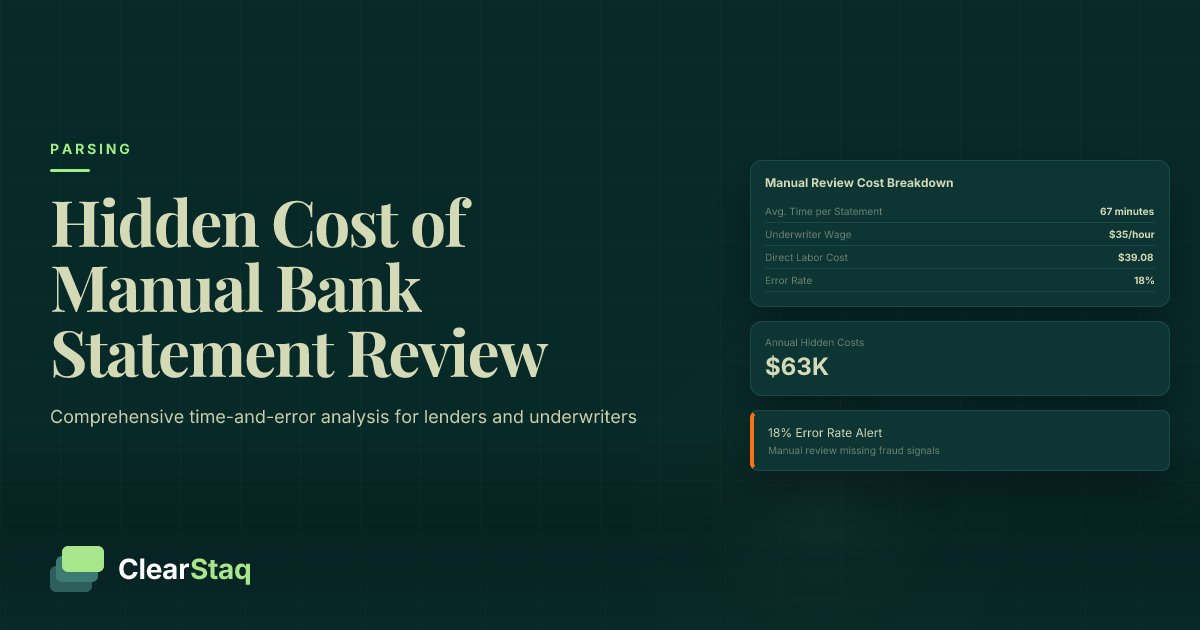

Manual bank statement review costs lenders $15-25 per application when factoring in labor, time, errors, and missed fraud. With underwriters spending 45-90 minutes per statement at $35/hour wages, plus 15-20% error rates causing loan losses, the total hidden cost can exceed $50,000 annually for mid-sized lenders processing 200+ applications monthly.

What you'll learn

- Manual bank statement review costs $15-25 per application including hidden expenses like turnover and errors

- Underwriters spend 45-90 minutes per statement with 15-20% error rates causing significant loan losses

- Automated systems achieve 99.5% accuracy versus 80-85% manual accuracy with 60-90% time savings

- Break-even for automation occurs at 50-100 applications monthly with ROI within 3-6 months

- Hidden costs include $5,000-8,000 replacement costs for 25-40% annual underwriter turnover

Manual bank statement review costs lenders $15-25 per application when factoring in labor, time, errors, and missed fraud. With underwriters spending 45-90 minutes per statement at $35/hour wages, plus 15-20% error rates causing loan losses, the total hidden cost can exceed $50,000 annually for mid-sized lenders processing 200+ applications monthly.

The True Cost of Manual Bank Statement Review

When most lenders calculate their underwriting costs, they focus on obvious expenses like salaries and software licenses. But the real manual bank statement review cost runs much deeper. Between direct labor, training overhead, and error-related losses, the true expense often doubles what appears on your P&L statement.

The foundation of this cost structure starts with labor. Skilled underwriters command $35-45 per hour in most markets, with senior reviewers earning even more. When you factor in benefits, payroll taxes, and overhead, that hourly rate climbs to $50-65 per hour in total compensation cost.

Breaking Down the Labor Math

Let's examine the real numbers behind underwriter compensation. A typical underwriter earns $72,000-94,000 annually, translating to $35-45 per hour in base wages. But direct wages represent only 65-70% of total labor costs.

The complete calculation includes:

- Base hourly wage: $35-45

- Benefits and taxes: Additional 25-30% ($9-14 per hour)

- Overhead allocation: Office space, equipment, management (15-20% or $5-9 per hour)

- Total loaded cost: $49-68 per hour

Regional variations compound this complexity. Underwriters in major financial centers like New York or San Francisco can cost 40-60% more than the national average, while rural markets may offer 20-30% savings.

