Equipment financing fraud primarily targets bank statements through seasonal revenue manipulation, phantom collateral schemes, and cash flow inflation. Equipment lenders lose an average of $45,000 per fraudulent loan, making automated fraud detection essential for protecting against the 23% of applications that contain fabricated financial documents.

What you'll learn

- Equipment financing fraud affects 23% of applications with average losses exceeding $45,000 per case

- Fraudsters exploit seasonal business patterns and equipment collateral complexity to manipulate bank statements

- Common schemes include phantom collateral, revenue timing manipulation, and sophisticated PDF alteration techniques

- AI-powered detection analyzes 27+ fraud signals simultaneously, catching patterns manual review misses

- Automated fraud detection provides real-time analysis in seconds versus 8-12 hours for manual review

Equipment financing fraud primarily targets bank statements through seasonal revenue manipulation, phantom collateral schemes, and cash flow inflation. Equipment lenders lose an average of $45,000 per fraudulent loan, making automated fraud detection essential for protecting against the 23% of applications that contain fabricated financial documents.

The Equipment Financing Fraud Landscape

Equipment financing represents one of the most lucrative targets for financial fraud, with industry data revealing that approximately 23% of equipment loan applications contain some form of documentation manipulation. Unlike traditional lending sectors, equipment financing fraud carries significantly higher stakes — with average losses exceeding $45,000 per fraudulent loan compared to $12,000 for general business lending.

The appeal for fraudsters lies in the substantial loan amounts and extended repayment terms typical of equipment financing. Heavy machinery, construction equipment, and manufacturing systems often require funding in the hundreds of thousands or millions of dollars, making successful fraud attempts extremely profitable.

Geographic patterns show fraud concentration in rapidly growing markets where equipment demand outpaces traditional financing infrastructure. Construction hubs in Texas, Florida, and California report the highest volumes of suspicious applications, while manufacturing centers in the Midwest see more sophisticated document manipulation schemes.

Equipment Financing vs. Traditional Lending Fraud

Equipment financing fraud differs fundamentally from traditional lending fraud in both sophistication and motivation. Higher loan amounts create stronger incentives for elaborate schemes, while the complexity of equipment collateral provides more opportunities for deception.

Traditional business loans might involve straightforward revenue inflation, but equipment financing fraud often includes multiple layers: fabricated equipment invoices, phantom lease agreements, and manipulated cash flow statements that align with fictional equipment acquisition timelines.

The collateral complexity also creates vulnerabilities. Unlike real estate, equipment values can be difficult to verify independently, especially for specialized machinery or industry-specific tools. This opacity allows fraudsters to inflate equipment values or claim ownership of non-existent assets.

The True Cost of Equipment Financing Fraud

Direct losses represent only the visible portion of equipment financing fraud costs. When a $200,000 excavator loan defaults due to fraud, lenders face recovery rates averaging just 15-20% due to equipment depreciation and disposal challenges.

Operational costs compound these losses. Each fraud investigation requires 40-60 hours of specialized review, involving equipment appraisers, forensic accountants, and legal counsel. These investigations cost an additional $15,000-25,000 per case, even when fraud is eventually proven.

Regulatory implications add another layer of expense. Equipment financing fraud often triggers compliance reviews, particularly when patterns suggest systematic weaknesses in underwriting protocols. For detailed context on broader fraud trends affecting the lending industry, see our bank statement fraud statistics analysis.

Why Bank Statements Are Critical in Equipment Lending

Bank statements serve as the primary verification tool for equipment financing because they reveal the operational reality behind loan applications. Unlike tax returns or financial statements that can be prepared months after the fact, bank statements provide real-time evidence of business cash flow, seasonal patterns, and operational consistency.

Equipment loans require substantial ongoing cash flow to service debt while maintaining operations. A construction company requesting $500,000 for excavation equipment must demonstrate sufficient revenue to cover loan payments, equipment maintenance, fuel costs, and seasonal fluctuations. Bank statements reveal whether this cash flow actually exists or has been artificially inflated.

