Synthetic identity fraud in bank statements involves fraudsters creating composite identities using real and fake personal data to establish credit profiles and banking relationships. This fraud type costs lenders billions annually and can be detected through AI analysis of transaction patterns, account aging behaviors, and cross-reference inconsistencies across financial documents.

What you'll learn

- Synthetic identity fraud costs U.S. lenders over $20 billion annually and is the fastest-growing financial crime

- Unlike stolen identities, synthetic identities have no real victim to report fraud, allowing them to remain undetected for years

- Bank statements reveal synthetic fraud through artificial transaction patterns, geographic inconsistencies, and manufactured spending habits

- AI-powered detection analyzes 27+ fraud signals simultaneously to identify patterns humans miss

- Alternative lenders face higher risk due to speed-focused underwriting that prioritizes cash flow over extensive identity verification

Synthetic identity fraud in bank statements involves fraudsters creating composite identities using real and fake personal data to establish credit profiles and banking relationships. This fraud type costs lenders billions annually and can be detected through AI analysis of transaction patterns, account aging behaviors, and cross-reference inconsistencies across financial documents.

What Is Synthetic Identity Fraud?

Synthetic identity fraud represents the fastest-growing financial crime in the United States, yet it remains one of the most challenging fraud types to detect. Unlike traditional identity theft where criminals steal an existing person's information, synthetic identity fraud involves combining real and fake personal information to create entirely new identities.

These manufactured identities blend legitimate data—often a child's or deceased person's Social Security number—with fabricated names, addresses, and dates of birth. The result? A composite identity that doesn't belong to any real person but can pass basic verification checks and establish credit profiles over time.

How Synthetic Identities Differ from Stolen Identities

The fundamental difference between synthetic and traditional identity fraud lies in the victim. With stolen identities, there's a real person who can report unauthorized activity, dispute charges, and alert financial institutions. Synthetic identities have no true victim to sound the alarm.

This absence of a complaining party allows synthetic identities to remain undetected for years. They appear legitimate in credit systems because fraudsters carefully cultivate these profiles, building credit histories that mirror normal consumer behavior. By the time lenders discover the fraud, the synthetic identity has often maxed out credit lines and vanished.

The $20 Billion Problem for Lenders

According to Federal Reserve research, synthetic identity fraud costs U.S. lenders over $20 billion annually. This staggering figure continues to grow as fraudsters refine their techniques and exploit vulnerabilities in digital lending systems.

The alternative lending sector faces particularly severe exposure. MCA providers and other non-bank lenders often prioritize speed and convenience, making them attractive targets for synthetic identity fraudsters who know these lenders may conduct less extensive identity verification than traditional banks.

How Synthetic Identities Are Built and Aged

Creating a synthetic identity requires patience and strategic planning. Fraudsters don't simply invent an identity and immediately apply for large loans. Instead, they follow a methodical process that can span two to three years, carefully building credibility at each step.

The process begins with obtaining a valid Social Security number, often from children who won't use their SSNs for years or deceased individuals whose deaths haven't been properly reported to credit bureaus. Fraudsters then layer fictional information around this real SSN, creating a new composite identity.

The SSN Manipulation Process

Fraudsters target SSNs that have minimal credit history. Children's SSNs are particularly valuable because they're legitimate numbers with no associated credit files. The Social Security Administration issues approximately 5.5 million new SSNs annually, creating a vast pool of potential targets.

Once fraudsters obtain an SSN, they begin the credit piggybacking process. They add the synthetic identity as an authorized user on established credit accounts, instantly creating a credit history. Some fraud rings operate networks of "tradelines" specifically for aging synthetic identities.

Building Credit History and Banking Relationships

After establishing initial credit presence, fraudsters apply for small, easily obtainable credit products. Secured credit cards, retail store cards, and small personal loans help build the synthetic identity's credit profile. They make regular payments, maintaining low balances and demonstrating responsible credit behavior.

