques helps underwriters stay ahead of evolving threats. Fraudsters have moved far beyond simple PDF editing, employing sophisticated tools and services that produce increasingly convincing fakes.

The fraud ecosystem has professionalized. What started as individuals editing statements in Photoshop has evolved into organized operations offering "verification-proof" documents. These services study bank formats meticulously, updating their templates whenever banks change their layouts.

Modern fraudsters use a combination of automated tools and manual refinement. They start with authentic statements as templates, maintaining genuine formatting while replacing key data. This hybrid approach produces documents that pass casual inspection but fail under systematic analysis.

PDF Editing and Manipulation Tools

The most common fraud method involves direct PDF editing. Fraudsters use both professional software and specialized tools designed specifically for document manipulation.

Popular software in the fraudster's toolkit includes Adobe Acrobat for basic edits, specialized PDF editors that preserve formatting, and custom scripts that automate common modifications. These tools leave specific signatures — Adobe products embed identifiable metadata, while black-market tools often strip all metadata entirely.

Advanced fraudsters use techniques like layer manipulation, where they edit the text layer while preserving the background, or font substitution, where they replace entire text blocks with matching fonts. They may also employ anti-forensic techniques, attempting to clean metadata and standardize compression to hide their tracks.

Statement Generation Services

The dark web hosts numerous "bank statement generator" services. These operations offer templates for major banks, complete with accurate formatting, logos, and transaction patterns. Prices range from $50 for basic statements to $500+ for "premium" packages with verification support.

These services have become alarmingly sophisticated. They maintain databases of real transaction patterns, use authentic bank fonts, and even provide fake online banking portals for "verification." Some offer guarantees that their documents will pass specific lender checks.

The templates are constantly updated. When banks change their statement formats, these services update within days. They monitor lender verification processes, adapting their techniques to bypass new security measures. This cat-and-mouse game drives the need for continuously evolving detection methods.

Manual vs. Automated Bank Statement Verification

The gap between manual and automated verification has never been wider. While human reviewers struggle with increasing fraud sophistication and volume, automated systems detect subtle fraud indicators in seconds that humans would never notice.

Manual review faces fundamental limitations. Human reviewers can process perhaps 20-30 statements daily while maintaining accuracy. Fatigue sets in quickly when examining repetitive documents, leading to missed fraud indicators. Studies show manual detection rates plateau around 65% accuracy, even with experienced underwriters.

Time constraints compound these challenges. In high-volume lending environments, reviewers have minutes per application. This pressure leads to shortcut-taking and overlooked red flags. As application volumes grow, maintaining consistent manual review quality becomes impossible.

The Manual Review Process

Traditional manual review follows a checklist approach. Underwriters verify basic elements like bank logos, account numbers, and running balances. They look for obvious signs of manipulation but lack tools to detect sophisticated fraud.

A typical MCA underwriting checklist includes verifying statement dates match application periods, checking for consistent formatting, calculating sample transactions, and confirming bank contact information. This process takes 15-30 minutes per statement under ideal conditions.

Manual review accuracy varies dramatically based on reviewer experience, training quality, and workload. Even experienced underwriters miss 30-40% of fraudulent documents, particularly those using advanced manipulation techniques. Consistency between reviewers is another challenge — different underwriters often reach different conclusions on the same document.

Scalability represents the ultimate limitation. Doubling application volume requires doubling staff, with linear cost increases. Training new reviewers takes weeks, and quality suffers during growth periods when experienced staff are stretched thin.

Benefits of Automated Detection

Automated detection transforms the verification process through speed, accuracy, and consistency. Systems analyze hundreds of fraud signals simultaneously, completing in seconds what would take humans hours.

Speed advantages are dramatic — automated systems process statements in 2-3 seconds versus 15-30 minutes manually. This acceleration enables real-time decisioning, improving customer experience while reducing operational costs. A single API can handle thousands of verifications daily without degradation in accuracy.

Consistency eliminates human variability. Every statement receives the same thorough analysis regardless of volume, time of day, or reviewer fatigue. Automated systems don't take shortcuts under pressure or miss details due to distraction.

Advanced detection capabilities surpass human abilities entirely. Pixel-level analysis, metadata forensics, and pattern recognition identify fraud invisible to human reviewers. Machine learning models trained on millions of statements recognize subtle patterns that indicate manipulation.

Real-time alerts demonstrate how automated systems catch fraud instantly. Each alert represents a detected anomaly that would likely escape manual review, from metadata inconsistencies to mathematical errors in running balances.

How AI-Powered Fraud Detection Works

Modern fraud detection combines multiple AI technologies to create a comprehensive defense against document manipulation. These systems analyze documents across dozens of dimensions simultaneously, far exceeding human capabilities.

The foundation is multi-signal analysis — examining 27 fraud detection signals that cover every aspect of document authenticity. From PDF metadata to pixel-level patterns, each signal contributes to an overall fraud risk score. This holistic approach catches fraud that single-method detection would miss.