The higher loan amounts in equipment financing demand more thorough cash flow verification than typical business lending. While a $50,000 working capital loan might be approved with basic income documentation, equipment financing requires 12-24 months of bank statements to establish business stability and payment capacity.

Equipment Loan Documentation Requirements

Standard equipment financing documentation includes tax returns, financial statements, and equipment invoices, but bank statements provide the most objective verification of business viability. They show actual deposit patterns, expense timing, and cash flow consistency that other documents cannot fabricate as easily.

Enhanced due diligence for larger equipment loans often requires multiple bank account statements, including business checking, savings, and any accounts used for equipment-related transactions. This comprehensive view helps identify cross-account manipulation schemes common in sophisticated fraud attempts.

Cash Flow Patterns in Equipment-Heavy Industries

Different equipment-intensive industries exhibit distinct cash flow patterns that legitimate businesses should reflect consistently across bank statements. Manufacturing operations typically show steady, predictable revenue with periodic large equipment maintenance expenses.

Construction companies demonstrate seasonal variations with higher activity in spring and summer months, while transportation businesses show weekly or monthly patterns aligned with delivery cycles. For comprehensive techniques used in evaluating these patterns, review our guide on cash flow analysis techniques.

[data-extraction]Common Bank Statement Fraud Patterns in Equipment Financing

Equipment financing fraud schemes exploit the complexity of equipment-heavy industries to manipulate bank statements in sophisticated ways. Unlike simple revenue inflation, these schemes create entire fictional business scenarios that align with equipment acquisition needs and industry patterns.

Phantom transaction insertion represents the most common manipulation technique. Fraudsters add fake customer payments that correspond to alleged equipment usage or service delivery. A landscaping company might insert fictional payments from property management companies, while a construction business adds fake subcontractor payments that justify equipment purchases.

Cross-account manipulation involves moving funds between multiple accounts to inflate apparent business volume. Fraudsters deposit the same funds repeatedly across different accounts, creating the illusion of multiple revenue streams and higher operational capacity than actually exists.

Phantom Collateral Schemes

Phantom collateral schemes combine bank statement manipulation with fabricated equipment documentation. Fraudsters create fake invoices for non-existent equipment purchases, then manipulate bank statements to show corresponding payments that never actually occurred.

These schemes often involve inflated equipment values through doctored invoices from legitimate dealers or entirely fictional vendor relationships. The bank statements are altered to show payments matching these inflated invoices, creating a false paper trail that supports the fraudulent loan application.

Recovery is particularly challenging because the equipment never existed or was purchased for significantly less than claimed. Lenders discover the fraud only after default, when attempts to locate and repossess collateral reveal the true scope of the scheme.

Revenue Timing Manipulation

Revenue timing manipulation exploits seasonal business patterns to justify equipment financing needs. Fraudsters front-load payments by showing large deposits during typically slow periods, suggesting business growth that requires equipment investment.

Delayed expense recognition accompanies revenue timing fraud, with fraudsters removing legitimate business expenses from bank statements during periods when they inflate revenue. This creates artificially high cash flow that appears to support larger equipment loan payments.

Inter-company transfers provide another manipulation method, where fraudsters create fictional business relationships and show transfers between related entities as legitimate revenue. These transfers inflate cash flow while maintaining the appearance of diverse customer relationships.

PDF Alteration Techniques

Modern PDF alteration techniques enable sophisticated bank statement manipulation that can fool casual inspection. Fraudsters use professional editing software to match fonts, spacing, and formatting exactly, making altered statements difficult to detect without technical analysis.

Font matching challenges arise because banks use proprietary fonts and specific formatting protocols. Sophisticated fraudsters invest significant effort in replicating these elements precisely, often succeeding well enough to pass manual review processes.