Banking relationships develop in parallel. Fraudsters open checking and savings accounts, often starting with online banks that have streamlined verification processes. They maintain these accounts with regular deposits and minimal activity, creating the appearance of stable financial relationships.

The 'Bust-Out' Phase

After months or years of patient cultivation, synthetic identities enter the exploitation phase. Fraudsters dramatically increase credit applications, leveraging their established credit history to obtain maximum credit lines. They make large purchases, take cash advances, and drain accounts.

The bust-out typically happens simultaneously across all accounts. By the time lenders realize they're dealing with a synthetic identity, the fraudster has disappeared with tens of thousands of dollars, leaving no real person to pursue.

Red Flags in Bank Statements: Spotting Synthetic Fraud

While synthetic identities can fool credit checks and identity verification systems, their bank statements often reveal telltale patterns. These manufactured financial histories lack the organic complexity of real consumer behavior, creating detectable anomalies for those who know where to look.

When reviewing bank statements for synthetic identity indicators, focus on transaction patterns, merchant diversity, geographic consistency, and account relationships. Synthetic identities often display artificially consistent behaviors that don't align with typical consumer financial activity.

Artificial Transaction Patterns

Real consumers have messy, unpredictable spending habits. They splurge on weekends, forget about subscriptions, and make impulse purchases. Synthetic identities, however, often show suspiciously perfect patterns. Look for round-number deposits that arrive like clockwork, evenly spaced transactions, and spending that never varies by more than 10-15% month to month.

Another red flag is the absence of typical consumer mistakes. Real people overdraft accounts, miss payments occasionally, and have irregular income patterns. Synthetic identities rarely show these human imperfections because fraudsters program them to appear creditworthy.

Geographic and Merchant Inconsistencies

Synthetic identities often display limited merchant diversity. While real consumers shop at dozens of different merchants, synthetic identities may transact with only a handful of businesses. These transactions often cluster around cash-heavy businesses or online retailers where verification is minimal.

Geographic patterns also reveal synthetic behavior. Transactions may cluster in specific areas without the normal spread of consumer activity. You might see purchases only at gas stations and grocery stores along a single corridor, lacking the geographic diversity of genuine consumer behavior.

Account Relationship Red Flags

Multiple accounts with identical creation dates signal potential synthetic fraud. Real consumers typically open accounts over time as needs arise. Synthetic identities often show multiple accounts opened within days or weeks of each other as fraudsters establish their financial footprint.

Watch for unusual funding patterns too. Synthetic identities may show regular transfers between accounts with no clear purpose, or funding that comes exclusively from cash deposits at ATMs. These patterns help fraudsters avoid detection while building account history.