Machine learning models train on millions of legitimate and fraudulent statements, learning subtle patterns that distinguish real from fake. These models continuously improve as they process more documents, adapting to new fraud techniques automatically. The result is a fraud detection platform that gets smarter over time.

Integration capabilities make these powerful tools accessible through simple APIs. Lenders can add fraud detection to existing workflows without disrupting operations. Real-time processing enables instant decisions while maintaining the highest accuracy standards.

The 27 Fraud Detection Signals

ClearStaq's fraud detection analyzes 27 distinct signals across four categories. Each signal represents a potential fraud indicator, weighted by its reliability and combined into a comprehensive risk score.

Metadata analysis examines PDF properties, creation timestamps, modification history, and software signatures. These invisible attributes often contain smoking-gun evidence of manipulation. Even sophisticated fraudsters struggle to perfectly clean metadata.

Visual pattern recognition uses computer vision to identify formatting inconsistencies, font variations, alignment issues, and image manipulation. AI models trained on millions of statements recognize subtle visual patterns that indicate fraud.

Mathematical validation recalculates every transaction, verifies running balances, checks date sequences, and analyzes transaction patterns. Any mathematical inconsistency immediately flags the document as suspicious.

Format consistency checks compare documents against known templates for each bank, identifying deviations in layout, styling, security features, and structure. Banks rarely change formats, making any variation suspicious.

Real-Time Fraud Scoring

Every analyzed document receives a fraud risk score from 0-100, with confidence levels for each detection signal. This granular scoring enables nuanced decision-making based on risk tolerance.

Scores above 80 indicate high fraud probability, requiring manual review or automatic rejection. Scores between 20-80 suggest specific concerns worth investigating. Scores below 20 indicate authentic documents with high confidence. These thresholds are customizable based on lender risk policies.

Beyond the overall score, the system provides actionable insights explaining why a document appears fraudulent. Underwriters see exactly which signals triggered alerts, from "PDF created after statement date" to "mathematical errors in transactions 14-16." This transparency builds trust and enables informed decisions.

API integration makes fraud scoring seamless. Send a statement via API and receive comprehensive results in seconds. The API supports batch processing for high-volume operations and webhooks for asynchronous workflows. Pre-built integrations exist for popular lending platforms.

The automated pipeline demonstrates how bank statement parsing and fraud detection work together. Documents flow through parsing to extract transaction data, then through fraud analysis to verify authenticity, providing both data and trust in one seamless process.

Best Practices for Bank Statement Verification

Effective fraud prevention combines automated detection with smart processes. Even the best technology requires proper implementation to maximize effectiveness while maintaining positive customer experiences.

The key is finding the right balance between security and friction. Overly aggressive fraud prevention frustrates legitimate customers, while lax processes invite fraud. Leading lenders use tiered approaches, applying different verification levels based on risk indicators.

Staff training remains critical even with automation. Underwriters need to understand both fraud techniques and detection technology to make informed decisions. Regular updates on emerging fraud trends keep teams ahead of evolving threats.

Documentation and compliance considerations shape verification workflows. Maintaining audit trails of verification decisions protects against liability while satisfying regulatory requirements. Clear policies ensure consistent application of fraud prevention measures.

Implementing a Verification Workflow

Successful verification workflows follow a structured process with clear decision points. Start with automated screening of all documents, flagging high-risk applications for enhanced review. This preserves resources for cases requiring human judgment.

Design decision trees based on fraud scores and specific risk signals. Applications scoring below 20 might receive automatic approval, while those above 80 trigger automatic rejection or enhanced due diligence. Middle-range scores route to manual review with specific investigation points highlighted.

Documentation requirements should be proportional to risk. Low-risk applications might need only the automated fraud report. High-risk cases require detailed notes on investigation steps and decision rationale. This graduated approach balances thoroughness with efficiency.

Quality assurance measures ensure consistent workflow application. Regular audits of approved and rejected applications identify process improvements. Tracking fraud detection rates and false positive rates guides threshold adjustments over time.

Staff Training and Education

Comprehensive staff training transforms fraud detection effectiveness. Begin with fraud awareness programs covering common schemes, evolving techniques, and real-world examples. Use actual fraudulent documents (anonymized) to build pattern recognition skills.

Regular training updates are essential as fraud evolves. Monthly sessions covering new fraud trends, technology updates, and case studies keep skills sharp. Create internal knowledge bases documenting detected fraud patterns specific to your customer base.

Provide underwriters with proper tools and resources. This includes access to fraud detection systems, reference libraries of legitimate statements, and clear escalation procedures for suspicious cases. Empower staff to investigate concerns without fear of slowing processes.

Performance monitoring helps identify training needs. Track individual reviewer accuracy rates, comparing their decisions to automated detection results. Use discrepancies as teaching opportunities, building expertise over time. For comprehensive MCA fraud prevention, combine technological tools with human expertise.

Legal and Compliance Considerations

Document verification carries significant legal and compliance obligations. Understanding these requirements protects lenders from regulatory penalties while establishing defensible fraud prevention practices.

Regulatory frameworks increasingly emphasize the importance of identity verification and document authenticity. Financial institutions face strict requirements for Know Your Customer (KYC) procedures, which extend to document verification. Non-compliance risks include substantial fines, legal liability, and reputational damage.

