MCA lenders are shifting from Plaid to bank statement parsing because open banking APIs cannot detect document fraud, have limited bank coverage, lack batch processing capabilities, and miss critical MCA-specific data points like transaction categorization and stacking detection that specialized parsing platforms provide.

What you'll learn

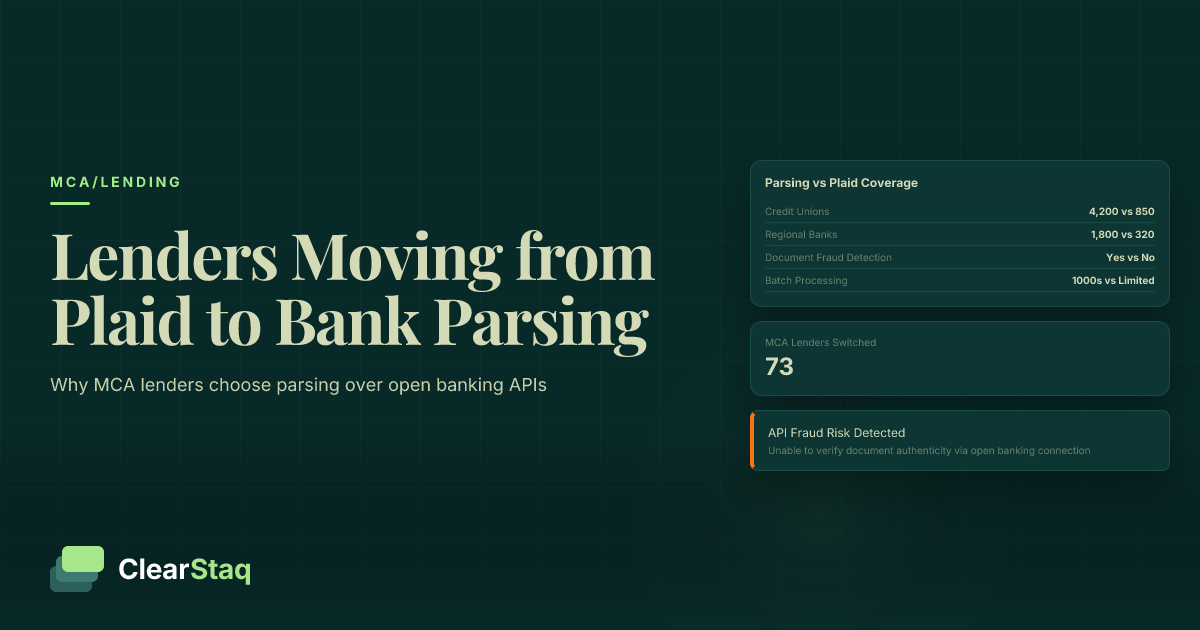

- Bank statement parsing covers 900+ banks versus Plaid's 200-300 major institutions

- Open banking APIs cannot detect document fraud or analyze PDF metadata integrity

- Parsing platforms provide MCA-specific analytics like stacking detection and revenue categorization

- Fraud detection capabilities prevent losses that often exceed processing costs by 10-50x

- Hybrid approaches combine API convenience with parsing's comprehensive analysis capabilities

MCA lenders are shifting from Plaid to bank statement parsing because open banking APIs cannot detect document fraud, have limited bank coverage, lack batch processing capabilities, and miss critical MCA-specific data points like transaction categorization and stacking detection that specialized parsing platforms provide.

The Rise of Open Banking in MCA Lending

The alternative lending industry embraced open banking APIs like Plaid as a solution to slow, manual bank statement reviews. Instead of waiting days for borrowers to collect and email PDF statements, lenders could access account data instantly through secure API connections.

This shift represented a major evolution in MCA underwriting — from labor-intensive document processing to automated data retrieval. Early adopters saw immediate benefits: faster application processing, improved borrower experience, and reduced operational overhead.