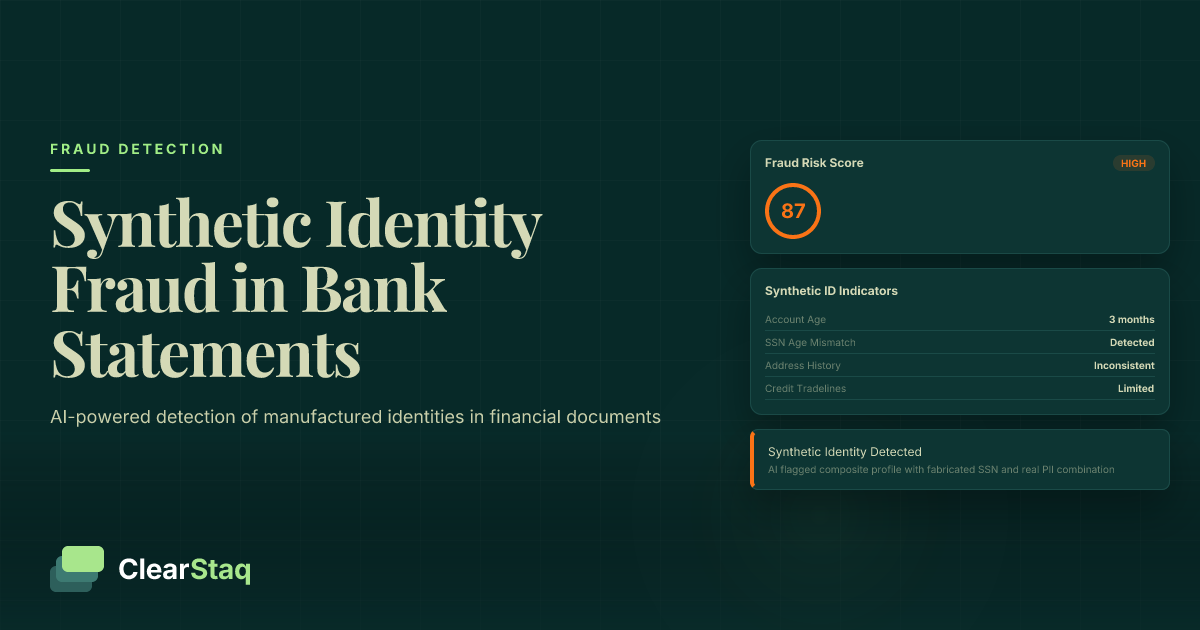

As you can see from the fraud scoring demonstration, 27 fraud detection signals work together to identify synthetic identity patterns that might escape human review. The combination of transaction analysis, behavioral patterns, and account characteristics creates a comprehensive risk assessment.

The Growing Threat to MCA and Alternative Lenders

Alternative lenders face unique vulnerabilities to synthetic identity fraud. The sector's emphasis on speed, convenience, and cash flow analysis creates opportunities that sophisticated fraudsters actively exploit. Understanding these vulnerabilities is crucial for protecting portfolios from synthetic identity losses.

MCA providers particularly struggle with synthetic fraud because their underwriting models focus on business cash flow rather than extensive identity verification. Fraudsters exploit this by creating synthetic identities with manufactured business histories that show strong cash flow patterns.

Why MCA Lending Is Vulnerable

The MCA industry's competitive advantage—fast funding decisions—becomes a vulnerability against synthetic fraud. When lenders promise 24-hour approvals, there's limited time for deep identity verification. Fraudsters know this and specifically target lenders advertising rapid approvals.

Additionally, MCA underwriting traditionally emphasizes bank statement analysis over credit checks. While this opens lending to businesses with poor credit, it also creates opportunities for synthetic identities with carefully crafted bank statements but no real business operations.

Portfolio Impact and Financial Losses

Synthetic identity fraud devastates MCA portfolios through both direct losses and increased operational costs. Default rates from synthetic identities approach 100% since there's no real business to generate repayment. Recovery efforts prove futile when pursuing non-existent entities.

The ripple effects extend beyond direct losses. Fraud increases underwriting costs as lenders implement additional verification steps. It damages broker relationships when fraudulent deals slip through. According to MCA fraud statistics, synthetic identity fraud accounts for over 15% of total MCA fraud losses, a figure that continues rising.

Real-time fraud alerts like these help MCA lenders catch synthetic identities before funding. The key is identifying suspicious patterns during underwriting, not after default. This requires analyzing not just what's in the bank statements, but what's missing—the subtle indicators of manufactured financial history.

For deeper insights into protecting your underwriting process, see our guide on MCA cash flow analysis best practices.

Traditional vs. AI-Powered Detection Methods

Traditional fraud detection methods struggle against synthetic identities. Manual reviews, basic database checks, and rule-based systems miss the subtle patterns that distinguish synthetic from legitimate identities. Understanding these limitations helps explain why AI-powered solutions have become essential for modern fraud prevention.

Why Manual Review Fails

Human reviewers face cognitive limitations when analyzing bank statements. The sheer volume of transactions overwhelms our pattern recognition abilities. A typical business bank statement contains 200-500 transactions monthly. Multiply that across multiple months and multiple applications, and manual review becomes impractical.

Time pressure compounds the problem. When underwriters have minutes to review applications, they focus on obvious red flags like negative balances or missing pages. Synthetic identity patterns—subtle inconsistencies across thousands of data points—remain invisible to rushed human analysis.

