Merchant Category Codes (MCC) are four-digit numbers that classify businesses by industry type in transaction data. Lenders use MCC analysis to assess borrower risk, detect fraud patterns, identify business changes, and make smarter underwriting decisions by analyzing transaction categories, volumes, and consistency patterns across bank statements.

What you'll learn

- MCC codes classify over 500 business types using standardized four-digit codes from payment networks

- Lenders use MCC analysis to verify business legitimacy and detect revenue source discrepancies

- High-risk MCC categories like gambling (7995) and cryptocurrency (6051) have default rates exceeding 15%

- AI-powered MCC analysis achieves 95% accuracy versus manual classification at 75-80%

- Automated tools analyze MCC patterns as part of 27 fraud signals for comprehensive risk assessment

Merchant Category Codes (MCC) are four-digit numbers that classify businesses by industry type in transaction data. Lenders use MCC analysis to assess borrower risk, detect fraud patterns, identify business changes, and make smarter underwriting decisions by analyzing transaction categories, volumes, and consistency patterns across bank statements.

What Are Merchant Category Codes (MCC)?

Merchant Category Codes are standardized four-digit numerical identifiers assigned by payment networks like Visa and Mastercard to classify businesses by their primary industry or service type. These codes serve as a universal language for transaction processing, enabling payment processors, banks, and financial institutions to quickly identify what type of business is involved in each transaction.

Payment networks maintain comprehensive lists of over 500 MCC codes, ranging from common retail categories like 5411 (grocery stores) and 5812 (restaurants) to specialized classifications like 7273 (dating services) and 6051 (cryptocurrency merchants). Each code represents a specific business type and carries associated risk profiles that lenders can analyze.

The primary purposes of MCC codes include risk management, fraud detection, regulatory compliance, and industry analysis. For lenders, these codes provide crucial insights into borrower business models, revenue sources, and operational patterns that traditional credit scores and financial statements might not reveal.

How MCC Codes Are Assigned

When merchants apply for payment processing services, their acquiring bank or payment processor assigns an MCC based on the business description, products sold, and services offered. The assignment process involves reviewing business registration documents, websites, and operational details to determine the most appropriate classification.

However, code assignment isn't always accurate. Payment processors may assign broad categories when businesses operate in multiple industries, or merchants might receive incorrect codes due to incomplete information or processor error. Studies indicate misclassification rates of 15-25%, creating challenges for lenders relying solely on MCC data.

Some merchants deliberately seek favorable MCC assignments to avoid restrictions or reduce processing fees, a practice known as "code laundering" that creates additional risks for financial institutions.

MCC vs SIC vs NAICS Codes

While MCC codes classify businesses for payment processing, Standard Industrial Classification (SIC) and North American Industry Classification System (NAICS) codes serve different purposes. SIC codes, established in the 1930s, provide broad industry categories primarily for government statistics. NAICS codes, introduced in 1997, offer more detailed industry classifications for economic analysis.

For lending decisions, **MCC codes provide the most relevant data** because they reflect actual transaction activity rather than stated business purposes. A company might register as "consulting services" (NAICS 541611) but generate revenue primarily through retail sales (MCC 5999), which MCC analysis would reveal through transaction patterns.

Smart lenders use MCC data as the primary business classification tool while cross-referencing SIC or NAICS codes to identify discrepancies that might indicate fraud or business model changes.

How MCC Codes Work in Transaction Data

MCC codes appear as part of the transaction record structure in bank statements and payment processing reports. Each transaction typically contains the date, amount, merchant name, location, and the four-digit MCC code that identifies the business type.

Transaction data sources include bank statements (both PDF and electronic formats), credit card processing reports, and direct feeds from payment networks. However, extracting and analyzing this data presents several challenges: inconsistent formatting across banks, missing MCC codes for certain transaction types, and variations in how different processors record the information.

Modern automated transaction categorization systems use artificial intelligence to parse transaction data, extract MCC codes, and classify transactions by industry type. These AI-powered tools can handle format variations, fill in missing codes based on merchant names, and detect anomalies that might indicate fraud or misclassification.

Reading MCC Data from Bank Statements

MCC codes typically appear in transaction descriptions within bank statements, though their location and format vary by financial institution. Some banks display the full four-digit code after the merchant name, while others abbreviate or omit codes entirely for certain transaction types.

Cash transactions, ACH transfers, and wire transfers rarely include MCC codes, creating gaps in the business classification picture. ATM withdrawals and deposits also lack MCC data, requiring lenders to infer business activity from deposit patterns and frequencies.

When MCC codes are missing, advanced analysis tools examine merchant names, transaction amounts, and timing patterns to infer likely business categories and identify potential classification issues.