How Plaid Changed Alternative Lending

Plaid's API-first approach revolutionized how lenders accessed financial data. Through OAuth authentication, borrowers could securely connect their bank accounts and provide instant access to transaction history, account balances, and basic account information.

The platform eliminated the friction of document collection while providing structured, machine-readable data that integrated directly into underwriting systems. For an industry built on speed, this represented a significant competitive advantage.

Why MCA Lenders Initially Adopted Open Banking

MCA lenders gravitated toward open banking for three compelling reasons. First, speed — account data became available in seconds rather than hours or days. Second, improved customer experience reduced application abandonment rates. Third, structured API responses eliminated the need for manual data entry and extraction.

These advantages aligned perfectly with the MCA industry's focus on quick decisions and MCA industry trends toward automation. However, as lenders scaled their operations, critical limitations became apparent.

Why Plaid Falls Short for MCA Deals

Despite its initial promise, Plaid and similar open banking platforms reveal significant gaps when applied to MCA underwriting at scale. These limitations stem from fundamental differences between real-time account access and the comprehensive analysis that MCA deals require.

The most critical shortcoming is coverage. While Plaid connects to major national banks, it struggles with the regional banks, credit unions, and community institutions where many small businesses maintain their primary operating accounts.

Coverage Limitations: The 900+ Bank Problem

MCA borrowers rarely bank exclusively with Chase, Bank of America, or Wells Fargo. They use regional institutions like PNC, Fifth Third Bank, or local credit unions that offer better business banking terms or simply maintain long-standing relationships.

Open banking APIs typically cover 200-300 major institutions, leaving massive gaps in regional and community bank access. This coverage problem forces lenders to fall back to manual statement collection for a significant portion of applications — exactly the workflow they sought to eliminate.

ClearStaq's 900+ bank format support demonstrates the scale of this challenge. Every bank formats statements differently, and APIs simply cannot cover this institutional diversity.

Every major US bank, credit union, and fintech

Automatic format detection • Zero configuration required

The Fraud Detection Blind Spot

Perhaps more critically, open banking APIs operate on trust. They assume the connected account is legitimate and the data represents actual banking activity. This assumption creates a dangerous blind spot for MCA lenders who regularly encounter fraudulent applications.

APIs cannot analyze PDF metadata, detect document manipulation, or identify synthetic bank statements created specifically to deceive underwriters. They provide clean, structured data regardless of whether the underlying account represents real business activity or sophisticated fraud.

MCA-Specific Data Requirements

MCA underwriting requires transaction-level categorization that open banking APIs don't provide. Lenders need to identify revenue deposits versus capital injections, spot existing MCA payments, and detect signs of MCA stacking detection across multiple advances.

Standard API responses include basic transaction descriptions and amounts but lack the categorization, pattern analysis, and business context that specialized MCA platforms provide. This limitation forces lenders to build extensive post-processing systems or accept less thorough underwriting.

Bank Statement Parsing: The MCA Advantage

Bank statement parsing addresses each limitation of open banking APIs while providing capabilities specifically designed for MCA underwriting. Rather than relying on bank API partnerships, parsing platforms process the actual documents that banks generate.

This approach offers universal compatibility — any bank that produces PDF, CSV, or electronic statements can be processed regardless of API availability. More importantly, it provides access to document-level analysis that reveals fraud indicators invisible to API-based systems.

Universal Bank Format Support

Advanced parsing platforms handle the full spectrum of bank statement formats, from major national institutions to small credit unions with custom formatting. This includes PDF statements, CSV exports, OFX files, QFX downloads, and proprietary formats that APIs cannot access.

The coverage advantage is dramatic — instead of hoping a borrower's bank supports API access, lenders can process statements from virtually any financial institution. This eliminates the coverage gaps that force mixed workflows and manual exceptions.

Advanced MCA Analytics

Modern parsing platforms provide MCA-specific analysis that goes far beyond basic transaction extraction. This includes revenue recognition algorithms that identify true business income versus capital injections, cash flow volatility calculations that assess seasonal patterns, and business health indicators that predict repayment capacity.