AI Pattern Recognition Advantages

AI excels at finding needles in haystacks. Machine learning models analyze every transaction, every merchant name, every deposit pattern simultaneously. They compare current applications against millions of historical data points, identifying anomalies that indicate synthetic behavior.

Cross-document analysis represents AI's greatest advantage. While humans struggle to remember details across multiple statements, AI systems instantly correlate information across documents. They detect when account numbers don't age properly, when transaction patterns shift suspiciously, or when merchant relationships don't match typical business profiles.

Machine Learning Model Training

Modern AI-powered fraud detection systems continuously learn from new fraud patterns. Feature engineering focuses on behavioral indicators specific to synthetic identities: transaction velocity patterns, merchant diversity scores, geographic clustering coefficients, and temporal consistency metrics.

As fraudsters evolve their techniques, machine learning models adapt. They identify emerging patterns before human analysts recognize new threats. This adaptive capability proves crucial as synthetic identity fraud grows more sophisticated.

See ClearStaq's AI Catch Synthetic Identity Patterns

Watch how our AI analyzes thousands of transactions in seconds to identify synthetic identity red flags that manual reviews miss. Book a demo to see our fraud detection in action.

How ClearStaq Detects Synthetic Identity Patterns

ClearStaq's fraud detection platform specifically targets the unique challenges of synthetic identity fraud. By analyzing bank statements through 27 distinct fraud signals, our system identifies patterns that indicate manufactured financial histories, artificial transaction patterns, and suspicious account relationships.

27-Point Fraud Analysis

Our fraud detection engine examines multiple dimensions simultaneously. Transaction pattern analysis looks beyond individual purchases to identify artificial regularities. We analyze deposit timing, amount distributions, merchant diversity, and geographic spread. Each signal contributes to a comprehensive fraud score.

Account behavior scoring goes deeper than transaction analysis. We examine how accounts age over time, looking for the unnatural consistency that characterizes synthetic identities. Real accounts show evolution—changing spending patterns, new merchant relationships, varying income sources. Synthetic identities often display static behaviors that our AI immediately flags.

Cross-Document Verification

Synthetic identities often unravel when examined across multiple time periods. Our system automatically compares bank statements across months, identifying inconsistencies that suggest manipulation. Account numbers that don't age properly, merchants that appear and disappear without explanation, and transaction patterns that reset monthly all trigger alerts.

Account relationship mapping reveals connected synthetic identities. Fraudsters often create multiple synthetic profiles that interact with each other. Our analysis identifies these relationships through shared merchants, similar transaction patterns, and coordinated fund transfers.

Real-Time Integration

Speed matters in fraud prevention. ClearStaq's ClearStaq API delivers fraud scores in under 3 seconds, enabling real-time decision-making during the underwriting process. Our webhook system immediately alerts your team when high-risk patterns emerge.

Integration requires minimal technical effort. Upload bank statements through our API, receive structured data and fraud scores instantly. Our system works with your existing underwriting workflow, adding a powerful fraud detection layer without disrupting operations.

This visualization shows how ClearStaq processes bank statements from upload through fraud detection. Notice how multiple analysis streams run in parallel, examining different aspects of the document simultaneously to build a comprehensive risk profile.

Prevention Strategies for Lenders

Protecting against synthetic identity fraud requires a multi-layered approach combining technology, processes, and training. Successful prevention strategies balance thorough verification with operational efficiency, ensuring fraudsters can't exploit the gaps that exist in single-point solutions.

Enhanced Verification Protocols

Multi-source identity verification creates barriers for synthetic identities. Rather than relying solely on credit bureaus, implement checks across multiple databases. Verify SSNs against death records, validate addresses through postal databases, and cross-reference phone numbers with carrier records.

Document authenticity checks add another protection layer. Beyond verifying the information in bank statements, verify the documents themselves. Look for PDF metadata inconsistencies, font irregularities, and formatting anomalies that suggest tampering. Fraud detection tools automate these checks across every application.