The Complexity Factor

Not all bank statements require the same review intensity. Simple personal checking accounts with standard formatting might take 30-45 minutes to process manually. Business accounts with multiple subsidiaries, foreign transactions, or complex cash flow patterns can require 90-120 minutes of detailed analysis.

During peak lending seasons—typically late spring for MCA applications and year-end for traditional business loans—statement complexity increases as borrowers submit more comprehensive financial packages. This seasonal variation can double average review times when deals become more competitive and documentation requirements intensify.

Time Analysis: How Long Does Manual Review Really Take?

Industry benchmarks show manual bank statement review requires 45-90 minutes per statement, but this figure masks significant variation. The actual bank statement review time depends on document quality, format complexity, and the reviewer's experience level.

A comprehensive time-and-motion analysis reveals where those minutes accumulate. Data extraction consumes the largest chunk—typically 20-30 minutes per statement. This includes manually transcribing transaction details, identifying deposits and withdrawals, and categorizing transaction types.

Mathematical calculations add another 15-25 minutes. Underwriters must verify running balances, calculate average daily balances, identify NSF patterns, and compute income metrics. Each calculation carries error risk, often requiring double-checking that extends the timeline further.

Time Breakdown by Task

Here's how manual review time typically allocates across core tasks:

| Task | Time Range | Complexity Factors |

|---|---|---|

| Data extraction | 20-30 minutes | Page count, scan quality, format type |

| Balance verification | 10-15 minutes | Transaction volume, calculation errors |

| Income calculation | 10-15 minutes | Deposit complexity, seasonal adjustments |

| Fraud review | 10-15 minutes | Suspicious patterns, document quality |

| Documentation | 5-10 minutes | Report format, exception notes |

Fraud detection adds substantial time overhead. Manual reviewers must visually inspect for altered fonts, inconsistent formatting, suspicious round-number patterns, and impossible balance progressions. This forensic analysis requires concentration and experience that many junior underwriters haven't developed.

Format Complexity Impact

Bank format variations create massive efficiency drains in manual processing. Each of the 900+ bank formats across financial institutions uses different layouts, terminology, and data organization schemes.

Standard formats like Wells Fargo or Bank of America statements are relatively efficient to process manually—most underwriters develop familiarity with common layouts. But regional credit unions, online banks, and international institutions often use custom formats that slow manual review by 50-100%.

Multi-page statements compound these challenges. Business accounts frequently span 20-50 pages, requiring systematic page-by-page review to ensure no transactions are missed. Manual reviewers must maintain focus across dozens of pages while tracking running calculations—a setup that virtually guarantees errors.

The Error Factor: When Human Review Goes Wrong

Human error represents the most expensive hidden component of manual bank statement review cost. Research consistently shows manual data entry error rates between 15-20%, even among experienced professionals. In financial document review, where precision determines loan decisions, these errors carry severe consequences.

The most frequent manual review errors fall into predictable categories. Transcription mistakes occur when underwriters misread amounts or transpose digits. These seemingly minor errors can dramatically alter income calculations or miss critical NSF patterns that indicate repayment risk.

Types of Manual Review Errors

Mathematical calculation errors represent another major category. When manually computing average daily balances or income trends, even experienced underwriters make arithmetic mistakes under time pressure. A misplaced decimal point or incorrect average can lead to approving a loan that defaults within months.

Perhaps most critically, manual reviewers consistently miss fraud indicators that automated systems detect instantly. The human eye cannot reliably spot subtle PDF manipulation, font inconsistencies, or metadata anomalies that signal 27 automated fraud signals track systematically.

Consider these error impact examples:

- Income miscalculation: 20% error in average monthly income leads to $50,000 loan approval that should have been declined

- Missed NSF pattern: Overlooked overdraft frequency results in default within 90 days

- Fraud oversight: Undetected document manipulation leads to $100,000+ loss on fabricated income statement

The Financial Impact of Errors

Each manual review error carries direct financial consequences that compound over time. Conservative industry estimates place the average cost per significant error between $2,500-15,000, depending on loan size and error type.

Default-related losses from income miscalculations average $12,000-25,000 per incident. Regulatory penalties for inadequate fraud detection can reach $50,000-500,000 depending on the violation scope. Customer acquisition costs become waste when errors force loan denials that should have been approvals.

The 99.5% parsing accuracy of automated systems creates a measurable competitive advantage. Over 1,000 processed applications, a 15% reduction in error rates prevents 150 mistakes that would otherwise cost $375,000-2.25 million in cumulative losses.

