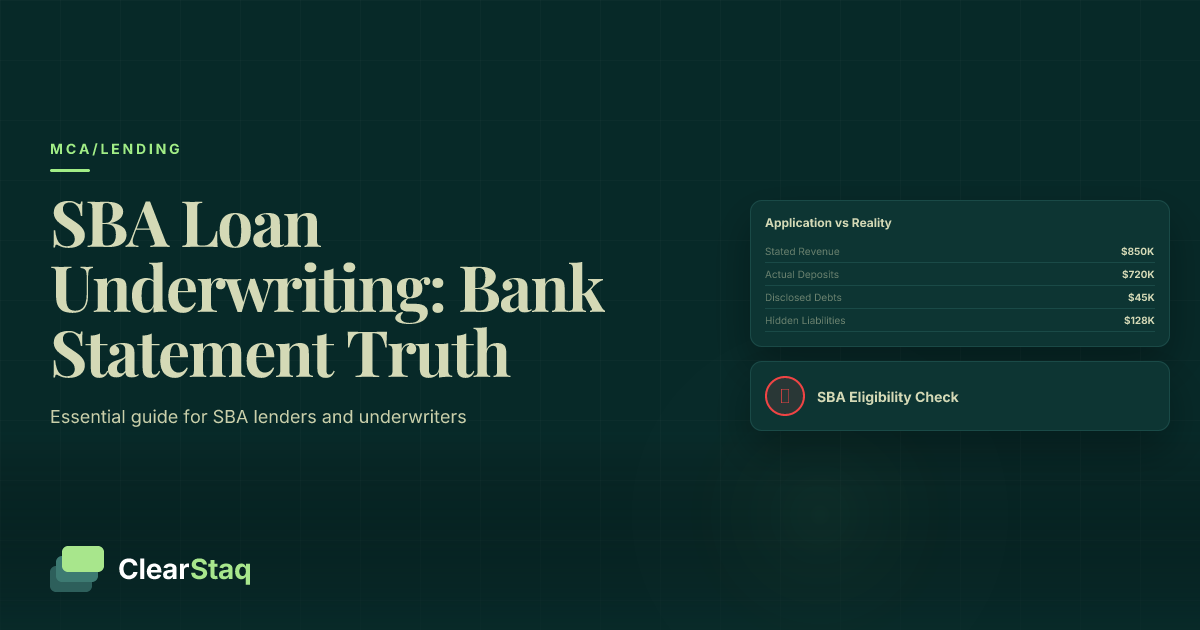

SBA loan bank statements reveal critical information that applications conceal: true cash flow patterns, undisclosed liabilities, seasonal fluctuations, personal vs. business expense mixing, and debt service coverage accuracy. While applications show projections, bank statements expose actual transaction history over 12+ months, helping underwriters assess real business stability and SBA eligibility compliance.

What you'll learn

- Bank statements show actual transaction history while applications only reveal projections and intentions

- Hidden liabilities like MCA payments and undisclosed debts only appear in bank statement analysis, not applications

- Seasonal cash flow patterns in statements help verify year-round debt service capacity for SBA compliance

- Personal vs business expense mixing detected in statements can impact SBA eligibility and add-back calculations

- Automated analysis tools can process 12+ months of statements in minutes versus hours of manual review

SBA loan bank statements reveal critical information that applications conceal: true cash flow patterns, undisclosed liabilities, seasonal fluctuations, personal vs. business expense mixing, and debt service coverage accuracy. While applications show projections, bank statements expose actual transaction history over 12+ months, helping underwriters assess real business stability and SBA eligibility compliance.

Why Bank Statements Matter More Than Applications in SBA Underwriting

When it comes to SBA loan underwriting, there's a fundamental truth that experienced lenders know: applications tell you what borrowers want you to believe, but bank statements tell you what actually happened. This distinction becomes critical in SBA lending, where the government guarantee depends on accurate assessment of business viability and borrower integrity.

The SBA's emphasis on historical cash flow over financial projections stems from decades of loan performance data. Borrowers can craft compelling narratives and optimistic forecasts in their applications, but bank statements provide an unfiltered view of business operations over the past 12 to 24 months.

The Limitation of SBA Applications

Standard SBA loan applications rely heavily on self-reported financial information. Borrowers provide projected revenues, estimated expenses, and anticipated cash flows that paint the most favorable picture possible. While this information has value for understanding business plans, it lacks the granular detail needed for accurate risk assessment.