Metadata manipulation accompanies visual alteration, with fraudsters attempting to modify PDF creation dates, software signatures, and other technical indicators that might reveal document tampering. Advanced detection methods examine these technical elements that manual reviews typically miss. For comprehensive coverage of these detection techniques, explore our analysis of PDF metadata analysis.

[fraud-score]Seasonal Revenue Manipulation in Equipment Loans

Seasonal businesses in equipment-intensive industries face legitimate cash flow variations that fraudsters exploit to hide manipulation. Construction companies naturally show reduced activity during winter months, while agriculture-related equipment businesses peak during planting and harvest seasons.

Fraudsters study these legitimate patterns and manipulate bank statements to show unrealistic consistency or artificial peaks during slow periods. A construction equipment rental company might fabricate winter revenue that no legitimate business in that climate could generate, hoping lenders won't recognize the geographic impossibility.

Manufacturing businesses with seasonal product demands provide another manipulation target. Fraudsters might inflate revenue during off-peak months to justify year-round equipment financing needs, creating cash flow profiles that appear stable but violate industry norms.

Identifying Legitimate vs. Fraudulent Seasonality

Industry benchmarks provide the foundation for distinguishing legitimate seasonal variations from fraudulent manipulation. Construction businesses in northern climates should show 60-80% revenue reduction during winter months, while lawn care equipment companies peak during spring and summer.

Historical pattern analysis reveals fraud when bank statements show sudden changes in seasonal patterns without corresponding business explanations. A roofing company that historically showed winter slowdowns but suddenly reports consistent year-round revenue triggers legitimate questions about data integrity.

Red flag indicators include perfectly smooth revenue across seasons, unusually high activity during industry-wide slow periods, and seasonal patterns that don't align with geographic climate realities or local economic conditions.

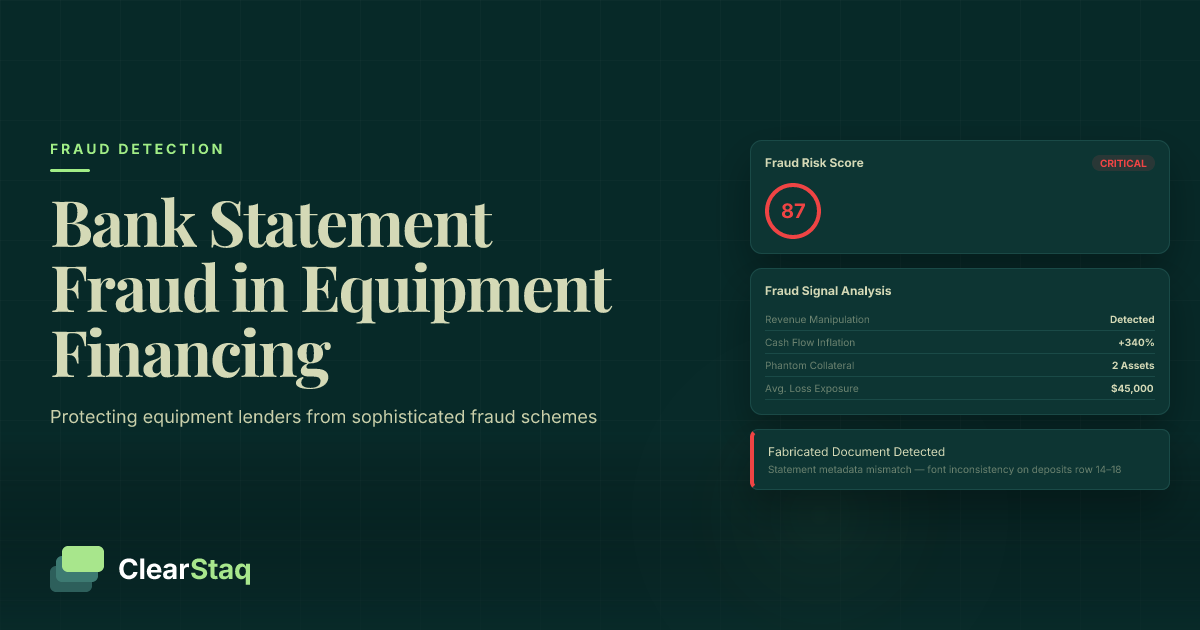

Case Study: Construction Equipment Fraud

A recent case involved a construction company requesting $750,000 for excavation equipment, supported by bank statements showing consistent $180,000 monthly revenue throughout winter months. Industry analysis revealed that legitimate construction businesses in that region average $25,000 monthly winter revenue.