Payment Network Differences

Visa and Mastercard maintain similar but not identical MCC code structures. While most common business types receive the same codes across networks, specialized industries may have different classifications. For example, certain fintech services might be categorized differently depending on the payment network.

Payment processors also introduce variations in how they record and report MCC data. Some processors use proprietary classification systems alongside standard MCC codes, while others modify code reporting based on their risk management policies.

These variations require sophisticated analysis systems that can normalize data across different sources and payment networks to provide consistent business classification for lending decisions.

Using MCC Analysis for Lending Decisions

MCC analysis transforms raw transaction data into actionable intelligence for underwriting decisions. Lenders use merchant category patterns to verify business legitimacy, assess industry-specific risks, and identify undisclosed revenue streams that might affect repayment ability.

The most powerful application is **business type verification** — comparing what borrowers claim about their business against what their transaction patterns reveal. A restaurant claiming steady revenue should show consistent MCC 5812 (restaurant) transactions, not primarily MCC 5999 (miscellaneous retail) activity.

Revenue diversification analysis examines the spread of MCC codes in deposit transactions to assess customer concentration risk. Businesses receiving payments from multiple industry categories typically demonstrate more resilience than those dependent on a single customer type or industry vertical.

MCC-Based Business Verification

Transaction MCC patterns provide objective evidence of business activities that complement loan application information. Discrepancies between stated business type and transaction categories often reveal undisclosed operations, business model changes, or application fraud.

For example, a borrower claiming to operate a consulting firm (typically low transaction volume, high average amounts) but showing numerous small-dollar retail transactions (MCC 5999) might actually be operating an undisclosed retail business with different risk characteristics.

Seasonal businesses also reveal themselves through MCC analysis. Tax preparation services show concentrated MCC 7291 activity during tax season, while landscaping companies display varying seasonal patterns that traditional financial analysis might miss.

Revenue Diversification Analysis

The variety and distribution of MCC codes in a business's deposit transactions indicate customer diversification and market resilience. Companies serving multiple industries or customer types typically show deposits from various MCC categories, suggesting lower concentration risk.

Customer concentration risk becomes apparent when 60-80% of deposits originate from a single MCC category, indicating potential vulnerability if that industry experiences downturns. This analysis integrates seamlessly with broader MCA cash flow analysis to provide comprehensive risk assessment.

Smart underwriters also examine MCC evolution over time to identify businesses expanding into new markets versus those losing market share in their primary industry.

High-Risk vs Low-Risk MCC Categories for Lenders

Different industries carry varying levels of default risk, regulatory scrutiny, and operational challenges that directly impact lending decisions. Understanding MCC-based risk categories helps lenders set appropriate terms, limits, and monitoring requirements for different business types.