Applications also fail to capture the operational rhythms that define small businesses. A restaurant's summer tourist season, a landscaping company's winter dormancy, or a retail shop's holiday surge — these patterns emerge clearly in bank statements but remain hidden in application summaries.

Most critically, applications cannot reveal what borrowers choose not to disclose: existing merchant cash advances, personal guarantee obligations, or the true extent of owner draws that impact available cash flow.

What Bank Statements Actually Reveal

Bank statements provide transaction-level detail that applications cannot match. Every deposit reveals revenue timing and consistency. Every withdrawal shows actual operating expenses, not estimates. The sequence of transactions tells the story of working capital management, vendor relationships, and cash flow timing.

For SBA underwriters, this granular data enables verification of key eligibility requirements. Bank statements confirm that businesses meet the SBA's operating requirements, demonstrate legitimate business purposes, and show the financial capacity to service additional debt.

Perhaps most importantly, bank statements reveal patterns over time. A single month's application data provides a snapshot, but 12 months of bank statements show how businesses respond to challenges, manage seasonal variations, and maintain operations through economic cycles. This is crucial for bank statement income verification that goes beyond simple deposit totals.

What SBA Lenders Look for in Bank Statements

SBA lenders follow specific guidelines when reviewing bank statements, focusing on elements that directly impact loan performance and regulatory compliance. Understanding these requirements helps explain why bank statement analysis has become more sophisticated and automated in recent years.

SBA Documentation Requirements

The SBA requires both personal and business bank statements for all principals with 20% or greater ownership. The standard requirement is 12 months of statements, though seasonal businesses or those with irregular income patterns may need 24 months to establish true operational patterns.

Lenders must obtain statements for all accounts — checking, savings, money market, and any other deposit accounts. This comprehensive requirement exists because businesses often spread operations across multiple accounts, and partial statement review can miss critical information about cash management and financial obligations.

The statements must be consecutive months with no gaps. Missing months raise immediate red flags about potential cash flow problems or attempts to hide problematic periods. Bank statements downloaded directly from financial institutions are preferred over printed statements to ensure authenticity and completeness.

Cash Flow Stability Indicators

Consistent deposit patterns indicate business stability that applications alone cannot demonstrate. Lenders analyze deposit frequency, timing, and amounts to understand revenue predictability. Regular deposits suggest stable customer relationships and predictable cash generation, while erratic patterns may indicate struggling operations or inconsistent business models.

Seasonal businesses receive special attention during this analysis. Lenders need to verify that slow periods don't create unsustainable cash shortages and that peak seasons generate sufficient reserves to carry the business through lean months. The 12-month review period captures these patterns that quarterly financial statements might miss.

Working capital management appears clearly in bank statement flows. Businesses that maintain appropriate cash reserves, time vendor payments strategically, and avoid frequent overdrafts demonstrate financial sophistication that reduces lending risk.

This business demonstrates strong financial health with consistent cash flow and minimal overdraft activity. Recommended for approval with standard terms.

Debt Service Coverage Verification

Bank statements provide the most accurate picture of existing debt obligations. Automatic loan payments, credit card settlements, and other recurring debt service appear as regular debits that applications might minimize or omit entirely.

This information enables precise calculation of debt service coverage ratios — a critical SBA underwriting metric. Lenders can identify exactly how much cash flow is available for new debt service after accounting for all existing obligations, not just those disclosed in applications.

Bank statements also reveal payment patterns that indicate financial stress. Late fees, partial payments, or irregular payment timing can signal borrowers struggling with current debt levels, even when applications suggest comfortable debt service capacity.

Cash Flow Patterns That Applications Can't Reveal

The most valuable insights from bank statement analysis come from patterns that emerge over time — patterns that no application can capture through static financial reporting. These operational rhythms tell the real story of business performance and sustainability.

Seasonal Business Analysis

Many small businesses experience significant seasonal variation that applications fail to adequately describe. A Christmas tree farm might generate 80% of annual revenue in six weeks, while a beach resort operates at full capacity for just three months. Bank statements reveal these patterns with precision that enables proper cash flow analysis.

Monthly variance analysis shows not just the magnitude of seasonal swings, but also how businesses manage the transitions. Do they build sufficient reserves during peak periods? How quickly do they recover from slow seasons? Are there consistent patterns year over year, or signs of declining performance?