These capabilities transform bank statements from simple transaction lists into comprehensive business assessments. Lenders gain insights into MCA cash flow analysis patterns, working capital management, and financial stability that inform better underwriting decisions.

The parsing workflow demonstrates how document analysis provides richer data than API extraction. By analyzing the actual bank statement format, metadata, and visual presentation, platforms can detect inconsistencies and anomalies that indicate potential fraud or misrepresentation.

Head-to-Head Comparison: 8 Key Factors

When evaluating open banking APIs versus bank statement parsing for MCA lending, eight critical factors determine which approach better serves underwriting needs. Each factor reveals trade-offs between convenience and capability.

| Factor | Open Banking APIs (Plaid) | Bank Statement Parsing |

|---|---|---|

| Bank Coverage | 200-300 major institutions | 900+ banks, credit unions, formats |

| Fraud Detection | None - trusts API data | 27+ signals, document analysis |

| Processing Speed | Real-time individual access | Seconds per statement, batch capable |

| Integration Complexity | OAuth flows, error handling | Simple REST API, webhooks |

| Data Retention | Limited historical access | Complete document archive |

| MCA Analytics | Basic transaction data | Categorization, stacking detection |

| Compliance | Bank-dependent permissions | Full audit trail, SOC2 |

| Cost Model | Per-connection pricing | Per-statement processing |

Coverage: APIs vs Universal Parsing

The coverage difference is stark. Open banking APIs require individual partnerships with each financial institution, creating inevitable gaps in regional and community bank support. Parsing platforms process documents directly, eliminating partnership dependencies and providing universal compatibility.

For MCA lenders, this coverage gap translates to operational complexity. Every application that involves an unsupported bank forces a manual workflow exception, reducing the automation benefits that drove API adoption in the first place.

Speed: Real-Time vs Batch Processing

While APIs provide instant access to individual accounts, they struggle with batch processing scenarios common in MCA brokerage operations. Processing 50 applications simultaneously requires 50 separate API connections, each with potential failure points and rate limits.

Bank statement parsing excels at batch processing, enabling brokers to upload multiple statements for concurrent analysis. This capability proves essential for high-volume operations where speed comes from parallel processing rather than individual transaction speed.

Integration: API Complexity vs Parsing Simplicity

Open banking integration requires OAuth implementation, bank-specific error handling, and ongoing maintenance for API changes. Each supported bank may have different data structures, rate limits, and authentication requirements.

Parsing platforms offer simpler integration through consistent APIs that handle format variations internally. Developers work with standardized responses regardless of the underlying bank statement format, reducing integration complexity and maintenance overhead.

Fraud Detection: Where Plaid Can't Compete

The most significant advantage of bank statement parsing lies in fraud detection capabilities that open banking APIs simply cannot provide. While APIs trust that connected accounts represent legitimate banking relationships, parsing platforms analyze documents for signs of manipulation and fraud.

This difference becomes critical in MCA lending, where fraudulent applications can result in substantial losses. Sophisticated fraudsters create convincing bank statements that pass visual inspection but fail detailed analysis of PDF metadata, transaction patterns, and document integrity.

See ClearStaq's Fraud Detection in Action

Experience how 27 fraud signals catch what open banking APIs miss. Book a demo to compare fraud detection capabilities side-by-side and see real fraud examples analyzed in real-time.

The 27 Fraud Signals Advantage

Advanced parsing platforms analyze 27 fraud detection signals across multiple dimensions: PDF metadata integrity, font consistency analysis, transaction pattern recognition, balance calculation verification, and visual formatting checks.

These signals detect everything from amateur document editing to sophisticated synthetic statements created by professional fraud rings. The analysis happens automatically during processing, flagging suspicious documents before they reach human underwriters.