Hidden Costs You're Not Tracking

Beyond direct labor and obvious error costs, manual bank statement review generates substantial hidden expenses that rarely appear in cost accounting analysis. Staff turnover alone creates a "hidden tax" that can double your effective review costs over multi-year periods.

Underwriting roles experience 25-40% annual turnover rates across the industry. The repetitive, detail-intensive nature of manual review contributes significantly to burnout and job dissatisfaction. Each departing underwriter triggers a cascade of replacement costs that extend far beyond simple recruitment.

The Turnover Tax

Replacing a single experienced underwriter costs between $5,000-8,000 in direct expenses, but total impact reaches $15,000-25,000 when including productivity losses. New hires require 3-6 months to reach full efficiency, during which their error rates run 50-100% higher than experienced staff.

Training costs accumulate rapidly during this ramp-up period. New underwriters need intensive supervision, frequent quality checks, and extensive coaching on bank format variations and fraud detection techniques. Senior staff productivity drops during training periods as experienced reviewers dedicate time to mentorship rather than processing applications.

Recruitment itself carries substantial costs—job posting fees, interviewing time, background checks, and opportunity costs from unfilled positions. In competitive markets, signing bonuses and premium salaries may be necessary to attract qualified candidates.

Infrastructure and Compliance Costs

Manual review operations require substantial technology infrastructure that automated solutions eliminate. Document management systems, secure file storage, and multi-user collaboration tools create ongoing licensing and maintenance expenses.

Compliance overhead represents another major hidden cost category. SOC2 compliance requirements demand extensive security controls around manual document handling. Staff must receive regular security training, access logs require monitoring, and physical document storage needs secure facilities.

Data breach risk increases exponentially with manual processes. Each additional person handling sensitive financial documents multiplies exposure points. The average financial data breach costs $5.9 million, with manual processing environments showing higher vulnerability rates than automated systems.

Ready to Calculate Your Exact ROI?

Book a demo to see how much your organization could save with automated bank statement processing. Discover your potential time savings, error reduction, and cost elimination in a personalized analysis.

Scalability Challenge: What Happens as You Grow

Manual review operations face a fundamental scalability limitation: growth requires proportional staff increases. Double your application volume, and you need twice as many underwriters. This linear scaling creates compound cost increases that strangle profitability as businesses expand.

Consider a mid-market MCA broker processing 200 applications monthly. At 60 minutes average review time per application, they need 200 hours of monthly review capacity. Factor in productivity rates, vacation time, and administrative duties, and this requires 1.5-2.0 FTE underwriters.

The Linear Scaling Trap

Scaling to 500 monthly applications demands 500 hours of review capacity—now requiring 4-5 FTE underwriters. Office space requirements expand proportionally. Management overhead increases as span of control limitations force additional supervisory layers.

Equipment and technology costs multiply with each new hire. Every underwriter needs workstation setup, software licenses, security access, and ongoing IT support. These per-seat costs accumulate rapidly as teams grow.

Quality control becomes increasingly challenging at scale. With 2 underwriters, a manager can review a meaningful sample of work daily. With 8-10 underwriters, maintaining quality standards requires dedicated QC staff or systematic sampling that may miss emerging error patterns.

Peak Season Breakdown

Seasonal lending volume surges expose the brittleness of manual scaling. Holiday lending increases, end-of-quarter deal rushes, and tax season application spikes can double normal volumes for 4-8 week periods.

Hiring temporary staff for peak seasons introduces substantial quality risks. New reviewers lack format familiarity and fraud detection experience. Error rates spike precisely when volume pressure is highest, creating a perfect storm for costly mistakes.

batch-processingThe batch processing capabilities of automated systems eliminate peak season staffing challenges entirely. Digital solutions scale instantly to handle volume surges without additional labor costs or quality degradation.

ROI Analysis: Automation vs Manual Review

The bank statement automation ROI calculation reveals compelling economics for most lending operations. Break-even typically occurs at 50-100 applications monthly, depending on current manual costs and automation pricing structures.

Time savings represent the most immediate benefit category. Automated parsing completes in 60 seconds what manual review accomplishes in 45-90 minutes—a 60-90% time reduction that translates directly to labor cost savings or capacity increases.

Error reduction provides compound benefits that grow over time. Moving from 85% manual accuracy to 99.5% automated accuracy prevents costly mistakes that otherwise accumulate. For high-volume lenders, accuracy improvements alone can justify automation investment within 6-12 months.