Recovery time analysis becomes particularly important for businesses with extended slow periods. Bank statements show whether businesses maintain operations during off-seasons, continue meeting obligations, and position themselves for the next peak period. This information directly impacts debt service capacity calculations and loan structuring decisions.

Revenue Concentration Risk

Large, infrequent deposits often indicate customer concentration risk that applications don't adequately address. A business receiving 40% of monthly revenue from a single customer faces different risks than one with dozens of smaller, regular payments.

Bank statements enable analysis of customer payment patterns, deposit timing, and revenue diversification. This information helps lenders assess the sustainability of reported income levels and the vulnerability of businesses to customer losses.

Income diversification appears clearly in deposit patterns. Businesses with multiple revenue streams, varied payment methods, and diversified customer bases demonstrate lower operational risk than those dependent on a few large relationships. For advanced assessment techniques, lenders increasingly rely on sophisticated cash flow analysis that goes beyond simple deposit totals.

Operating Expense Patterns

Bank statements reveal the true cost structure of businesses through actual expense timing and amounts. Fixed costs appear as regular monthly debits, while variable expenses fluctuate with business activity levels. This distinction helps lenders understand operational leverage and break-even requirements.

Expense timing analysis shows how businesses manage working capital. Do they pay vendors promptly to maintain relationships, or stretch payments to preserve cash? Are there regular investments in inventory, equipment, or marketing that applications might not fully capture?

Cost control indicators emerge through expense pattern analysis. Businesses that maintain disciplined expense management during slow periods demonstrate operational sophistication that reduces lending risk. Conversely, those with uncontrolled expense growth during good times may struggle when conditions tighten.

Hidden Liabilities and Undisclosed Debts

One of the most critical functions of bank statement analysis is revealing financial obligations that borrowers fail to disclose in applications. These hidden liabilities can dramatically impact debt service capacity and loan performance.

Alternative Lending Detection

Merchant cash advances and other alternative lending products rarely appear on credit reports but show clearly in bank statements through daily or weekly payment patterns. These obligations can consume significant portions of cash flow while carrying much higher effective interest rates than traditional financing.

Factor payment patterns indicate accounts receivable financing that impacts cash flow timing and creates contingent liabilities. Equipment financing through direct payment arrangements might not appear in credit applications but shows in bank statement analysis through regular vendor payments.

The detection of these obligations is crucial for accurate debt service calculations and compliance with SBA regulations. The SBA has specific requirements about refinancing alternative lending products, making their identification essential for proper loan structuring. Advanced lenders use tools for MCA stacking detection to identify multiple undisclosed obligations.

Personal Guarantee Implications

Personal guarantees on business debt often create cross-collateral exposure that applications don't fully capture. Bank statements may show personal account transfers to cover business obligations, indicating the extent to which personal and business finances are intertwined.

Blended account usage patterns reveal situations where personal and business expenses flow through the same accounts, creating potential SBA compliance issues and complicating debt service analysis. These patterns require careful evaluation to ensure proper loan structuring and documentation.

Cross-collateral exposure becomes apparent when business bank statements show payments for what appear to be personal obligations, or when timing suggests cash flow management across multiple guarantee relationships.

Tax and Regulatory Obligations

IRS payment patterns in bank statements reveal tax compliance issues that applications might not address. Regular installment agreement payments, penalty assessments, or large quarterly payments indicate tax situations that impact cash flow and regulatory standing.

State tax obligations appear through unemployment tax payments, sales tax remittances, and other regulatory fees. The timing and amounts of these payments help verify business legitimacy and operational compliance.

Payroll tax compliance shows through regular federal and state tax deposits. Irregular timing or missing payments can indicate cash flow stress or compliance issues that increase lending risk.

See ClearStaq's SBA Analysis in Action

Upload bank statements and see instant analysis of cash flow patterns, seasonal trends, and hidden liabilities that manual review might miss. Start your free trial — no credit card required.

Personal vs Business Expense Verification

The SBA requires clear separation between personal and business expenses, making bank statement analysis critical for compliance verification. This analysis goes beyond simple categorization to assess the legitimacy of business deductions and the accuracy of financial reporting.

Expense Categorization Standards

IRS business expense rules provide the framework for evaluating bank statement transactions. Expenses must be ordinary, necessary, and directly related to business operations to qualify as legitimate business deductions. Bank statements reveal the true nature of expenses that applications might categorize differently.