The fraudulent bank statements showed fabricated payments from fictional municipal contracts and private development projects. Investigation revealed that most claimed projects didn't exist, while legitimate winter work consisted only of minor repair contracts averaging $3,000-5,000.

Project timeline manipulation accompanied the revenue fraud, with bank statements showing payment schedules that didn't align with actual permit dates or project completion timelines available through public records verification.

Red Flags: What Equipment Lenders Should Watch For

Equipment lenders should monitor specific warning signs that indicate potential bank statement manipulation. Unlike general business lending red flags, equipment financing fraud exhibits unique patterns related to equipment acquisition timing, maintenance costs, and operational expenses.

Inconsistent equipment purchase patterns represent a primary red flag. Bank statements should show equipment-related expenses that align with the requested financing timeline. A company claiming to need replacement equipment should show maintenance costs, fuel expenses, or repair payments for existing equipment.

Revenue timing misalignment occurs when bank statements show income patterns that don't correlate with typical equipment utilization cycles. Heavy equipment generates revenue through consistent usage patterns that should be reflected in regular, predictable customer payments.

Transaction Pattern Analysis

Frequency anomalies in transaction patterns often indicate manipulation. Legitimate equipment-heavy businesses show regular patterns of fuel purchases, maintenance expenses, and operational costs that fraudulent statements often omit or fail to replicate convincingly.

Amount patterns reveal fraud through unrealistic consistency or mathematical precision. Real businesses show natural variation in payment amounts, while fabricated transactions often involve round numbers or suspicious repetition.

Timing inconsistencies emerge when bank statements show business activity that doesn't align with operational realities. A snow removal service showing summer revenue or an agricultural equipment company with off-season activity may indicate manipulation.

Equipment-Specific Red Flags

Maintenance cost irregularities provide strong fraud indicators. Companies operating significant equipment should show regular maintenance expenses, fuel costs, and periodic repair charges. Bank statements lacking these operational indicators suggest either non-existent equipment or fraudulent documentation.

Fuel expense patterns vary by equipment type and usage intensity, but should appear consistently in legitimate business bank statements. Construction companies without fuel expenses, or transportation businesses with unrealistic fuel costs relative to claimed revenue, indicate potential fraud.

Equipment rental vs. purchase indicators help identify phantom collateral schemes. Companies claiming to own equipment should show insurance, licensing, and maintenance expenses, while those renting equipment should demonstrate regular rental payments to legitimate providers.

[alert-feed]For detailed guidance on recognizing these and other warning signs, consult our comprehensive fraud red flags resource.

Manual vs. Automated Fraud Detection for Equipment Lenders

Manual bank statement review for equipment financing typically requires 8-12 hours per application due to the complexity of analyzing seasonal patterns, equipment-related expenses, and industry-specific cash flow characteristics. Human reviewers must cross-reference multiple documents while maintaining awareness of equipment depreciation schedules and industry benchmarks.

The time investment creates significant operational constraints for equipment lenders processing high application volumes. During peak equipment buying seasons, manual review backlogs can extend approval timelines to 2-3 weeks, losing competitive advantage to lenders offering faster decisions.

Human limitations in pattern recognition become particularly problematic when analyzing sophisticated fraud schemes that span multiple months of bank statement data. Reviewers may identify individual suspicious transactions but miss coordinated manipulation patterns that artificial intelligence can detect immediately.

The Manual Review Challenge

Time constraints force human reviewers to focus on obvious red flags while missing subtle manipulation indicators. A reviewer spending 45 minutes per month of bank statements may catch blatant alterations but overlook metadata inconsistencies or sophisticated font matching issues.