The legal landscape continues evolving as digital fraud becomes more sophisticated. Courts increasingly expect financial institutions to employ reasonable fraud detection measures. "Reasonable" now includes automated verification for any significant lending operation.

Risk management frameworks must incorporate document verification as a core component. This includes policies, procedures, technology selection, and ongoing monitoring. Proper frameworks protect against both fraud losses and regulatory sanctions.

Regulatory Requirements

FFIEC guidelines establish baseline requirements for authentication and fraud detection in financial services. These guidelines mandate "layered security" approaches combining multiple verification methods. Single-factor verification no longer meets regulatory expectations.

Due diligence standards require verifying customer-provided information through reliable sources. Bank statement verification forms a critical component of income verification and financial capacity assessment. Regulators expect institutions to detect and prevent fraudulent documentation.

Documentation requirements include maintaining records of verification procedures, detection results, and decision rationale. Auditors review these records to assess compliance with fraud prevention obligations. Inadequate documentation can result in compliance failures even when fraud is successfully prevented.

Audit expectations continue rising as fraud becomes more prevalent. Examiners now specifically review document verification procedures, testing their effectiveness against known fraud patterns. Institutions must demonstrate both preventive measures and detection capabilities.

Legal Consequences of Fraud

Borrowers submitting fraudulent documents face serious criminal penalties. Bank fraud charges carry sentences up to 30 years in federal prison and fines up to $1 million. State charges for forgery and fraud add additional penalties. Prosecution rates are increasing as law enforcement prioritizes financial fraud.

Lender liability considerations extend beyond direct fraud losses. Accepting fraudulent documents can trigger legal exposure for negligent lending practices. Investors and guarantors may seek recourse for losses resulting from inadequate verification procedures.

Insurance and loss mitigation strategies require documented fraud prevention efforts. Many policies exclude losses from fraud that "should have been detected" through reasonable measures. Automated verification provides evidence of reasonable fraud prevention efforts.

Reporting obligations vary by jurisdiction but generally require notifying law enforcement of detected fraud attempts. Suspicious Activity Reports (SARs) must be filed for fraud exceeding threshold amounts. Proper detection and documentation facilitate required reporting while protecting the institution.

Frequently Asked Questions

How can you tell if a bank statement is fake?

Look for inconsistent fonts, incorrect running balances, suspicious PDF metadata, round-number deposits, formatting irregularities, missing security features, and pixel-level manipulation evidence. Automated tools can detect these signs instantly by analyzing 27+ fraud signals simultaneously.

Can AI detect fake bank statements automatically?

Yes. AI-powered fraud detection analyzes PDF metadata, font consistency, mathematical accuracy, transaction patterns, and visual artifacts to detect document manipulation with over 99% accuracy in real-time.

What are the most common signs of a forged bank statement?

The most common signs include font inconsistencies, mathematical errors in running balances, suspicious PDF creation dates, unrealistic transaction patterns, missing bank security features, and formatting irregularities.

How accurate is automated fraud detection compared to manual review?

Automated fraud detection is significantly more accurate than manual review, with accuracy rates exceeding 99% compared to 60-80% for human reviewers. Automation also processes documents in seconds rather than minutes or hours.

What are the legal consequences of submitting fake bank statements?

Submitting fake bank statements constitutes fraud and can result in criminal charges, substantial fines, loan default, permanent blacklisting from financial services, and potential federal prosecution depending on the amount involved.

Ready to Automate Fraud Detection?

Stop reviewing bank statements manually. ClearStaq's fraud detection engine catches what human eyes miss — analyzing 27 fraud signals in seconds, not hours. Start your free trial today.

Frequently Asked Questions

How can you tell if a bank statement is fake?

Look for inconsistent fonts, incorrect running balances, suspicious PDF metadata, round-number deposits, formatting irregularities, missing security features, and pixel-level manipulation evidence. Automated tools can detect these signs instantly by analyzing 27+ fraud signals simultaneously.

Can AI detect fake bank statements automatically?

Yes. AI-powered fraud detection analyzes PDF metadata, font consistency, mathematical accuracy, transaction patterns, and visual artifacts to detect document manipulation with over 99% accuracy in real-time.

What are the most common signs of a forged bank statement?

The most common signs include font inconsistencies, mathematical errors in running balances, suspicious PDF creation dates, unrealistic transaction patterns, missing bank security features, and formatting irregularities.

How accurate is automated fraud detection compared to manual review?

Automated fraud detection is significantly more accurate than manual review, with accuracy rates exceeding 99% compared to 60-80% for human reviewers. Automation also processes documents in seconds rather than minutes or hours.

What are the legal consequences of submitting fake bank statements?

Submitting fake bank statements constitutes fraud and can result in criminal charges, substantial fines, loan default, permanent blacklisting from financial services, and potential federal prosecution depending on the amount involved.

ClearStaq Team

Product Team

The ClearStaq team builds AI-powered tools for bank statement parsing, fraud detection, and income verification.