SBA add-back policies allow certain owner-related expenses to be added back to cash flow for debt service calculations. However, these add-backs must be properly documented and justified through bank statement analysis. Personal use of business vehicles, family member payments, and owner benefits require careful evaluation.

Personal use indicators in business accounts include grocery purchases, personal insurance payments, residential utility bills, and other clearly non-business expenses. The frequency and magnitude of such expenses impact both compliance assessment and cash flow calculations. Effective business expense categorization requires sophisticated analysis tools that can distinguish legitimate business purposes from personal use.

Owner Draw vs Salary Analysis

Compensation method verification through bank statements ensures accurate financial reporting and tax compliance. Regular salary payments suggest formal payroll processes and proper tax withholding, while irregular draws may indicate more informal compensation arrangements.

Reasonable salary standards for S-corporation owners require verification that declared salaries align with actual payments and industry norms. Bank statements provide evidence of actual compensation levels that may differ from tax return reporting.

Tax implication assessment includes verifying that payroll tax deposits match salary payments and that owner distributions follow proper corporate formalities. Discrepancies can indicate compliance issues or financial reporting errors that impact loan analysis.

Red Flags That Can Kill an SBA Application

Certain patterns in bank statements create immediate concerns for SBA underwriters and can result in application denials regardless of other positive factors. Understanding these red flags helps explain why automated analysis has become essential for modern lending operations.

Cash Flow Stress Indicators

NSF fees indicate insufficient cash management and potential inability to service additional debt. Frequent overdrafts suggest businesses operating too close to cash flow margins, while patterns of back-to-back overdrafts indicate systematic cash shortages rather than occasional timing issues.

The frequency and timing of NSF fees and overdrafts provide insights into business cash management sophistication. Businesses that frequently overdraw accounts demonstrate poor financial planning and increase the risk of loan payment difficulties.

Minimum balance analysis reveals how close businesses operate to their cash flow limits. Accounts that frequently approach zero balances or require daily cash management indicate thin margins that may not support additional debt service obligations.

Fraud and Misrepresentation Signals

Deposit manipulation attempts appear in bank statements through unusual transaction patterns, round-number deposits that don't align with normal business operations, or timing that suggests artificial inflation of account balances during statement periods.

Circular transactions involve moving money between accounts to create the appearance of higher activity levels or deposit amounts. These patterns become apparent through detailed transaction analysis and cross-referencing between multiple account statements.

Document inconsistencies between applications and bank statements raise immediate fraud concerns. Significant variances in reported income, unexplained large transactions, or missing transaction details require investigation and explanation.

Compliance Violations

Commingling of personal and business funds violates SBA requirements for business purpose and proper record-keeping. Extensive personal use of business accounts can disqualify loans or require restructuring to ensure compliance.

Prohibited activities under SBA guidelines may appear in bank statement transactions. Gambling, adult entertainment, or other restricted business types can disqualify applications even if not prominently disclosed in business descriptions.

Undisclosed affiliations between businesses or related party transactions may appear through payment patterns that suggest common ownership or control. These relationships can impact SBA eligibility and require proper disclosure and evaluation.

Modern fraud detection systems analyze patterns across multiple dimensions simultaneously. ClearStaq's platform examines 27 fraud detection signals to provide comprehensive risk assessment that manual review cannot match in terms of speed or thoroughness.

Advanced Bank Statement Analysis Techniques

Modern SBA underwriting increasingly relies on sophisticated analysis tools that can process large volumes of transaction data quickly and accurately. These techniques go far beyond manual statement review to provide insights that improve both decision quality and processing speed.

Automated Analysis Tools

AI-powered transaction categorization systems can process months of bank statements in minutes, automatically identifying business vs. personal expenses, recurring obligations, and unusual transaction patterns. This automation enables consistent analysis standards across all applications while freeing underwriters to focus on interpretation and decision-making.

Pattern recognition algorithms identify seasonal trends, cash flow cycles, and operational patterns that might take human analysts hours to discern. These tools can spot subtle indicators of financial stress, fraud attempts, or compliance issues that manual review might miss.

Anomaly detection capabilities flag transactions or patterns that deviate from normal business operations, helping underwriters focus attention on areas that require detailed investigation. This targeted approach improves both efficiency and analysis quality.

Document Cross-Referencing

Bank statement to tax return verification ensures consistency between reported income and actual deposit patterns. Sophisticated systems can automatically compare tax return line items to categorized bank statement transactions, identifying discrepancies that require explanation.