The fraud scoring demonstration shows real-time analysis that evaluates multiple document characteristics simultaneously. This comprehensive assessment provides confidence levels for document authenticity that API-based systems cannot match.

Document Integrity vs API Trust

Open banking APIs operate within a trust framework — they assume connected accounts are legitimate because the bank authenticated the connection. This assumption breaks down when fraudsters use stolen credentials, synthetic identities, or compromised accounts.

Document analysis provides an independent verification layer that examines the bank statement itself for signs of manipulation. PDF creation analysis, modification detection, and source verification create multiple validation checkpoints that fraudsters must overcome.

Cost Analysis: TCO Comparison

Total cost of ownership comparison between open banking APIs and bank statement parsing reveals hidden expenses that affect long-term profitability. While per-transaction costs provide one metric, successful cost analysis must include fraud prevention value, operational efficiency gains, and compliance expenses.

Direct processing costs vary based on volume and provider, but the real value lies in reduced fraud losses and eliminated manual review expenses. A single prevented fraud case often justifies months of processing fees, making fraud detection capabilities a significant economic factor.

Direct Cost Comparison

Open banking APIs typically charge per connection or per account access, with costs ranging from $0.30 to $2.00 per connection depending on data depth and retention. High-volume operations may qualify for reduced pricing, but rate limits and connection management create operational overhead.

Bank statement parsing costs depend on document complexity and analysis depth, typically ranging from $0.50 to $3.00 per statement. However, batch processing capabilities and fraud detection value often provide superior ROI for MCA operations.

Hidden Costs and Risk Factors

The hidden costs of manual review become apparent when API coverage gaps force fallback processes. Every unsupported bank creates a manual exception that requires human processing, eliminating automation benefits and introducing delays.

Fraud losses represent the largest hidden cost difference. A single successful fraud case can cost $25,000 to $100,000 in MCA context, making fraud detection capabilities worth significant processing fee premiums. The prevention value often exceeds processing costs by orders of magnitude.

Implementation and Integration Differences

The technical implementation requirements for open banking APIs versus bank statement parsing reveal significant differences in complexity, maintenance overhead, and developer resources. These factors affect both initial deployment timeline and ongoing operational costs.

Open banking integration requires OAuth implementation, token management, and bank-specific error handling. Each supported institution may have different API behaviors, rate limits, and data structures that require custom handling logic.

API Integration Complexity

OAuth flows require careful implementation to maintain security while providing smooth user experience. Developers must handle consent management, token refresh cycles, and error scenarios that can interrupt data access. Each bank's API may have different requirements and limitations.

Rate limiting and connection management add operational complexity, especially for high-volume operations. API quotas, concurrent connection limits, and retry logic requirements create infrastructure challenges that affect scalability.

Parsing Integration Simplicity

Bank statement parsing offers simpler integration through consistent APIs that handle format variations internally. Developers work with standardized request and response formats regardless of the underlying document source or bank formatting differences.

The ClearStaq API integration demonstrates this simplicity through single-endpoint processing with comprehensive webhook support for automated workflows. Error handling focuses on document quality rather than API connectivity issues.

{

"status": "success",

"fraud_score": 57,

"transactions": 47,

"bank": "Chase",

"processing_time_ms": 238

}The API demonstration shows the straightforward request structure for document processing, contrasting sharply with the complex OAuth flows required for open banking integration. This simplicity reduces development time and maintenance overhead.

The Future: Hybrid Approaches and What's Next

The future of MCA data analysis lies not in choosing between open banking APIs and bank statement parsing, but in strategically combining both approaches to maximize their respective strengths while minimizing limitations.

Smart lenders are adopting hybrid workflows that use APIs for initial customer onboarding and real-time monitoring while relying on statement parsing for comprehensive underwriting analysis and fraud detection. This approach provides the best user experience without sacrificing analytical depth.

Strategic Use Cases for Each Method

Open banking APIs excel at initial customer qualification and ongoing account monitoring. They provide instant access to basic financial metrics that inform preliminary decisions and trigger alerts for significant account changes during the advance period.