Reviewer fatigue compounds accuracy problems during high-volume periods. Studies show fraud detection accuracy declining by 23% after reviewing more than 6 applications per day, as cognitive load impairs attention to detail.

Inconsistent standards emerge when different reviewers apply varying criteria or fail to maintain current knowledge of evolving fraud techniques. Equipment financing fraud schemes evolve rapidly, requiring constant training updates that manual processes struggle to accommodate.

AI-Powered Detection Advantages

AI-powered fraud detection analyzes 27+ simultaneous fraud signals in seconds, examining PDF metadata, transaction patterns, mathematical inconsistencies, and formatting irregularities that manual review cannot process comprehensively.

Metadata examination reveals document creation details, editing history, and software signatures that indicate potential tampering. This technical analysis operates below human perception levels but provides definitive evidence of document manipulation.

Cross-document correlation identifies patterns spanning multiple bank statements or connecting bank data with other application documents. AI systems can instantly compare transaction timing with equipment invoices, identifying discrepancies that manual review might miss. For complete details on automated capabilities, see our analysis of 27 fraud detection signals.

See ClearStaq's Equipment Fraud Detection in Action

Watch how 27 fraud signals analyze equipment financing applications in real-time, catching sophisticated manipulation that manual reviews miss. Book a demo to see actual fraud cases detected instantly.

How ClearStaq Detects Equipment Financing Fraud

ClearStaq's fraud detection engine provides real-time API integration specifically designed for equipment lending workflows. The system analyzes bank statements within seconds of upload, returning detailed fraud risk scores and specific manipulation indicators before underwriting decisions are made.

Industry-specific fraud pattern recognition distinguishes ClearStaq from generic fraud detection tools. The system maintains updated profiles of equipment-intensive industries, understanding seasonal variations, typical expense patterns, and operational indicators that legitimate businesses should demonstrate.

Equipment loan size correlation analysis evaluates whether reported cash flow realistically supports requested financing amounts while accounting for equipment depreciation, maintenance costs, and industry-typical profit margins.

Equipment-Specific Fraud Signals

Cash flow timing analysis compares bank statement deposits with industry-standard payment cycles for different equipment sectors. Construction equipment rentals typically generate weekly payments, while manufacturing equipment produces more consistent daily revenue streams.

Equipment depreciation correlation verifies that businesses claiming ownership of aging equipment show appropriate maintenance expenses, insurance costs, and operational patterns consistent with equipment condition and utilization.

Industry benchmark comparison evaluates submitted bank statements against verified data from similar businesses in comparable markets, identifying outliers that suggest manipulation or misrepresentation.

Integration with Equipment Lending Workflows

API endpoints enable seamless integration with existing equipment lending platforms, providing fraud analysis without disrupting established underwriting processes. Results appear instantly within current workflow systems.

Webhook notifications alert underwriting teams immediately when high-risk applications are detected, enabling rapid response to prevent fraudulent approvals while maintaining processing speed for legitimate applications.

Dashboard integration provides comprehensive fraud analysis summaries, including specific manipulation indicators, risk scores, and recommended follow-up actions tailored to equipment lending requirements.

Our comprehensive AI-powered document forgery detection capabilities extend beyond bank statements to analyze equipment invoices, insurance documents, and other supporting materials for consistency and authenticity.

Best Practices for Equipment Lenders

Equipment lenders should implement multi-layer verification approaches that combine automated fraud detection with targeted manual review. Initial automated screening identifies high-risk applications requiring enhanced due diligence, while low-risk applications proceed through streamlined approval processes.

Industry-specific benchmarking provides essential context for evaluating equipment financing applications. Lenders should maintain current data on seasonal patterns, typical expense ratios, and operational indicators for different equipment sectors in their target markets.