Financial statement reconciliation capabilities match balance sheet and income statement items to actual cash flows and account balances. This cross-referencing helps verify the accuracy of borrower-prepared financial statements and identifies areas of concern.

Application consistency checking compares loan application representations to actual bank statement data, flagging material discrepancies in income, expenses, or cash flow patterns. This automated verification process helps ensure accurate risk assessment. The process of cross-referencing with tax returns has become essential for modern underwriting workflows.

How ClearStaq Enhances SBA Underwriting

ClearStaq's platform provides comprehensive bank statement analysis specifically designed for SBA lending requirements. The system automatically calculates key SBA metrics including debt service coverage ratios, cash flow stability indicators, and compliance verification measures.

The 27-point fraud detection system identifies potential misrepresentation attempts, document manipulation, and transaction anomalies that could indicate application fraud. This comprehensive screening helps protect both lenders and the SBA guarantee program from fraudulent applications.

Seasonal business analysis tools automatically identify businesses with significant seasonal variations and provide specialized cash flow analysis that accounts for operational patterns. This capability ensures appropriate loan structuring for businesses with non-standard cash flow patterns.

For lending institutions looking to streamline their SBA underwriting process while maintaining rigorous analysis standards, ClearStaq's underwriting solutions provide the automation and insights needed for efficient, accurate loan decisions.

Frequently Asked Questions

How many months of bank statements do SBA lenders require?

SBA lenders typically require 12 months of bank statements for both business and personal accounts. Some lenders may request up to 24 months for seasonal businesses or complex financial situations to better understand operational patterns and cash flow cycles.

What do SBA lenders look for in bank statements that applications don't show?

Bank statements reveal actual cash flow patterns, seasonal fluctuations, undisclosed debts, personal vs business expense mixing, and debt service coverage reality that applications cannot capture through projections alone. They show what actually happened rather than what borrowers project will happen.

Can personal expenses in business bank statements disqualify an SBA loan?

Excessive personal expenses can raise red flags, but legitimate owner draws and reasonable personal use may be acceptable if properly documented and within SBA guidelines for add-backs. The key is proper documentation and reasonable amounts relative to business income.

What bank statement red flags can kill an SBA application?

Major red flags include frequent NSF fees, unexplained large deposits, evidence of undisclosed debt payments, excessive cash transactions, and patterns suggesting fraud or misrepresentation. These indicators suggest financial stress or integrity issues that increase lending risk.

How do SBA lenders analyze seasonal businesses from bank statements?

Lenders examine 12-24 months of statements to identify seasonal patterns, calculate average monthly cash flow, assess recovery times from slow periods, and verify the business can service debt year-round. This analysis ensures loan structuring matches operational realities.

Transform Your SBA Underwriting Process

Stop manually reviewing bank statements for hours. ClearStaq's automated analysis provides instant insights into cash flow patterns, fraud risks, and SBA compliance — helping you make faster, more confident lending decisions.

Frequently Asked Questions

How many months of bank statements do SBA lenders require?

SBA lenders typically require 12 months of bank statements for both business and personal accounts. Some lenders may request up to 24 months for seasonal businesses or complex financial situations to better understand operational patterns and cash flow cycles.

What do SBA lenders look for in bank statements that applications don't show?

Bank statements reveal actual cash flow patterns, seasonal fluctuations, undisclosed debts, personal vs business expense mixing, and debt service coverage reality that applications cannot capture through projections alone. They show what actually happened rather than what borrowers project will happen.

Can personal expenses in business bank statements disqualify an SBA loan?

Excessive personal expenses can raise red flags, but legitimate owner draws and reasonable personal use may be acceptable if properly documented and within SBA guidelines for add-backs. The key is proper documentation and reasonable amounts relative to business income.

What bank statement red flags can kill an SBA application?

Major red flags include frequent NSF fees, unexplained large deposits, evidence of undisclosed debt payments, excessive cash transactions, and patterns suggesting fraud or misrepresentation. These indicators suggest financial stress or integrity issues that increase lending risk.

How do SBA lenders analyze seasonal businesses from bank statements?

Lenders examine 12-24 months of statements to identify seasonal patterns, calculate average monthly cash flow, assess recovery times from slow periods, and verify the business can service debt year-round. This analysis ensures loan structuring matches operational realities.

ClearStaq Team

Product Team

The ClearStaq team builds AI-powered tools for bank statement parsing, fraud detection, and income verification.