Bank statement parsing dominates comprehensive underwriting scenarios where fraud detection, detailed analysis, and regulatory compliance take priority. The document-based approach provides the analytical depth and verification capabilities that final underwriting decisions require.

Regulatory and Industry Evolution

Regulatory changes continue shaping the landscape as the CFPB develops open banking standards and MCA industry practices evolve toward greater standardization. These changes will likely increase fraud detection requirements and compliance documentation standards.

The evolution favors platforms that provide comprehensive analysis capabilities with full audit trails. MCA broker solutions must balance speed with thoroughness as regulatory scrutiny increases and fraud techniques become more sophisticated.

Frequently Asked Questions

What is the difference between Plaid and bank statement parsing?

Plaid is an open banking API that connects to bank accounts for real-time data access, while bank statement parsing extracts and analyzes data from PDF/document statements. Parsing offers broader bank coverage, fraud detection, and MCA-specific analytics that APIs cannot provide.

Why don't MCA lenders use Plaid for underwriting?

Plaid lacks fraud detection capabilities, has limited bank coverage, cannot detect MCA stacking, and doesn't provide the transaction categorization and historical analysis that MCA underwriting requires. It also cannot process statements from regional banks and credit unions.

Is bank statement parsing better than open banking for MCA deals?

For MCA underwriting, yes. Bank statement parsing provides fraud detection, universal bank coverage, batch processing, and MCA-specific analytics. Open banking APIs are better for real-time account monitoring but insufficient for comprehensive underwriting.

Which approach is more cost-effective for MCA lenders?

Bank statement parsing typically offers better ROI for MCA lenders due to fraud loss prevention, reduced manual review costs, and comprehensive analysis capabilities. While per-transaction costs may vary, the total cost of ownership favors parsing for most MCA workflows.

Can MCA lenders use both Plaid and bank statement parsing together?

Yes, many lenders adopt a hybrid approach using open banking APIs for initial customer onboarding and real-time monitoring, while relying on statement parsing for comprehensive underwriting, fraud detection, and detailed financial analysis.

Ready to Move Beyond Plaid's Limitations?

ClearStaq provides the comprehensive bank statement analysis that MCA lenders actually need — with fraud detection, universal coverage, and MCA-specific insights built in. Book a demo to see the difference.

Frequently Asked Questions

What is the difference between Plaid and bank statement parsing?

Plaid is an open banking API that connects to bank accounts for real-time data access, while bank statement parsing extracts and analyzes data from PDF/document statements. Parsing offers broader bank coverage, fraud detection, and MCA-specific analytics that APIs cannot provide.

Why don't MCA lenders use Plaid for underwriting?

Plaid lacks fraud detection capabilities, has limited bank coverage, cannot detect MCA stacking, and doesn't provide the transaction categorization and historical analysis that MCA underwriting requires. It also cannot process statements from regional banks and credit unions.

Is bank statement parsing better than open banking for MCA deals?

For MCA underwriting, yes. Bank statement parsing provides fraud detection, universal bank coverage, batch processing, and MCA-specific analytics. Open banking APIs are better for real-time account monitoring but insufficient for comprehensive underwriting.

Which approach is more cost-effective for MCA lenders?

Bank statement parsing typically offers better ROI for MCA lenders due to fraud loss prevention, reduced manual review costs, and comprehensive analysis capabilities. While per-transaction costs may vary, the total cost of ownership favors parsing for most MCA workflows.

Can MCA lenders use both Plaid and bank statement parsing together?

Yes, many lenders adopt a hybrid approach using open banking APIs for initial customer onboarding and real-time monitoring, while relying on statement parsing for comprehensive underwriting, fraud detection, and detailed financial analysis.

ClearStaq Team

Product Team

The ClearStaq team builds AI-powered tools for bank statement parsing, fraud detection, and income verification.