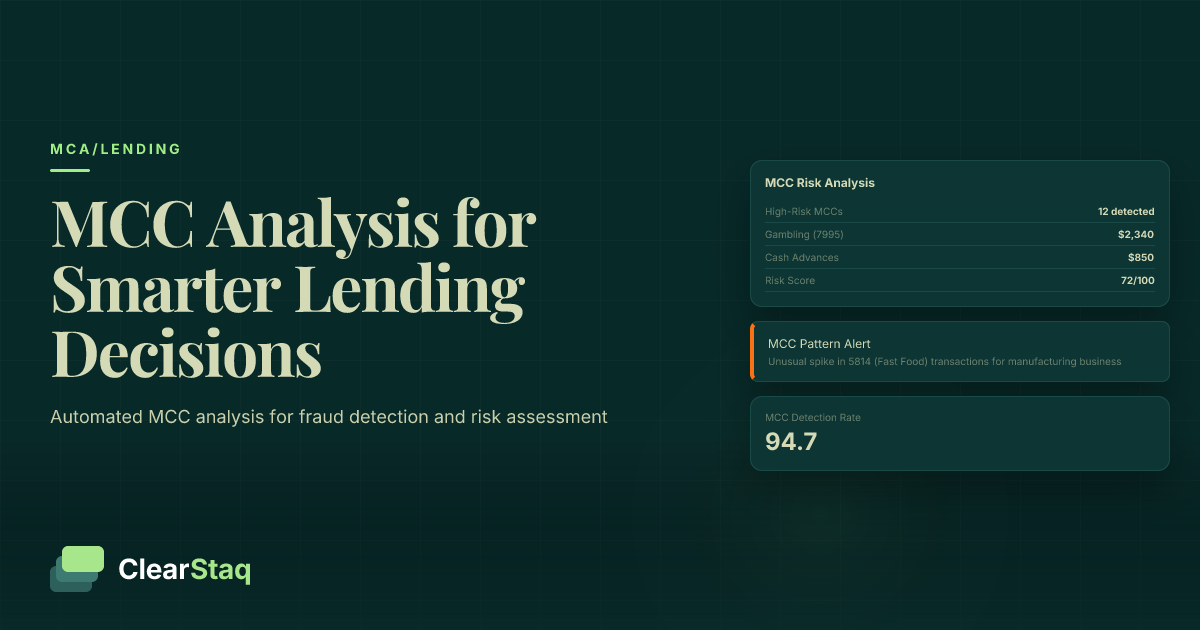

**High-risk MCC categories** typically include adult entertainment (7273), gambling and gaming (7995), cryptocurrency services (6051), debt collection agencies (7322), and payday lending operations (6012). These industries face regulatory restrictions, high chargeback rates, and volatile business models that increase default probability.

**Medium-risk categories** encompass restaurants (5812), retail establishments (5999), travel services (4722), and construction contractors (1799). While these businesses operate in legitimate industries, they often experience seasonal fluctuations, high failure rates, or cash flow challenges that require careful evaluation.

**Low-risk MCC codes** include professional services (8999), healthcare providers (8011), educational institutions (8220), and established retail chains (5411). These categories typically demonstrate stable cash flows, lower default rates, and predictable business models that align with traditional lending criteria.

Top 10 High-Risk MCC Codes

The highest-risk MCC codes for lenders include gambling establishments (7995) with default rates exceeding 15%, adult entertainment services (7273) facing constant regulatory challenges, cryptocurrency merchants (6051) operating in volatile markets, and debt collection agencies (7322) with inherent business model risks.

Telemarketing operations (5967), payday loan companies (6012), and check cashing services (6051) also rank among high-risk categories due to regulatory scrutiny and business model sustainability concerns. Many traditional lenders maintain prohibited MCC lists that automatically decline applications from these categories.

However, risk assessment should consider the entire transaction profile rather than individual MCC codes. A business showing minimal activity in high-risk categories alongside substantial legitimate business activity might still qualify for financing with appropriate terms and monitoring.

Emerging Risk Categories

New business models continue to challenge traditional MCC classification systems. Gig economy platforms, subscription box services, social media influencers, and digital content creators often operate across multiple MCC categories or receive inappropriate classifications that mask their true risk profiles.

The rise of online marketplaces and platform businesses creates additional complexity, as individual merchants may process transactions through marketplace MCCs rather than their specific business category codes. This trend requires more sophisticated analysis of underlying business activities beyond surface-level MCC data.

Cryptocurrency-related businesses present particular challenges, as payment processors frequently reassign these merchants to generic categories to avoid regulatory complications, making risk assessment through MCC analysis more difficult.

MCC Fraud Patterns and Red Flags

Fraudulent applications and business misrepresentation often reveal themselves through MCC pattern analysis. Sophisticated AI fraud detection systems examine transaction categorization for inconsistencies, anomalies, and patterns that suggest deliberate deception or document manipulation.

**Inconsistent MCC codes** represent the most common fraud indicator — when the same merchant appears with different category codes across transactions, suggesting either processing errors or deliberate misrepresentation. Legitimate businesses typically maintain consistent MCC classifications across all payment processing relationships.

**High-risk code switching** occurs when merchants move from prohibited or restricted categories to more favorable classifications to access financing. This pattern often appears as sudden shifts from high-risk MCCs to generic categories like 5999 (miscellaneous retail) without corresponding business model changes.

**Volume anomalies** manifest as transaction patterns inconsistent with stated MCC categories. For example, a professional services firm (8999) showing hundreds of small-dollar transactions daily suggests retail activity that contradicts the business classification.

Common MCC Fraud Schemes

**Code laundering** involves merchants deliberately obtaining favorable MCC assignments to access restricted services or better processing rates. They may register shell companies in acceptable categories while conducting business in prohibited industries, creating misleading transaction patterns.

**Payment facilitator abuse** occurs when merchants use payment processors or aggregators to mask their true business activities. Transactions appear under the facilitator's MCC rather than the actual merchant category, obscuring high-risk business activities from lender analysis.

**Shell company indicators** include businesses showing MCC activity completely unrelated to their stated operations, minimal transaction volume despite claiming substantial revenue, or MCC patterns that change dramatically without explanation.

Detection Techniques

Advanced fraud detection systems analyze MCC patterns using machine learning algorithms that identify statistical anomalies, compare business profiles against industry benchmarks, and flag transactions that deviate from expected patterns for specific business types.