Documentation cross-referencing protocols ensure that bank statements align with equipment invoices, insurance policies, and other supporting documents. Automated systems can perform these correlations instantly, while manual processes require systematic checklists to maintain consistency.

Implementing Automated Fraud Detection

Technology selection criteria should prioritize systems designed specifically for equipment lending requirements rather than generic fraud detection tools. Equipment financing involves unique patterns and risk factors that specialized solutions handle more effectively.

Integration considerations include API compatibility with existing lending platforms, processing speed requirements during peak application periods, and scalability to handle growing application volumes without degrading performance.

Training requirements involve educating underwriting teams on interpreting automated fraud analysis results and understanding when additional manual review is warranted based on system recommendations.

Building a Fraud Prevention Culture

Team training should encompass both traditional fraud indicators and emerging techniques that fraudsters employ in equipment financing schemes. Regular updates ensure staff awareness of evolving manipulation methods.

Process documentation creates consistent standards for fraud evaluation, appeals handling, and ongoing monitoring of approved loans for signs of post-approval fraud discovery.

Continuous improvement involves analyzing fraud detection performance, false positive rates, and missed fraud cases to refine detection criteria and improve overall program effectiveness.

Consider implementing our comprehensive underwriting checklist adapted for equipment financing requirements to ensure consistent evaluation standards.

Frequently Asked Questions

What makes equipment financing vulnerable to bank statement fraud?

Equipment financing involves larger loan amounts and longer terms, making it attractive to fraudsters. The complexity of equipment collateral and seasonal business patterns in equipment-heavy industries create opportunities for sophisticated financial document manipulation.

How common is fraud in equipment lending?

Industry data shows approximately 23% of equipment financing applications contain some form of documentation fraud, with bank statement manipulation being the most common type. Average losses per fraudulent equipment loan exceed $45,000.

What are the most common bank statement fraud patterns in equipment financing?

Common patterns include seasonal revenue manipulation, phantom collateral schemes, inflated rental income, and timing manipulation of equipment purchases to justify higher cash flow requirements.

How can AI detect equipment financing fraud in bank statements?

AI analyzes 27+ fraud signals simultaneously, including PDF metadata, transaction patterns, seasonal inconsistencies, and equipment-specific cash flow indicators that human reviewers often miss during manual analysis.

What role does seasonality play in equipment financing fraud?

Fraudsters exploit legitimate seasonal variations in equipment-heavy industries by fabricating revenue during typically slow periods or smoothing out natural business cycles to appear more stable than reality.

Protect Your Equipment Lending Portfolio

Don't let equipment financing fraud drain your profits. ClearStaq's AI detects what manual reviews miss — protecting your portfolio while accelerating approvals for legitimate borrowers.

Frequently Asked Questions

What makes equipment financing vulnerable to bank statement fraud?

Equipment financing involves larger loan amounts and longer terms, making it attractive to fraudsters. The complexity of equipment collateral and seasonal business patterns in equipment-heavy industries create opportunities for sophisticated financial document manipulation.

How common is fraud in equipment lending?

Industry data shows approximately 23% of equipment financing applications contain some form of documentation fraud, with bank statement manipulation being the most common type. Average losses per fraudulent equipment loan exceed $45,000.

What are the most common bank statement fraud patterns in equipment financing?

Common patterns include seasonal revenue manipulation, phantom collateral schemes, inflated rental income, and timing manipulation of equipment purchases to justify higher cash flow requirements.

How can AI detect equipment financing fraud in bank statements?

AI analyzes 27+ fraud signals simultaneously, including PDF metadata, transaction patterns, seasonal inconsistencies, and equipment-specific cash flow indicators that human reviewers often miss during manual analysis.

What role does seasonality play in equipment financing fraud?

Fraudsters exploit legitimate seasonal variations in equipment-heavy industries by fabricating revenue during typically slow periods or smoothing out natural business cycles to appear more stable than reality.

ClearStaq Team

Product Team

The ClearStaq team builds AI-powered tools for bank statement parsing, fraud detection, and income verification.