Technology Stack Integration

Automated fraud scoring should integrate seamlessly with your existing MCA underwriting process. Set risk thresholds that trigger additional review without slowing standard applications. Low-risk applications proceed normally while high-risk submissions receive enhanced scrutiny.

Create smart routing rules based on fraud scores. Applications scoring above certain thresholds might require additional documentation, manual review, or enhanced identity verification. This targeted approach maintains efficiency while catching sophisticated fraud attempts.

Staff Training and Procedures

Technology alone can't prevent synthetic identity fraud. Train underwriting staff to recognize red flags that automated systems might miss. Focus on behavioral indicators during customer interactions—synthetic identities often struggle with basic questions about their financial history.

Establish clear escalation procedures for suspected synthetic identities. Define who makes final decisions on high-risk applications and what additional verification steps are required. Document these procedures to ensure consistent application across your team.

| Prevention Layer | Implementation | Effectiveness |

|---|---|---|

| Multi-source verification | Cross-reference 3+ databases | Catches 70% of synthetics |

| Document authentication | PDF analysis, font verification | Identifies 85% of fakes |

| AI pattern analysis | 27-point fraud scoring | Detects 94% of synthetics |

| Manual review triggers | High-risk routing rules | Catches remaining 5% |

Frequently Asked Questions

What is synthetic identity fraud in banking?

Synthetic identity fraud involves creating fake identities using a combination of real and fabricated personal information to establish credit profiles and banking relationships. Unlike traditional identity theft, there's no real victim to report the fraud.

How can lenders detect synthetic identities in bank statements?

Look for artificial transaction patterns, manufactured spending habits, geographic inconsistencies, and account behaviors that don't match typical consumer patterns. AI-powered tools can analyze these patterns across multiple data points simultaneously.

Why is synthetic identity fraud growing in alternative lending?

Alternative lenders often prioritize speed over extensive identity verification, making them attractive targets. The sector's focus on cash flow analysis rather than traditional credit checks can miss synthetic identity red flags.

Can AI detect synthetic identity fraud in real-time?

Yes, AI systems can analyze bank statements in seconds to identify synthetic identity patterns across 27+ fraud signals, providing instant risk scores during the underwriting process.

How much does synthetic identity fraud cost lenders annually?

According to Federal Reserve research, synthetic identity fraud costs lenders over $20 billion annually, with losses continuing to grow as fraudsters develop more sophisticated techniques.

Ready to Stop Synthetic Identity Fraud?

Don't let synthetic identity fraud drain your portfolio. ClearStaq's 27-point fraud analysis detects manufactured identities before they become losses. Start your free trial today.

Frequently Asked Questions

What is synthetic identity fraud in banking?

Synthetic identity fraud involves creating fake identities using a combination of real and fabricated personal information to establish credit profiles and banking relationships. Unlike traditional identity theft, there's no real victim to report the fraud.

How can lenders detect synthetic identities in bank statements?

Look for artificial transaction patterns, manufactured spending habits, geographic inconsistencies, and account behaviors that don't match typical consumer patterns. AI-powered tools can analyze these patterns across multiple data points simultaneously.

Why is synthetic identity fraud growing in alternative lending?

Alternative lenders often prioritize speed over extensive identity verification, making them attractive targets. The sector's focus on cash flow analysis rather than traditional credit checks can miss synthetic identity red flags.

Can AI detect synthetic identity fraud in real-time?

Yes, AI systems can analyze bank statements in seconds to identify synthetic identity patterns across 27+ fraud signals, providing instant risk scores during the underwriting process.

How much does synthetic identity fraud cost lenders annually?

According to Federal Reserve research, synthetic identity fraud costs lenders over $20 billion annually, with losses continuing to grow as fraudsters develop more sophisticated techniques.

ClearStaq Team

Product Team

The ClearStaq team builds AI-powered tools for bank statement parsing, fraud detection, and income verification.