ROI Calculation Framework

Building accurate ROI projections requires comprehensive cost modeling that includes all manual review expenses:

Monthly Automation Savings = (Applications × Manual Cost per Application) - (Automation Fees + Remaining Manual Costs)

For a lender processing 300 monthly applications with $18 manual cost per application, monthly savings could reach $4,500-5,100 after accounting for automation fees. Annual savings of $54,000-61,200 provide substantial ROI on typical automation investments.

Implementation typically requires 2-4 weeks for API integration and staff training. Most organizations see immediate productivity gains, with full ROI realization within 3-6 months as processes optimize and error rates decline.

Real-World ROI Examples

A regional MCA lender processing 150 monthly applications calculated these results after automation implementation:

- Time savings: 75% reduction in review time (67.5 minutes to 16.5 minutes)

- Labor cost reduction: $1,687 monthly savings in direct labor

- Error prevention: $3,200 monthly savings from accuracy improvements

- Total monthly benefit: $4,887

- ROI timeline: 4.2 months

Scalability benefits compound these initial savings. The same automated system handles 500 monthly applications without proportional cost increases, creating exponential ROI improvement as volume grows.

Making the Business Case for Automation

Building executive support for bank statement automation requires quantified business cases that address both cost savings and strategic benefits. Financial stakeholders respond to concrete ROI projections backed by comprehensive cost analysis.

Start your analysis by gathering current cost data across all manual review categories. Many organizations discover their true costs exceed initial estimates by 40-60% once hidden expenses are included.

Cost Analysis Worksheet

Document these cost components for accurate baseline calculation:

| Cost Category | Monthly Amount | Notes |

|---|---|---|

| Direct labor (loaded cost) | $_______ | Include benefits, taxes, overhead |

| Training and turnover | $_______ | Amortized over 12 months |

| Error-related losses | $_______ | Defaults, penalties, rework |

| Technology overhead | $_______ | Document management, compliance |

| Management time | $_______ | QC, supervision, coordination |

Peak season costs require separate analysis since temporary staffing and overtime expenses can double baseline costs during high-volume periods.

Implementation Strategy

Successful automation implementations follow proven change management principles. Start with pilot programs on 20-30% of volume to demonstrate results before full deployment. This approach builds internal confidence while identifying process optimization opportunities.

Staff communication should emphasize how automation eliminates repetitive tasks rather than replacing jobs. Most organizations redeploy manual review staff to higher-value activities like complex deal structuring, customer relationship management, or automated cash flow analysis interpretation.

Define success metrics before implementation begins. Track time savings, error reduction, processing volume increases, and staff satisfaction scores. Quantified results strengthen the business case for expanding automation to additional processes.

Frequently Asked Questions

How long does manual bank statement review take?

Manual bank statement review typically takes 45-90 minutes per statement, depending on complexity. Simple single-account statements may take 30-45 minutes, while complex multi-account reviews can take up to 2 hours.

What is the cost of manual underwriting?

Manual underwriting costs $15-25 per application when including labor, overhead, and error costs. For a lender processing 200 applications monthly, this equals $36,000-60,000 annually in direct review costs.

What is the ROI of bank statement automation?

Bank statement automation typically delivers ROI within 3-6 months for lenders processing 50+ applications monthly. Time savings of 60-90% plus accuracy improvements create compound benefits that grow with volume.

How accurate is manual vs automated bank statement review?

Manual review accuracy ranges from 80-85% due to human error in data entry and calculations. Automated systems achieve 99.5% accuracy with consistent performance regardless of volume or complexity.

Stop Losing Money to Manual Review Inefficiencies

See how ClearStaq can reduce your bank statement processing costs by 60-80% while improving accuracy and scale. Book a demo to discover your exact savings potential and implementation timeline.

Frequently Asked Questions

How long does manual bank statement review take?

Manual bank statement review typically takes 45-90 minutes per statement, depending on complexity. Simple single-account statements may take 30-45 minutes, while complex multi-account reviews can take up to 2 hours.

What is the cost of manual underwriting?

Manual underwriting costs $15-25 per application when including labor, overhead, and error costs. For a lender processing 200 applications monthly, this equals $36,000-60,000 annually in direct review costs.

What is the ROI of bank statement automation?

Bank statement automation typically delivers ROI within 3-6 months for lenders processing 50+ applications monthly. Time savings of 60-90% plus accuracy improvements create compound benefits that grow with volume.

How accurate is manual vs automated bank statement review?

Manual review accuracy ranges from 80-85% due to human error in data entry and calculations. Automated systems achieve 99.5% accuracy with consistent performance regardless of volume or complexity.

ClearStaq Team

Product Team

The ClearStaq team builds AI-powered tools for bank statement parsing, fraud detection, and income verification.