Cross-reference verification compares MCC data against business registration information, website content, and stated business activities to identify mismatches. Comprehensive systems incorporate 27 fraud detection signals including MCC analysis alongside document authenticity, transaction patterns, and metadata analysis.

Automated alerts trigger when businesses show prohibited MCC activity, sudden category changes, or transaction volumes inconsistent with their stated industry classification, enabling rapid fraud identification before funding decisions.

Automated MCC Analysis Tools

Modern lending operations require automated systems to process the volume and complexity of MCC data in bank statement analysis. AI-powered categorization tools use machine learning algorithms trained on millions of transactions to classify business activities, detect anomalies, and provide real-time risk assessment capabilities.

**Pattern recognition algorithms** identify subtle indicators that human reviewers might miss, such as gradual shifts in MCC distribution, seasonal patterns that don't match stated business types, or correlation anomalies between transaction amounts and merchant categories.

**Real-time processing capabilities** enable instant analysis of bank statements upon upload, providing immediate insights into business classifications, risk indicators, and fraud patterns. This speed advantage allows lenders to make faster decisions while maintaining thorough analysis standards.

See ClearStaq's Automated MCC Analysis in Action

Watch how ClearStaq's automated MCC analysis integrates with 27 fraud signals to provide instant risk assessment. Book a demo to see it analyze real bank statements in seconds.

Machine Learning Classification

Training data requirements for effective MCC classification include millions of labeled transactions across diverse industries, business types, and transaction patterns. Accuracy benchmarks for modern systems exceed 95% for common business categories, with continuous improvement through feedback loops and model updates.

Advanced systems combine MCC analysis with natural language processing of merchant names, transaction descriptions, and amounts to provide more accurate business classification than MCC codes alone. This multi-signal approach compensates for missing or incorrect MCC assignments.

Continuous improvement mechanisms incorporate new business models, emerging fraud patterns, and regulatory changes to maintain classification accuracy as the business landscape evolves.

How ClearStaq Analyzes MCC Data

ClearStaq's integrated parsing and analysis system automatically extracts MCC codes from bank statements regardless of format variations, fills gaps using AI-powered merchant name analysis, and cross-references patterns against fraud databases to provide comprehensive risk assessment.

The platform incorporates MCC analysis as part of 27 distinct fraud signals, examining category consistency, business type verification, and pattern anomalies alongside document authenticity, transaction manipulation detection, and MCA stacking detection.

Real-time risk scoring combines MCC patterns with cash flow analysis, deposit consistency, and business verification to provide instant lending decisions backed by comprehensive data analysis rather than manual review processes.

MCC Limitations and Accuracy Issues

Despite their utility in lending analysis, MCC codes face significant accuracy challenges that lenders must understand and address. **Assignment errors** occur when payment processors incorrectly classify businesses during onboarding, leading to misleading transaction categorization throughout the merchant relationship.

**Business evolution** creates ongoing accuracy problems when companies expand into new product lines or service areas without updating their MCC assignments. A restaurant adding catering services might continue showing only MCC 5812 activity despite generating significant revenue from event planning services.

**Processor variations** compound accuracy issues as different payment networks and processors may assign different codes for similar businesses based on their internal classification policies or risk management requirements.

Common Accuracy Problems

Misclassification rates vary by industry, with newer business models like digital services, subscription businesses, and platform companies experiencing higher error rates due to unclear category definitions. Traditional retail and restaurant businesses typically receive more accurate MCC assignments.

Update lag issues occur when businesses change their primary activities but payment processors don't update MCC assignments, creating persistent classification errors that affect lending analysis. Some merchants operate for months or years under incorrect codes before corrections occur.

Multi-business entities present particular challenges when single companies operate across multiple industries but receive a single primary MCC classification, obscuring the full scope of business activities from lender analysis.

Supplementing MCC Analysis

Transaction descriptions provide additional context when MCC codes are missing or incorrect. Modern analysis systems use natural language processing to extract business type indicators from merchant names and transaction details, creating more accurate categorization than MCC codes alone.

Merchant names often contain industry indicators that complement or correct MCC classifications. Advanced systems maintain databases of merchant names linked to accurate business categories, enabling verification and correction of MCC-based classifications.

Amount patterns and frequency analysis provide additional verification of business types. Professional services typically show larger, less frequent transactions while retail businesses demonstrate smaller, more frequent payment patterns that help validate or question MCC assignments.

Best Practices for MCC-Based Underwriting

Effective MCC analysis requires integration with broader underwriting processes rather than standalone evaluation. **Combine MCC data with other metrics** including cash flow patterns, deposit consistency, customer concentration analysis, and traditional financial ratios to create comprehensive risk profiles.

**Regular monitoring** of MCC patterns over time identifies business changes, seasonal variations, and emerging risks that single-point analysis might miss. Establishing baseline patterns enables detection of significant deviations that warrant additional investigation or loan restructuring.

**Industry expertise** remains crucial for interpreting MCC data within specific sector contexts. Understanding that restaurants (5812) naturally show seasonal variations while healthcare providers (8011) demonstrate steady patterns helps distinguish normal business cycles from concerning trends.

Building MCC Policies

Risk tier definitions should incorporate MCC categories alongside traditional credit metrics, creating clear guidelines for high-risk, medium-risk, and acceptable business classifications. Establish specific approval thresholds and review requirements for each risk category rather than blanket approvals or denials.

Approval thresholds might include maximum loan amounts for medium-risk MCC categories, required additional documentation for high-risk classifications, and automatic approval parameters for low-risk businesses with strong financial metrics.

Review triggers should activate when borrowers show new MCC activity, significant changes in category distribution, or patterns suggesting business model evolution that might affect repayment capacity.

Integration with Existing Workflows

Incorporate MCC analysis into standard MCA underwriting checklists to ensure consistent evaluation across all applications. Establish clear procedures for handling MCC-related red flags, required follow-up actions, and escalation procedures for unusual patterns.

Risk scoring models should weight MCC factors appropriately alongside traditional metrics, avoiding over-reliance on category classification while ensuring industry-specific risks receive proper consideration in lending decisions.

Portfolio management systems should track MCC distribution across loan portfolios to identify concentration risks, monitor industry performance trends, and adjust lending strategies based on category-specific default rates and regulatory changes.

For comprehensive MCA lending solutions that integrate automated MCC analysis with full underwriting workflows, explore MCA lending solutions designed specifically for modern lending operations.

Frequently Asked Questions

What are merchant category codes used for in lending?

Merchant Category Codes (MCC) help lenders verify business types, assess industry risk, detect fraud patterns, and analyze revenue diversification. They provide insight into what type of business a borrower operates and whether transaction patterns match their stated industry.

How do MCC codes help in underwriting decisions?

MCC codes enable lenders to verify business legitimacy, assess industry-specific risks, identify revenue sources, and detect potential fraud. They help underwriters understand business models and compare transaction patterns against industry benchmarks.

What MCC codes are considered high risk for lenders?

High-risk MCC codes include adult entertainment (7273), gambling (7995), cryptocurrency (6051), debt collection (7322), and payday lending (6012). These industries typically have higher default rates and regulatory restrictions.

How accurate are MCC codes for business classification?

MCC accuracy varies but studies show 15-25% misclassification rates due to processor errors, business evolution, and merchant manipulation. Lenders should supplement MCC analysis with transaction descriptions and merchant names for better accuracy.

Can MCC codes detect fraud in lending applications?

Yes, MCC codes can reveal fraud through inconsistent business classification, prohibited industry participation, and transaction pattern anomalies. AI-powered tools can detect MCC manipulation and cross-reference codes with stated business activities.

Ready to Automate MCC Analysis?

Stop manually reviewing MCC codes. ClearStaq's AI analyzes merchant categories, detects fraud patterns, and scores risk automatically — giving you deeper insights in seconds, not hours.

Frequently Asked Questions

What are merchant category codes used for in lending?

Merchant Category Codes (MCC) help lenders verify business types, assess industry risk, detect fraud patterns, and analyze revenue diversification. They provide insight into what type of business a borrower operates and whether transaction patterns match their stated industry.

How do MCC codes help in underwriting decisions?

MCC codes enable lenders to verify business legitimacy, assess industry-specific risks, identify revenue sources, and detect potential fraud. They help underwriters understand business models and compare transaction patterns against industry benchmarks.

What MCC codes are considered high risk for lenders?

High-risk MCC codes include adult entertainment (7273), gambling (7995), cryptocurrency (6051), debt collection (7322), and payday lending (6012). These industries typically have higher default rates and regulatory restrictions.

How accurate are MCC codes for business classification?

MCC accuracy varies but studies show 15-25% misclassification rates due to processor errors, business evolution, and merchant manipulation. Lenders should supplement MCC analysis with transaction descriptions and merchant names for better accuracy.

Can MCC codes detect fraud in lending applications?

Yes, MCC codes can reveal fraud through inconsistent business classification, prohibited industry participation, and transaction pattern anomalies. AI-powered tools can detect MCC manipulation and cross-reference codes with stated business activities.

ClearStaq Team

Product Team

The ClearStaq team builds AI-powered tools for bank statement parsing, fraud detection, and income verification.